ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

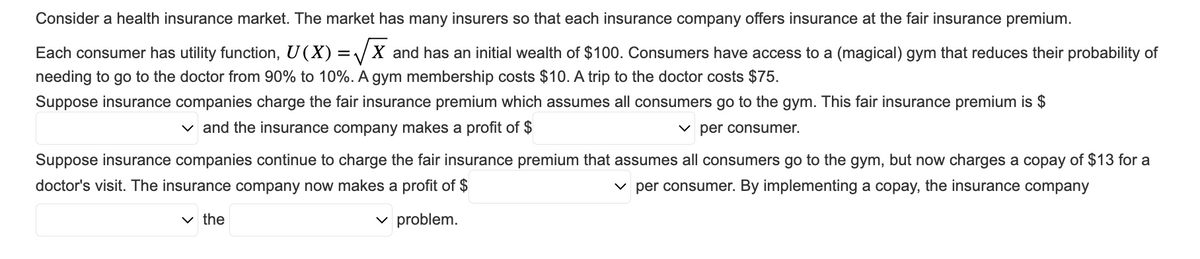

Transcribed Image Text:Consider a health insurance market. The market has many insurers so that each insurance company offers insurance at the fair insurance premium.

Each consumer has utility function, U(X) = √X and has an initial wealth of $100. Consumers have access to a (magical) gym that reduces their probability of

needing to go to the doctor from 90% to 10%. A gym membership costs $10. A trip to the doctor costs $75.

Suppose insurance companies charge the fair insurance premium which assumes all consumers go to the gym. This fair insurance premium is $

✓ and the insurance company makes a profit of $

✓per consumer.

Suppose insurance companies continue to charge the fair insurance premium that assumes all consumers go to the gym, but now charges a copay of $13 for a

doctor's visit. The insurance company now makes a profit of $

✓per consumer. By implementing a copay, the insurance company

✓ problem.

✓the

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider the lottery that assigns a probability T of obtaining a level of consumption CH and a probability 1-T an individual facing such a lottery with utility function u(c) that has the properties that more is better (that is, a strictly positive marginal utility of consumption at all levels of c) and diminishing marginal utility of consumption, u"(c) CL. Consider du(c) for the first derivative of the utility function with respect to dc du(c) du' (c) consumption and u"(c) (which is also the derivative of the first derivative of the utility function). to be the second derivative of the utility function dc dc2 1. Provide a definition for the certainty equivalent level of consumption for the simple lottery described above.arrow_forwardAn individual is off ered a choice of either $50 or a lottery which may result in $0 or $100, each with equal probability 1/2. If the individual has a utility function u(w) = w, which one would they choose? If the individual has a utility function u(w) =sqr(w)?arrow_forwardPersons A and B are roommates. Person A smokes and Person B does not. The index s measures how smoky the room is. It varies from s=0, where there is no smoke in the room, to s=1, when the room is filled with smoke. Thus, 1-s measures how "clean" the air in the room is. Person A's utility function is UA(XA,S)=XA+In(1+s), where xA is the amount of money Person A owns. Person B's utility function is uB(XB,1s)%3D3XB+2(1-s), where Xg is the amount of money Person B owns. Each person starts with an endowment of 5 units of money. Persch B has the legal right to a smoke-free room and there is a market for "emission right." At the Walrasian equilibrium, what will be the (per unit of smoke index) price p of the emission rights if the price of money is 1? O a. None of the other answers. O b. p=2/3 O c. p=1 O d. p=3/2 О е. р31/6arrow_forward

- Persons A and B are roommates. Person A smokes and Person B does not. The index s measures how smoky the room is. It varies from s=0, when there is no smoke in the room, to s=1, when the room is filled with smoke. Thus, 1-s measures how "clean" the air in the room is. Person A's utility function is ua(XA,s)=Xa.S, where xA is the amount of money Person A owns. Person B's utility function is ug(xg, 1s)=Xg .(1-s)³, where xg is the amount of money Person B owns. Each person starts with an endowment of 5 units of money. Person A has the legal right to a fill up the room with smoke and there exists a market for smoke "abatements". At the Walrasian equilibrium, how much money will person B be left with? а. Хв31.25 ОБ. Хв32.25 O c. XB=0.25 O d. Xg=0.25 е. None of the other answers.arrow_forwardShane just bought a house worth $360,000 in an area that is known for floods. A flood occurs with a 5% chance and if it occurs, his home is ✓ for reduced in value to $202,500. Shane has utility function given by U(X)=√√X. He would be willing to pay a maximum of flood insurance. The fair insurance premium for flood insurance is Shane's risk premium is Suppose, instead, that Shane's utility function is given by U(X) = X². Then, the maximum he would be willing to pay for flood insurance isarrow_forwardAn investor has preferences represented by a utility function u(c) and initial wealth w > 0. Consider an asset that pays G with probability \pi and B with probability 1-\pi. 1.1 Suppose the investor owns this asset. What is the minimum price he would sell it for? (It is sufficient to formulate the condition that this price must satisfy). 1.2 Suppose he does not own it. What is the maximum price he would be willing to pay to buy it? (It is sufficient to formulate the condition that this price must satisfy). 1.3 Explain why (or under which conditions) the buy and sell prices you have found are or are not the same. 1.4 Suppose w = 10, G = 10, B = 5 and u(c) = √c. Compute the buy and sell prices.arrow_forward

- Priyanka has an income of £90,000 and is a von Neumann-Morgenstern expected utility maximiser with von Neumann-Morgenstern utility index . There is a 1 % probability that there is flooding damage at her house. The repair of the damage would cost £80,000 which would reduce the income to £10,000. a) Would Priyanka be willing to spend £500 to purchase an insurance policy that would fully insure her against this loss? Explain. b) What would be the highest price (premium) that she would be willing to pay for an insurance policy that fully insures her against the flooding damage?arrow_forwardConsider two lotteries. Lottery A is such that an individual receives a prize of 1.25 units of a consumption good with 50% probability and 0.75 units of the consumption good with 50% probability. Lottery B presents the winner with a prize of 1.5 units of a consumption good with 50% probability and a prize of 0.5 units of the consumption good with 50% probability.arrow_forward1. ) Suppose a driver has a 6% of having one accident a year. In case of an accident the value of the car is reduced from $25,000 to $5,000. If driver buys an insurance policy the insurance company would completely cover damage to the car (essentially restoring its value to its initial level). Assume that the driver's utility function is U = VW. a) If price of the insurance policy (premium) is $1500, would this driver be willing to purchase the policy? Explain Show you computations b) What would be the maximum price a driver with 10% chance of accident be willing to pay for the insurance policy?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education