Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

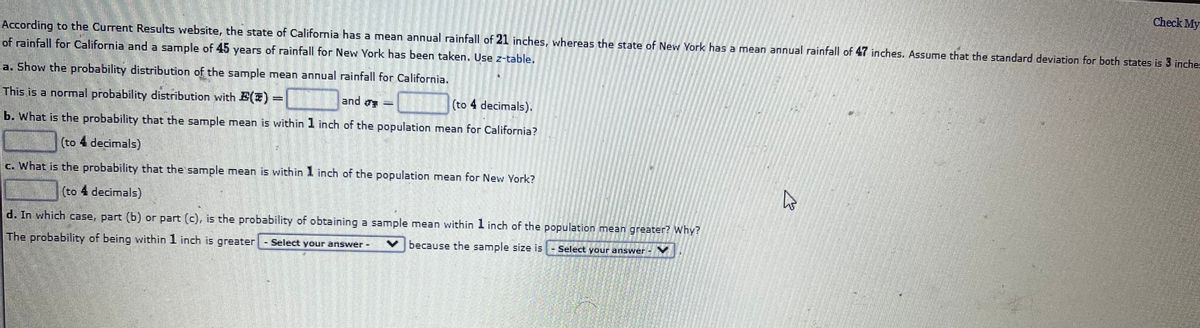

Transcribed Image Text:Check My

According to the Current Results website, the state of California has a mean annual rainfall of 21 inches, whereas the state of New York has a mean annual rainfall of 47 inches. Assume that the standard deviation for both states is 3 inches

of rainfall for California and a sample of 45 years of rainfall for New York has been taken. Use z-table.

a. Show the probability distribution of the sample mean annual rainfall for California.

This is a normal probability distribution with E(E)

and os

(to 4 decimals).

b. What is the probability that the sample mean is within 1 inch of the population mean for California?

(to 4 decimals)

c. What is the probability that the sample mean is within1 inch of the population mean for New York?

(to 4 decimals)

d. In which case, part (b) or part (c), is the probability of obtaining a sample mean within I inch of the population mean greater? Why?

because the sample size is

-Seléct your answer - Y

Select your answer-

|The probability of being within 1 inch is greater

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Similar questions

- Using the following returns, calculate the arithmetic average returns, the variances, and the standard deviations for X and Y. Year Returns X Y 1 9% 23% 2 27 44 3 16 -6 4 -17 -20 5 18 52 Calculate the arithmetic average return for X. Calculate the arithmetic average return for Y.arrow_forwardUse the following returns for X and Y. Year 1 2 3 4 5 Returns X 22.1% -17.1 10.1 20.2 5.1 Y 27.3% -4.1 29.3 -15.2 33.3 a. Calculate the average returns for X and Y. Note: Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16. b. Calculate the variances for X and Y. Note: Do not round intermediate calculations and round your answers to 6 decimal places, e.g., .161616. c. Calculate the standard deviations for X and Y. Note: Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16. X Answer is complete but not entirely correct. X 8.06 a. Average return b. Variance c. Standard deviation 136.454400 % 11.67 X % Y 14.04 377.286400 x % 19.42%arrow_forwardUse the following returns for X and Y. Returns Year x y 1 21.8% 26.4% 2 -16.8 -3.8 3 9.8 28.4 4 19.6 -14.6 5 4.8 32.4 a. Calculate the average returns for X and Y. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) b. Calculate the variances for X and Y. (Do not round intermediate calculations and round your answers to 6 decimal places, e.g., 32.161616.) c. Calculate the standard deviations for X and Y. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.)arrow_forward

- Over the past four days, the realized values of the random variable A are: 8, -2, 2 and 11. In the same order, the realized values of the random variable B are: 6, 2, 2 and -10. Compute the correlation between A and B.arrow_forwardConsider a population proportion p = 0.20. a. What are the expected value and the standard error for the sampling distribution of the sample proportion with n = 20 and n = 58? Note: Round the standard error to 4 decimal places. Answer is complete and correct. n Expected value Standard error 20 58 0.20 0.20 0.0894 0.0525 b. Can you conclude that the sampling distribution of the sample proportion is approximately normally distributed for both sample sizes? Yes, the sampling distribution of the sample proportion is normally distributed for both sample sizes. No, the sampling distribution of the sample proportion is not normally distributed for either sample size. No, only the sample proportion with n = 20 will have a normal distribution. No, only the sample proportion with n = 58 will have a normal distribution. c. If the sampling distribution of the sample proportion is normally distributed with n = 20, then calculate the probability that the sample proportion is between 0.18 and 0.20.…arrow_forwardFind the mean, variance, and standard deviation of the binomial distribution with the given values of n and p. n= 124, p = 0.56arrow_forward

- 4. Using the following returns, calculate the arithmetic average returns, the variances, and the standard deviations for X and Y. Year 1 2 3 4 5 X 12% 28% 9% -7% 10% Return Y 25% 34% 13% -27% 14%arrow_forwardExpected Return, Variance, Std. Deviation and Cofficient of Variation:Magee Inc.'s manager believes that economic conditions during the next year will be strong, normal, or weak, and she thinks that the firm's returns will have the probability distribution shown below. What's the standard deviation of the estimated returns?Round your answer to two decimal places. For example, if your answer is $345.6671 round as 345.67 and if your answer is .05718 or 5.7182% round as 5.72. State of the Economy Probability of State Occurring Stock's Expected Return Boom 20% 24.15% Normal 50% 13.50% Recession 30% –13.30% Group of answer choices 15.68% 16.39% 14.26% 13.54% 10.69%arrow_forwardUsing the following annual returns, calculate the estimates of the arithmetic mean returns, the variances, and the standard deviations for assets X and Y. Also calculate the estimates of the covariance and correlation between X and Y. These five years are a sample of the entire population of returns for X and Y. Year 2001 2002 2003 2004 2005 Returns X 11% 6% -8% 28% 13% Y 36% -7% 2% -12% 43% A stock has had returns over the past six years of 29%, 14%, 23%, -18%, 9%, and -14%. What was its arithmetic mean and geometric mean returns over that period? What was the standard deviation of its returns over this six-year period?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education