ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

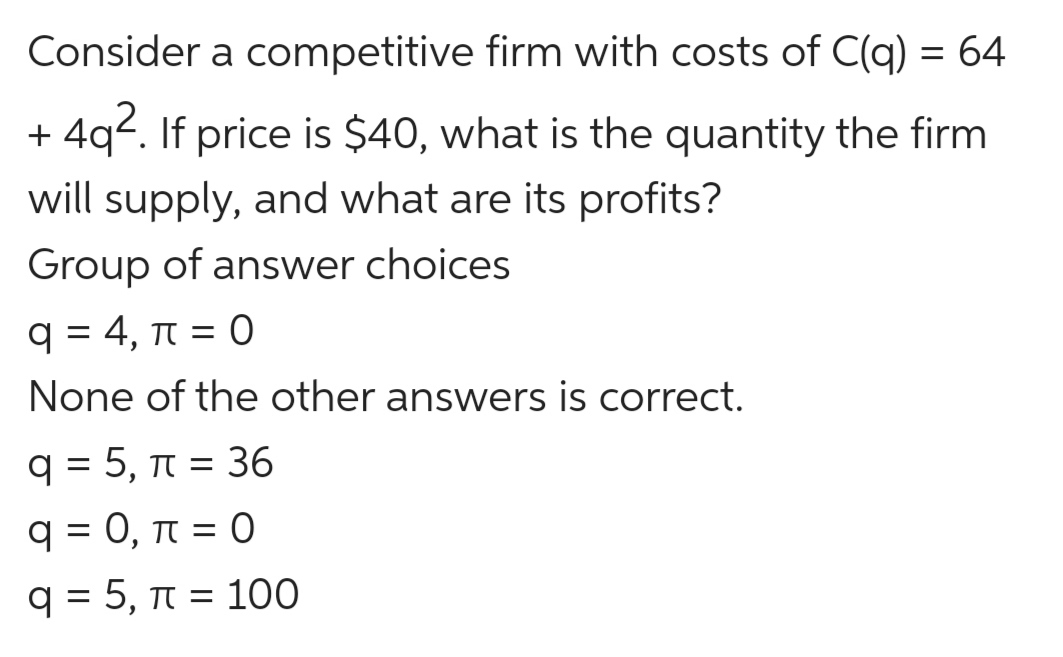

Transcribed Image Text:Consider a competitive firm with costs of C(q) = 64

4q2. If price is $40, what is the quantity the firm

+

will supply, and what are its profits?

Group of answer choices

q = 4, T = 0

None of the other answers is correct.

q = 5, T = 36

%3D

q = 0, t = 0

q = 5, n = 100

%D

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Each firm in a perfectly competetive market has a long-run total cost of LRTC = 100g – 10q + 100. The market demand is Q* = 2150 – 5P. At the long-run equilibrium price, how many firms will there be in the market? (а) 500 (b) 1,000 (c) 1,200 (d) 2,000 (e) 2,400arrow_forwardSuppose a large of firms have cost function C(q ) = = 72+ 4q+2q 2 and the market demand Q_{D = 712 4p What is equilibrium and the long-run number of firms? (a) Q = 600 and N = 100 (b) Q 688 and V100 (c) Q = 600 and N = = 688 and N = 115 (e) None of the above 115 (d) Qarrow_forwardThe Lead Zeppelin Company produces powered and steerable lighter-than-air craft. The company’s airships are specially lined and are therefore safer than normal dirigibles. The table below shows the weekly production of dirigibles, along with the associated Average Cost and Total Revenue figures (the Average Cost and Total Revenue figures are actually in thousands of dollars, so the $15 represents $15,000, but we have left off the zeros to save space). Quantity Average Cost Total Cost Total Revenue 0 -- 0 $0 1 $15 15 $10 2 $9 18 $20 3 $8 24 $30 4 $8.50 34 $40 5 $9 45 $50 6 $10 60 $60 7 $12 84 $70 The Lead Zeppelin Company has decided that it will produce at least 1 dirigible. Now the question becomes, how many more dirigibles should it produce to make as much profit as possible? Use the profit-maximizing rule to explain how many dirigibles the Lead Zeppelin Company should produce to…arrow_forward

- The Jones are small farmers in the wheat industry – they are price takers. Their cost function is: TC = 600,000 + 3,000Q + Q2 and MC = 3,000 + 2Q. The market price is $5,000 per ton. Assuming the Jones are maximizing profits (or minimizing loses), how much profit are they making? You must show your work.arrow_forwardDetermining the Effect of Taxes on a Market Suppose all firms in a constant cost industry have identical costs of C(q)=5q²+6q+20. The market demand is Qo=256 – 2p. (a) Find the long-run equilibrium: Q*, q*, p*, and N*. (b) Suppose the government restricts the market to 41 firms. To do so, firms are required to get i permit to operate, but only 41 permits are issued in total. Find the equilibrium price and quantity. (c) Suppose instead of permits, the government simply charges all firms a fixed fee to operate of F=60. What is the resulting equilibrium price, quantity, and number of firms?arrow_forwardA competitive firm faces the following market price: P=200. Variable costs are C(Q)=Q^2. The firm also pays $17000 in costs that do not depend on production (even if q=0). Hint – marginal cost is MC(Q)=2*Q NOTE - KEEP YOUR CALCULATIONS. THIS INFORMATION WILL BE USED IN MULTIPLE QUESTIONS What is the optimal quantity this firm should produce? Question 6 options: 0 50 200 100arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education