FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

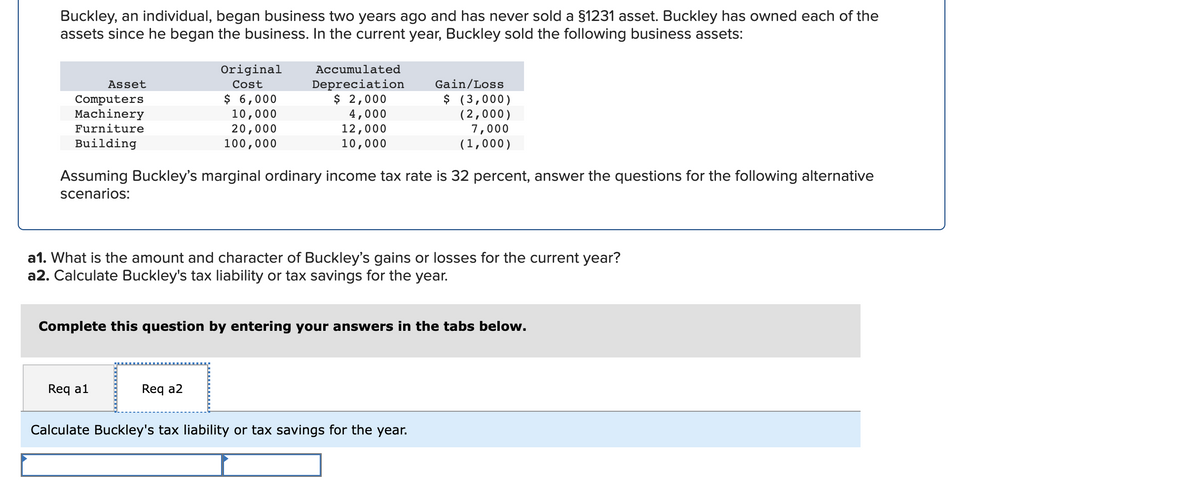

Transcribed Image Text:Buckley, an individual, began business two years ago and has never sold a §1231 asset. Buckley has owned each of the

assets since he began the business. In the current year, Buckley sold the following business assets:

Original

Accumulated

Gain/Loss

Depreciation

$ 2,000

4,000

12,000

10,000

Asset

Cost

Computers

Machinery

Furniture

$ 6,000

10,000

20,000

100,000

$ (3,000)

(2,000)

7,000

(1,000)

Building

Assuming Buckley's marginal ordinary income tax rate is 32 percent, answer the questions for the following alternative

scenarios:

a1. What is the amount and character of Buckley's gains or losses for the current year?

a2. Calculate Buckley's tax liability or tax savings for the year.

Complete this question by entering your answers in the tabs below.

Req al

Req a2

Calculate Buckley's tax liability or tax savings for the year.

Transcribed Image Text:Buckley, an individual, began business two years ago and has never sold a §1231 asset. Buckley has owned each of the

assets since he began the business. In the current year, Buckley sold the following business assets:

Original

Accumulated

Gain/Loss

Depreciation

$ 2,000

4,000

12,000

10,000

Asset

Cost

Computers

Machinery

Furniture

$ 6,000

10,000

20,000

100,000

$ (3,000)

(2,000)

7,000

(1,000)

Building

Assuming Buckley's marginal ordinary income tax rate is 32 percent, answer the questions for the following alternative

scenarios:

a1. What is the amount and character of Buckley's gains or losses for the current year?

a2. Calculate Buckley's tax liability or tax savings for the year.

Complete this question by entering your answers in the tabs below.

Req a1

Req a2

What is the amount and character of Buckley's gains or losses for the current year?

Description

Amount

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- During the current year, Jean and Steve sold the following assets and made the following gains and losses. Capital asset. Capital gain/loss. Type A stock. $35,000. long 0/15/20% B stock. (8,000). short Antiques. 5,000. long 28% Rental home. 100,000. long 25% and 0/15/20% *40,000 of the gain is 25 percent gain from accumulated depreciation on the property. i)Complete the capital gains and losses netting process and determine the maximum tax rates applicable to the gains. ii) Given that Jean and Steve have taxable income of $450,000 before considering the sales above, what is their gross tax liability for 2021 assuming they file a joint return?arrow_forwardShimmer Inc. is a calendar-year-end, accrual-method corporation. This year, it sells the following long-term assets: Asset Sales Price Cost Accumulated Depreciation Building $752,000 $749,000 $34,000 Sparkle Corporation stock 219,000 256,000 n/a Shimmer does not sell any other assets during the year, and its taxable income before these transactions is $847,000. What are Shimmer's taxable income and tax liability for the year? Taxable income: Tax Liability:arrow_forwardConvers Corporation (calendar year-end) acquired the following assets during the current tax year: (ignore §179 expense and bonus depreciation for this problem): (Use MACRS Table 1, Table 2, and Table 5.) Asset Date Placed in Service Original Basis Machinery October 25 $ 104,000 Computer equipment February 3 44,000 Delivery truck* March 17 57,000 Furniture April 22 184,000 Total $ 389,000 *The delivery truck is not a luxury automobile. In addition to these assets, Convers installed qualified real property (MACRS, 15 year, 150% DB) on May 12 at a cost of $640,000. b. What is the allowable MACRS depreciation on Convers's property in the current year assuming Convers does not elect out of bonus depreciation (but does not take §179 expense)? Note: Round your intermediate calculations to the nearest whole dollar amount. Table 1 MACRS Half-Year Convention Depreciation Rate for Recovery Period 3-Year 5-Year 7-Year 10-Year 15-Year 20-Year Year 1 33.33%…arrow_forward

- Sergio, a sole proprietor, purchased a van for $35,000 to use exclusively in his delivery business. Six months later, he sold the van for $38,000. Sergio's $3,000 gain from the sale of this property should be reported as: O Gross receipts or sales on Schedule C, Part I. A gain from the sale or exchange of property used in a trade or business on Form 4797, Part I. An ordinary gain on Form 4797, Part II. O A gain from the disposition of property on Form 4797, Part III.arrow_forwardBrandon an individual, began business four years ago and has sold 1231 assets with $5,700 of losses within the last 5 years. Brandon owned each of the assets for several years. In the current year,Brandon sold the following business assets: Asset original cost accumulated deprection gain/loss Machinery $31,400 $8,400 $10,700 Land 54,000 0 27,000 Building 118,000 34,000 (10,000) Assuming Brandon's marginal ordinary income tax rate is 32 percent, what effect do the gains and losses have on Brandon's tax liability? Use dividends and capital gains tax rates for reference.arrow_forwardA piece of land personally owned by John was transferred to the business for the use of its operation. The land was acquired 2 years ago with a cost of $50,000. The market value as of this date is $75,000.arrow_forward

- Timmy paid $800,000 cash for all of the assets of Bob’s Chicken Fried Steak Shack, Inc. (Bob’s). Timmy did not buy the stock of Bob’s; rather he bought all of Bob’s assets from Bob’s. Here is a list of the physical assets that Timmy got for his $800,000, showing the stand-alone FMV of each category:*** Land & Building, $350,000 Furniture & Equipment, $160,000 Inventory, $15,000 Bob’s latest property tax appraisal from Dallas County showed the land value at $150,000, the building at $100,000, the furniture and equipment at $75,000. What is Timmy’s depreciable basis in the building? What is Timmy’s depreciable basis in the furniture and equipment? What amount will Timmy eventually record as COGS with respect to the purchased inventory? How much, if any, goodwill did Timmy purchase? Address each item separately. (Each part must be correctly answered to earn a point for this item (3).) *** These FMVs are as agreed and stated in the negotiated Purchase Agreement.arrow_forwardConvers Corporation (calendar year-end) acquired the following assets during the current tax year: (ignore §179 expense and bonus depreciation for this problem): (Use MACRS Table 1, Table 2 and Table 5.) Asset Date Placed in Service Original Basis Machinery October 25 $ 78,000 Computer equipment February 3 18,000 Delivery truck* March 17 31,000 Furniture April 22 158,000 Total $ 285,000 *The delivery truck is not a luxury automobile. In addition to these assets, Convers installed new flooring (qualified improvement property) to its office building on May 12 at a cost of $380,000. a. What is the allowable MACRS depreciation on Convers’s property in the current year assuming Convers does not elect §179 expense and elects out of bonus depreciation? (Round your intermediate calculations and final answer to the nearest whole dollar amount.) b. What is the allowable MACRS depreciation on Convers's property in the current year assuming Convers does not elect out of…arrow_forwardLowes Corporation sold its storage building for $86,000 cash. Lowes originally purchased the building for $200,000, and depreciation through the date of sale totaled $120,000. Required:Prepare the journal entry to record the sale of this building. (A separate calculation of any gain or loss is recommended.)arrow_forward

- John’s uncle donated a truck to his company, John’s Corporation. The truck had an original cost of $95,000, a book value of $40,000, and a fair value of $55,000. The journal entry by John’s Corporation to record this donated asset will include a a. debit Truck for $60,000 and credit Gain for $20,000. b. debit Truck for $55,000 and credit Gain for $55,000. c. debit Truck for $95,000 and credit Gain for $95,000. d. debit Truck for $60,000 and credit Gain for $60,000.arrow_forward7. Gibby sold 4-year-old business machinery for $100,000.The machinery had an original cost of $ 80,500. Gibby claimed$ 12,500 in depreciation through the date of sale. The only other§ 1231 transactions H has had were in the two prior years. Hehad a §1231 gain of $3,500 two years ago and a §1231 loss of$12,000 last year. How are Gibby’s gains for the current yeartreated?a. $12,500 ordinary gain; $19,500 long-term capital gainb. $21,000 ordinary gain; $11,000 long-term capital gainc. $24,500 ordinary gain; $7,500 long-term capital gaind. $32,000 ordinary gaine. $32,000 long term capital gainarrow_forwardBrandon, an individual, began business four years ago and has sold §1231 assets with $5,550 of losses within the last five years. Brandon owned each of the assets for several years. In the current year, Brandon sold the following business assets: Asset Original Cost Accumulated Depreciation Gain/Loss Machinery $ 31,100 $ 8,100 $ 10,550 Land 51,000 0 25,500 Building 112,000 31,000 (16,000 ) Assuming Brandon's marginal ordinary income tax rate is 32 percent, what effect do the gains and losses have on Brandon's tax liability? Use dividends and capital gains tax rates for reference.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education