Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

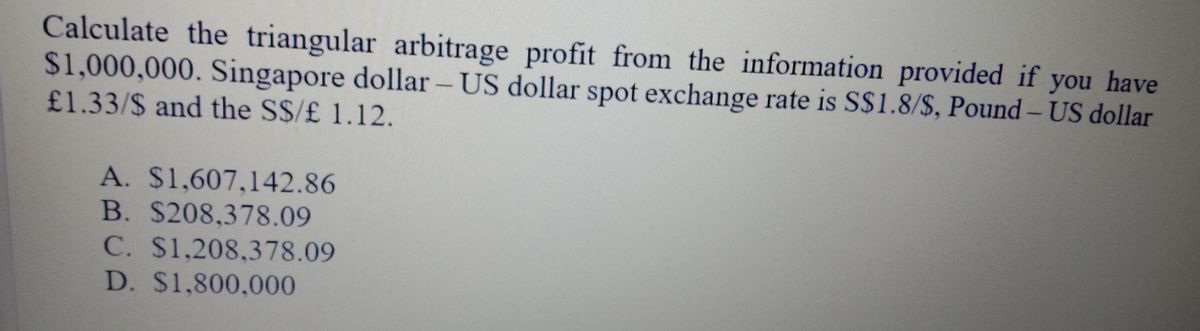

Transcribed Image Text:Calculate the triangular arbitrage profit from the information provided if you have

$1,000,000. Singapore dollar – US dollar spot exchange rate is S$1.8/$, Pound – US dollar

-

£1.33/$ and the S$/£ 1.12.

A. $1,607,142.86

B. $208,378.09

C. $1,208,378.09

D. $1,800,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Calculate the possible rate for buying GBP (Great Britain Pound) in exchange for selling JPY as well as the possible rate for selling GBP in exchange for buying JPY. Assume that the exchange rates are quoted as follows: USD 1 = JPY 104.50-104.60, GBP 1 = USD 1.3260 – 1.3265.arrow_forwardThe following exchange rates are available to you. • Bank Quotation Fuji Bank, Tokyo Y120/$ • Credit Suisse First Boston, New York SF 1.60/$ Swiss First Bank, Zurich 83/ SF • Assume that you have an initial USD 10,000,000. What is the profit in USD from Triangular Arbitrage Show all working a. $66,666.67 b. $1,066,666 $533333 C. d. $75000arrow_forwardQ4) Assume the current U.S. dollar-yen spot rate is 109.00¥/$. Further, the current nominal 360-day rate of return in Japan is 0.10% and 1.95% in the United States. What is the approximate forward exchange rate for 360 days? A) 110.85¥/$ 109.00¥/$ 107.02\/$ 111.01\/$arrow_forward

- K (Foreign exchange arbitrage) You own $7,000. The dollar rate in Tokyo is ¥215.9372/$. The yen rate in New York is given in the following table: Selling Quotes for Foreign Currencies in New York Country-Currency Japan-yen Contract Spot 30-day 90-day (Click on the icon in order to copy its contents into a spreadsheet.) Are arbitrage profits possible? Set up an arbitrage scheme with your capital. What is the gain in dollars? The net View an example $/Foreign Currency "Assuming no transaction costs, the rates in Tokyo and New York are out of line. Therefore, arbitrage profits are possible." The statement above is true (Select from the drop-down menu.) 0.004698 0.004741 0.004782 Get more help - ... from arbitrage would be $ (Round to the nearest cent.) Clear all Check answerarrow_forwardD3)arrow_forwardAssume that you are a retail customer. Use the information below to answer the following question. Exchange Rate - Bid Exchange Rate - Ask Interest Rate APR S0($/€) $ 1.42 = € 1.00 $ 1.45 = € 1.00 i$ 4 % F360($/€) $ 1.48 = € 1.00 $ 1.50 = € 1.00 i€ 3 % If you had borrowed $1,000,000, traded them for euros at the spot rate, and invested those euros in Europe, how many euros do you receive in one year?arrow_forward

- TB SA Qu. 06-69 If you had borrowed $1,000,000.... Use the information below to answer the following question. Exchange Rate $ 1.60 €1.00 $1.58 € 1.00 So ( $/ €) F360 ($/C) Interest Rate is ic APR 28 4% If you had borrowed $1,000,000, traded them for euro at the spot rate, and invested those euros in Europe, how many euros will you receive in one year?arrow_forwardSuppose that in the Moscow interbank market one ruble corresponds to 0.0135 euros and 1.5 yen, while in the Tokyo interbank market 100 yen equals 0.8 euros. Consider whether there is a possibility of Triangular Arbitrage.arrow_forwardIf the ratio between direct quote of forward divided by spot exchange rates of US $ over Mexican Peso is 0.95 and the interest rate in the US is 4%, then the interest rate in Mexico is expected to be:(Please show work) A) -1.2% B) 3% C) 4% D) 2% E) 5%arrow_forward

- Please use the data below, to answer the following question. BigMac price in the US BigMac price in Mexico Current Exchange Rate O overvalued by 14.29% O undervalued by 14.29% O overvalued by 12.50% O undervalued by 12.50% USD 3.50 12 MXN 80 Based on PPP, the MXN is 1 USD - MXN 20 140 15 16 (2 hparrow_forwardFrom the following data provided, ascertain what would be the exchange rates that the Bank would quote for an FDI transaction amounting to USD 2 Mn for value cash basis, assuming a margin of 3 paise where., Spot USD/INR = 75.0900/75.1000 ., Cash/Spot : 4/5 paise. Arrive at the exchange rate up to 4 decimal places. Adhere to the steps involved in calculation.arrow_forwardVALUE OF EURO (U.S. dollars per euro) 1.9 1.8 1.7 1.6 1.5 1.4 1.3 1.2 1.1 0 50 100 150 200 250 300 350 400 450 500 550 600 QUANTITY OF EUROS (Billions) At an exchange rate of 1.5 per euro, the quantity of euros demanded is of euros demanded is + (?) billion euros, while at an exchange rate of 1.1 per euro, the quantity sloping. billion euros. This confirms that the demand curve for euros isarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education