Related questions

"Only answer c-d ones"

(a) Calculate the

The opportunity cost of producing one additional unit of good x in Home or foreign is the amount of good y that must be given up to produce it.

At Home, one worker can produce 2 units of good x or 1 unit of good y. Thus, to produce one additional unit of good x, half a unit of good y must be given up. The opportunity cost in Home is 0.5 units of good y. In Foreign, one worker can produce 1 unit of good x or 2 units of good y. To produce one additional unit of good x, two units of good y must be given up. The opportunity cost in Foreign is 2 units of good y.

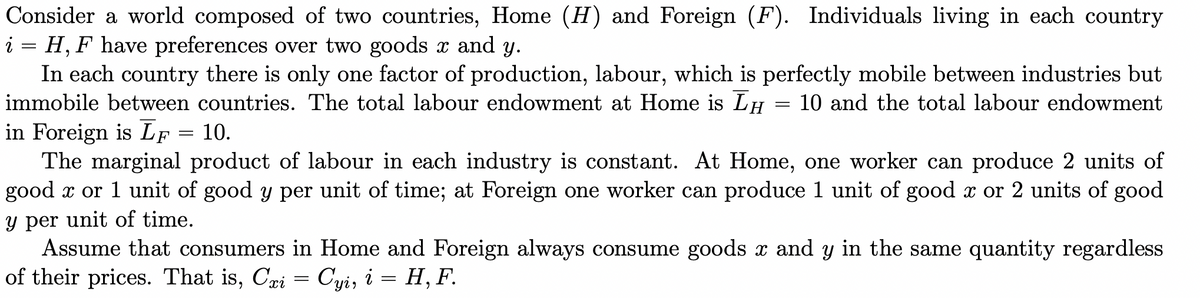

(b) Derive the production possibilities frontier (

To derive the production possibilities frontier (PPF) for Home and Foreign, we use the labor market clearing condition in each country.

For Home, the total labor endowment is LH = 10. In Home, 1 worker produces 2 units of good x (xH) and 1 unit of good y (yH). The labor market clearing condition in Home is: LH = (xH / 2) + yH. Rearrange this equation to get yH in terms of xH: yH = 10 - (xH / 2).

For Foreign, the total labor endowment is LF = 10. In Foreign, 1 worker produces 1 unit of good x (xF) and 2 units of good y (yF). The labor market clearing condition in Foreign is: LF = xF + (yF / 2). Rearrange this equation to get yF in terms of xF: yF = 20 - 2 * xF.

Both PPFs are linear, with negative slopes. We Plot the Home PPF using the equation yH = 10 - (xH / 2) and the Foreign PPF using the equation yF = 20 - 2 * xF to get the following graph below:

(c) Determine the

(d) Determine the optimal consumption and production at Home and Foreign under autarky. Depict this situation in a graph that includes each country's PPF and indifference

(e) Assume that Home and Foreign open to trade with each other. Explain how is the pattern of trade (which good will each country export and import) determined (Use the the Ricardian model, the pattern of trade is determined by

(f) Suppose that the equilibrium price of good x (keeping the price of good y as 1) is equal to 1. Determine the optimal production and consumption both at Home and Foreign when they open up to trade. Depict this in graph.

Step by stepSolved in 3 steps with 2 images

WHat are the graphs for both?

WHat are the graphs for both?

- 1. Suppose you have $1000 to spend on shirts and sweaters. The price of a shirt is $10, and the price of a sweater is $50. a. The opportunity cost of buying 1 shirt = __________ sweaters b. The opportunity cost of buying 1 sweater = __________shirtsarrow_forwardIce cream (millions of gallons per year) 5 A 4 В 3 2 3 4 Milk (millions of gallons per year) The figure above shows the production possibilities frontier for a country. The opportunity cost of a gallon of milk between combination point A and Bis A) 4 gallons of ice cream for a gallon of milk. B) 3 gallons of ice cream for a gallon of milk. C) 1 gallon of ice cream for a gallon of milk. D) 1/3 of a gallon of ice cream for a gallon of milk. E) zero because at point A, zero milk is being produced.arrow_forward1. Problems and Applications Q1 Yvette can read 40 pages of economics in an hour. She can also read 30 pages of sociology in an hour. She spends 4 hours per day studying. Use the blue line (circle symbol) to draw Yvette's production possibilities frontier (PPF) for reading economics and sociology. (?) 200 180 160 140 Economics Pages F 120 100 80 80 40 20 0 0 20 40 60 80 100 120 Sociology Pages 140 180 180 200 Yvette's opportunity cost of reading 90 pages of sociology is PPF pages of economics.arrow_forward

- -A) Describe production and the factors that go into producing various goods and services. -B) Describe the opportunity cost an economy incurs to increase the production of one product. Use a production possibilities frontierarrow_forward!arrow_forward1. If the economy is operating at point C in the PPF below, the opportunity cost of producing an additional 15 units of bacon is: Exhib: 6 50 40 30- A 20 10 D 20 20 40 50 60 (a) 40 eggs (b) 10 eggs (c) 20 eggs (d) 30 eggs (e) 50 eggs Explain: _ ||| 38 Egysarrow_forward

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education