ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

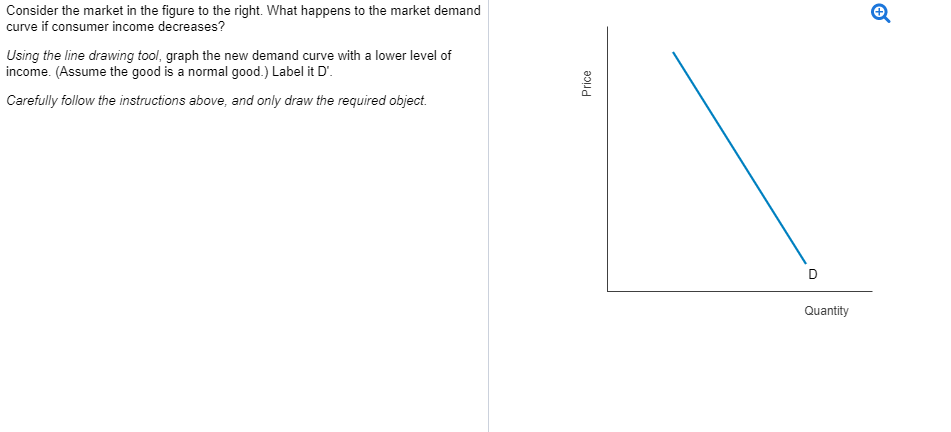

Transcribed Image Text:Consider the market in the figure to the right. What happens to the market demand

curve if consumer income decreases?

Using the line drawing tool, graph the new demand curve with a lower level of

income. (Assume the good is a normal good.) Label it D'.

Carefully follow the instructions above, and only draw the required object.

Price

D

Quantity

✔

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 10. What happens to the demand curve for an inferior good if a consumer's income increases? Show me using a diagram, please.arrow_forwardThe law of diminishing marginal utility helps to explain the direct relationship between price and quantity supplied. a. True b. Falsearrow_forwardPrice (P) S1 P2 P1 Q: Quantity (Q) In the diagram above, which of the following events would explain the change shown? Select one: a. The price of a complementary good has increased, and this is the market for its related good. b. There has been an improvement in the technology used to produce the good in this market. c. Consumer incomes have increased and this is the market for a normal good. d. There has an increase in the price of an important input used in the production of this good.arrow_forward

- Question 2 (5 marks) No words allowed, only a diagram with annotations To answer this question only a diagram with annotations is required. Suppose apples and pears are substitutes in consumption. An outbreak of Grumpy Granny Smith fungus has a devastating effect on the size of the apple crop. Show on a diagram how this will affect the market for pears. Indicate how the equilibrium price and equilibrium quantity of pears will change. The direction of any changes should be indicated using arrows. S hp Please turn over. FTSE jse 40arrow_forwardFigure 4-6Refer to Figure 4-6. The movement from D’ to D could be caused by a. an increase in the price of a complement. b. a decrease in income, assuming the good is inferior. c. a decrease in price. d. buyers expecting the price of the good to fall in the near future.arrow_forwardThe following scenarios describe products that are price.... ? 1. The new Mercedes sports car costs over 200,000 dollars 2. Jamal picks a box of corn flakes amongst the many available brands ? 3. Carl buys a large bag of gummy candies for 1 dollar ? A. Elastic B. Inelasticarrow_forward

- 05- Income and Substitution Effects Question 4arrow_forward3. If the demand for a product is perfectly price inelastic, what does the corresponding price consumption curve look like? Draw a graph to show the price consumption curve.arrow_forwardHot dogs and hot dog buns are complimentary goods. Therefore, an increase in the price of hot dogs would cause the demand for hot dog buns to A- decrease. B-stay the same. C-not change. D-increase.arrow_forward

- Suppose that a decrease in the price of X results in less of good Y sold. What are X and Y called? A. substitute goods B. complementary goods C. normal goods D. inferior goodsarrow_forwardA change of which of the following will not directly shift the demand curve for Regular Coke? Question 1 options: The price of regular Coke The price of diet Pepsi The price of diet Coke The income of the consumerarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education