FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

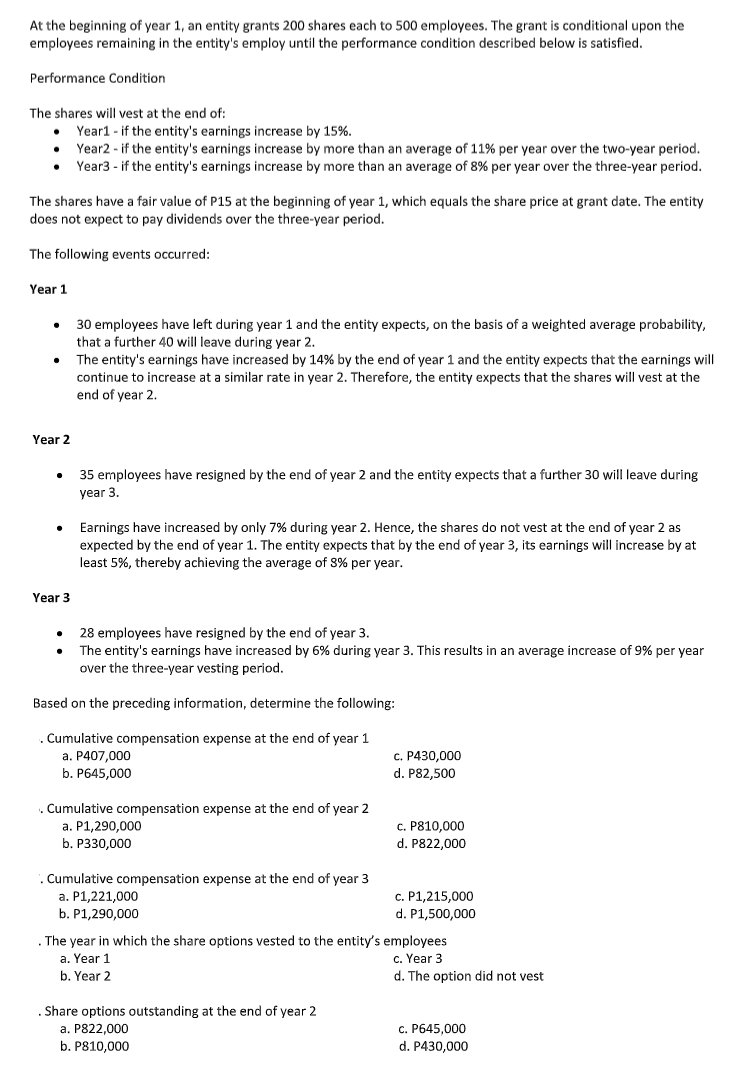

Transcribed Image Text:At the beginning of year 1, an entity grants 200 shares each to 500 employees. The grant is conditional upon the

employees remaining in the entity's employ until the performance condition described below is satisfied.

Performance Condition

The shares will vest at the end of:

Year1 - if the entity's earnings increase by 15%.

• Year2 - if the entity's earnings increase by more than an average of 11% per year over the two-year period.

Year3 - if the entity's earnings increase by more than an average of 8% per year over the three-year period.

The shares have a fair value of P15 at the beginning of year 1, which equals the share price at grant date. The entity

does not expect to pay dividends over the three-year period.

The following events occurred:

Year 1

30 employees have left during year 1 and the entity expects, on the basis of a weighted average probability,

that a further 40 will leave during year 2.

The entity's earnings have increased by 14% by the end of year 1 and the entity expects that the earnings will

continue to increase at a similar rate in year 2. Therefore, the entity expects that the shares will vest at the

end of year 2.

Year 2

35 employees have resigned by the end of year 2 and the entity expects that a further 30 will leave during

year 3.

Earnings have increased by only 7% during year 2. Hence, the shares do not vest at the end of year 2 as

expected by the end of year 1. The entity expects that by the end of year 3, its earnings will increase by at

least 5%, thereby achieving the average of 8% per year.

Year 3

28 employees have resigned by the end of year 3.

The entity's earnings have increased by 6% during year 3. This results in an average increase of 9% per year

over the three-year vesting period.

Based on the preceding information, determine the following:

Cumulative compensation expense at the end of year 1

a. P407,000

b. P645,000

с. Р430,000

d. P82,500

Cumulative compensation expense at the end of year 2

c. P810,000

a. P1,290,000

b. Р330,000

d. P822,000

Cumulative compensation expense at the end of year 3

а. Р1,221,000

b. P1,290,000

c. P1,215,000

d. P1,500,000

The year in which the share options vested to the entity's employees

c. Year 3

a. Year 1

b. Year 2

d. The option did not vest

Share options outstanding at the end of year 2

а. Р822,000

c. P645,000

b. P810,000

d. P430,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 6 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- 23. A company grants 100 Share appreciation rights (SAR), payable in cash, to an employee on 1/1/Y1. The predetermined amount for the SAR plan is P50 per right, and the market value of the stock is P55 on 12/31/Y1, P53 on 12/31/Y2, and P61 on 12/31/Y3. The plan had a two-year service period. Compensation expense in year 3?arrow_forwardOn January 1, 2023, Pyxis Company issued share appreciation rights to its president exercisable for one year beginning January 1, 2025 provided that the president is still in the employ of the company at that date of exercise. Each right provides for a cash payment equal to the excess of the entity’s share price over P50. The equivalent number of shares for share appreciation rights will be based on the level of sales at the date of exercise. The number of equivalent shares is 20,000 if the level of sales is P4,000,000 to P6,000,000 and 30,000 shares if the level of sales is over P6,000,000. The actual sales achieved totaled P5,000,000 in 2023 and P7,000,000 in 2024. The share prices are P70 in 2023 and P65 in 2024. What is the compensation expense for 2023? ANSWER: 200,000 What is the compensation expense for 2024? ANSWER: 150,000 Show full solutionarrow_forwardHammond Manufacturing Inc. was legally incorporated on January 2, 2020. Its articles of incorporation granted it the right to issue an unlimited number of common shares and 100,000 shares of $14.0 non-cumulative preferred shares. The following transactions are among those that occurred during the first three years of operations: 2020 Jan. 12 Issued 40,300 common shares at $4.4 each. 20 Issued 6,000 common shares to promoters who provided legal services that helped to establish the company. These services had a fair value of $32,000. 31 Issued 76,000 common shares in exchange for land, building, and equipment, which have fair market values of $356,000, $476,000, and $44,000, respectively. Mar. 4 Purchased equipment at a cost of $8,120 cash. This was thought to be a special bargain price. It was felt that at least $10,400 would normally have had to be paid to acquire this equipment. Dec. 31 During 2020, the company incurred a loss of $92,000. The Income Summary account was closed. 2021…arrow_forward

- Hammond Manufacturing Inc. was legally incorporated on January 2, 2020. Its articles of incorporation granted it the right to issue an unlimited number of common shares and 100,000 shares of $14.0 non-cumulative preferred shares. The following transactions are among those that occurred during the first three years of operations: 2020 Jan. 12 Issued 40,300 common shares at $4.4 each. 20 Issued 6,000 common shares to promoters who provided legal services that helped to establish the company. These services had a fair value of $32,000. 31 Issued 76,000 common shares in exchange for land, building, and equipment, which have fair market values of $356,000, $476,000, and $44,000, respectively. Mar. 4 Purchased equipment at a cost of $8,120 cash. This was thought to be a special bargain price. It was felt that at least $10,400 would normally have had to be paid to acquire this equipment. Dec. 31 During 2020, the company incurred a loss of $92,000. The Income Summary account was closed. 2021…arrow_forward6arrow_forwardSubject - accountarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education