ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

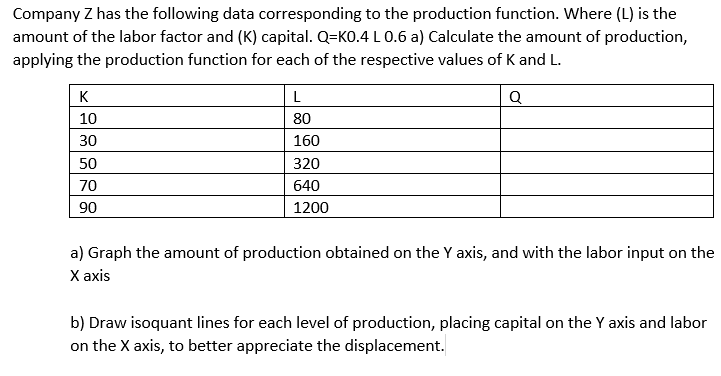

Transcribed Image Text:Company Z has the following data corresponding to the production function. Where (L) is the

amount of the labor factor and (K) capital. Q=K0.4 L 0.6 a) Calculate the amount of production,

applying the production function for each of the respective values of K and L.

K

L

Q

10

80

30

160

50

320

70

640

90

1200

a) Graph the amount of production obtained on the Y axis, and with the labor input on the

Х аxis

b) Draw isoquant lines for each level of production, placing capital on the Y axis and labor

on the X axis, to better appreciate the displacement.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 5 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A small clothing manufacturer employs a production method that is approximated by the following production function: q=12KL², where L measures the number of labor hours and K measures the number of rental hours for the machines used in the clothing construction process. Does this production process exhibit increasing, decreasing, or constant returns to scale? Briefly explain your answer. The hourly wage rate for workers at this company is $15; and the rental cost on the machines is $75 per hour. The company has a total budget of $3,150 that it can allocate to cover weekly production costs. The goal of the company's owner is to maximize their output, subject to the constraint of their production budget. Determine the output-maximizing levels of labor and capital the owner will employ.arrow_forwardConsider the following production function when K is fixed. (This is a description of the figure: it shows a two-axis graph; in the horizontal axis we measure labor and in the vertical axis we measure meals; the graph of the production function is a line that intersects the vertical axis at a positive amount; this graph is a line with positive slope and passes through the point (4,300)). Can we say that the production function satisfies the law of decreasing marginal returns of labor?True Falsearrow_forwardFor the production function Qs = K0.4L0.1 find the returns to scale, recall that a doubling of inputs that doulbes output is a CONSTANT returns to scale = 1.0 Please enter your response as a positive number with 1 decimal and 5/4 rounding (e.g. 1.15 = 1.2, 1.14 = 1.1).arrow_forward

- Suppose that a firm's production function is given by the following relationship: Q = 2.5√/LK (i.e., Q = 2.5L0.5 K0.5) where is output, L is labor input, and K is capital input. What is the percentage increase in output if labor input is increased by 10%? (Assume that capital input is held constant.) What is the percentage increase in output if capital input is increased by 25%? (Assume that labor input is held constant.) What is the the percentage increase in output if both labor and capital are increased by 10%? 11arrow_forwardA firm's production function is given by Q = 20L0.8 K0.2. At that moment, the firm sets = 1,000 and K = 1,000. Which of the following combinations of L and Klies on the same isoquant? L = 1,063.9; K = 698.7 L= 1,063.9; K = 698.7 L=698.7; K = 1,063.9 L = 1,302.3; K = 936.1 L 936.1; K 1,302.3arrow_forwardThe Cobb-Douglas production function is a classic model from economics used to model output as a function of capital and labor. It has the form f(L, C) = c₂LC1C²2 C2 are constants. The variable L represents the units of input of labor and the variable C represents the units of input of capital. (a) In this example, assume co 5, C₁ = 0.25, and c2₂ 0.75. Assume each unit of labor costs $25 and each unit of capital costs $75. With $90,000 available in the budget, develop an optimization model for determining how the budgeted amount should be allocated between capital and labor in order to maximize output. = = where co, C₁, and Max s.t. L, C ≥ 0 A ≤ 90,000 (b) Find the optimal solution to the model you formulated in part (a). What is the optimal solution value (in dollars)? Hint: Put bound constraints on the variables based on the budget constraint. Use L ≤ 3,000 and C ≤ 1,000 and use the Multistart option as described in Appendix 8.1. (Round your answers to the nearest integer when…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education