ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

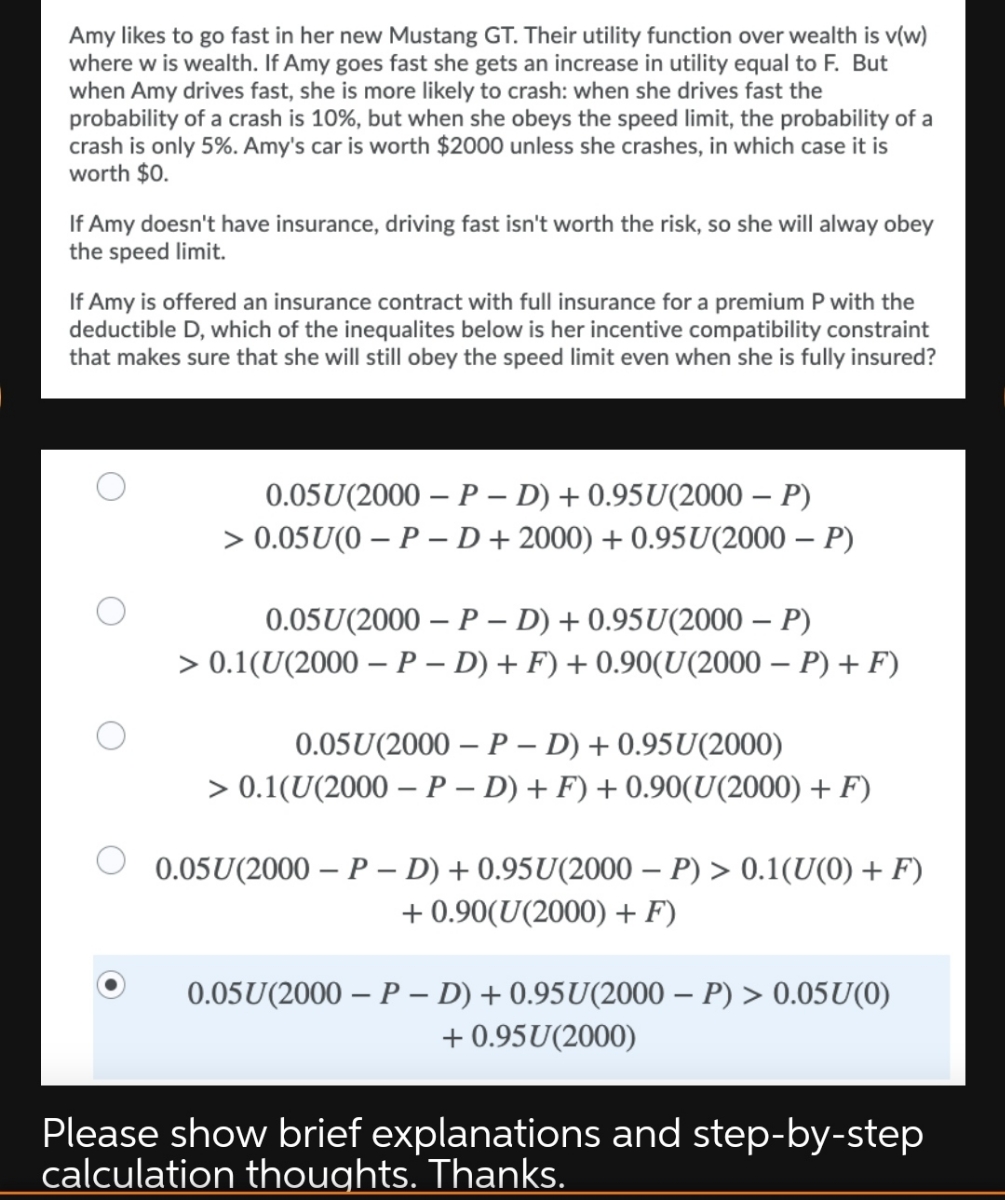

Transcribed Image Text:Amy likes to go fast in her new Mustang GT. Their utility function over wealth is v(w)

where w is wealth. If Amy goes fast she gets an increase in utility equal to F. But

when Amy drives fast, she is more likely to crash: when she drives fast the

probability of a crash is 10%, but when she obeys the speed limit, the probability of a

crash is only 5%. Amy's car is worth $2000 unless she crashes, in which case it is

worth $0.

If Amy doesn't have insurance, driving fast isn't worth the risk, so she will alway obey

the speed limit.

If Amy is offered an insurance contract with full insurance for a premium P with the

deductible D, which of the inequalites below is her incentive compatibility constraint

that makes sure that she will still obey the speed limit even when she is fully insured?

0.05U(2000 – P – D) + 0.95U(2000 – P)

> 0.05U(0 – P – D + 2000) + 0.95U(2000 – P)

0.05U(2000 – P – D) + 0.95U(2000 – P)

> 0.1(U(2000 – P – D) + F) + 0.90(U(2000 – P) + F)

0.05U(2000 – P – D) + 0.95U(2000)

> 0.1(U(2000 – P – D) + F) + 0.90(U(2000) + F)

0.05U(2000 – P – D) + 0.95U(2000 – P) > 0.1(U(0) + F)

+ 0.90(U(2000) + F)

0.05U(2000 – P – D) + 0.95U(2000 – P) > 0.05U(0)

+ 0.95U(2000)

Please show brief explanations and step-by-step

calculation thoughts. Thanks.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The value of a successful project is $420,000; the probabilities of success are 1/2 with good supervision and 1/4 without. The manager is risk neutral, not risk averse as in the text, so his expected utility equals his expected income minus his disutility of effort. He can get other jobs paying $90,000, and his disutility for exerting the extra effort for good supervision on your project is $100,000. (a) Show that inducing high effort would require the firm to offer a compensation scheme with a negative base salary; that is, if the project fails, the manager pays the firm an amount stipulated in the scheme. (b) How might a negative base salary be implemented in reality? (c) Show that if a negative base salary is not feasible, then the firm does better to settle for the low-pay, low-effort situation.arrow_forwardNatalie entered a raffle recently and never checked her tickets. She has recently learned the exact number of the other unchecked tickets. Based on this information she knows that there is a 30% chance that she has won the raffle prize of $1,600. If she does not win the raffle her wealth will be zero. Natalie has a von Neumann- Morgenstern utility such that she wants to maximize the expected value of cvc, where cc is total wealth. What is the minimum price for which Natalie would sell her raffle tickets? $arrow_forwardSuppose you have an exponential utility function given by U(x) =1- exp(-x/R) where, for you, R = 1000. Further, suppose you have an investment with a 50/50 chance of returning either 0 or 2000 dollars. Note U(0) = 0 and U(2000) = 0.865, so the utility of the lottery is 0.432. What is the certain equivalent of that investment?arrow_forward

- Clancy has difficulty finding parking in his neighborhood and, thus, is considering the gamble of illegally parking on the sidewalk because of the opportunity cost of the time he spends searching for parking. On any given day, Clancy knows he may or may not get a ticket, but he also expects that if he were to do it every day, the average amount he would pay for parking tickets should converge to the expected value. If the expected value is positive, then in the long run, it will be optimal for him to park on the sidewalk and occasionally pay the tickets in exchange for the benefits of not searching for parking. Suppose that Clancy knows that the fine for parking this way is $100, and his opportunity cost (OC) of searching for parking is $20 per day. That is, if he parks on the sidewalk and does not get a ticket, he gets a positive payoff worth $20; if he does get a ticket, he ends up with a payoff ofarrow_forwardA pirate is about to set sail on a 2-period journey (trip). He has 100 bags of barley (food). He must decide how much to consume in period 1 and how much to consume in period 2: (C1, c2). He gets all the barley in period 1 and none in period 2. Unfortunately, rats will eat 50% of any barley that he saves to consume in period 2. If the pirate's utility function is U(C1, C2) = C1C2, what levels of consumption does he choose in each period? (Hint: The "price" of barley in each period can be assumed to be 1.)arrow_forwardDavid is an expected-utility maximizer that likes to drive fast (and reckless at times), so his probability of an accident is 2/3. David's preferences over wealth are u(w) = vw. Suppose that David's initial wealth is $100. If David has an accident, he incurs a $51 loss. How much is the risk premium David willing to pay to be as well off in case of accident or not?arrow_forward

- Clancy has difficulty finding parking in his neighborhood and, thus, is considering the gamble of illegally parking on the sidewalk because of the opportunity cost of the time he spends searching for parking. On any given day, Clancy knows he may or may not get a ticket, but he also expects that if he were to do it every day, the average amount he would pay for parking tickets should converge to the expected value. If the expected value is positive, then in the long run, it will be optimal for him to park on the sidewalk and occasionally pay the tickets in exchange for the benefits of not searching for parking. Suppose that Clancy knows that the fine for parking this way is $100, and his opportunity cost (OC) of searching for parking is $20 per day. That is, if he parks on the sidewalk and does not get a ticket, he gets a positive payoff worth $20; if he does get a ticket, he ends up with a payoff ofarrow_forwardAn investor has preferences represented by a utility function u(c) and initial wealth w > 0. Consider an asset that pays G with probability \pi and B with probability 1-\pi. 1.1 Suppose the investor owns this asset. What is the minimum price he would sell it for? (It is sufficient to formulate the condition that this price must satisfy). 1.2 Suppose he does not own it. What is the maximum price he would be willing to pay to buy it? (It is sufficient to formulate the condition that this price must satisfy). 1.3 Explain why (or under which conditions) the buy and sell prices you have found are or are not the same. 1.4 Suppose w = 10, G = 10, B = 5 and u(c) = √c. Compute the buy and sell prices.arrow_forwardPriyanka has an income of £90,000 and is a von Neumann-Morgenstern expected utility maximiser with von Neumann-Morgenstern utility index . There is a 1 % probability that there is flooding damage at her house. The repair of the damage would cost £80,000 which would reduce the income to £10,000. a) Would Priyanka be willing to spend £500 to purchase an insurance policy that would fully insure her against this loss? Explain. b) What would be the highest price (premium) that she would be willing to pay for an insurance policy that fully insures her against the flooding damage?arrow_forward

- Max Pentridge is thinking of starting a pinball palace near a large Melbourne university. His utility is given by u(W) = 1 - (5,000/W), where W is his wealth. Max's total wealth is $15,000. With probability p = 0.9 the palace will succeed and Max's wealth will grow from $15,000 to $x. With probability 1 - p the palace will be a failure and he’ll lose $10,000, so that his wealth will be just $5,000. What is the smallest value of x that would be sufficient to make Max want to invest in the pinball palace rather than have a wealth of $15,000 with certainty? (Please round your final answer to the whole dollar, if necessary)arrow_forwardLucy, the manager of the medical test firm Dubrow Labs, worries about the firm being sued for botched results from blood tests. If it isn't sued, the firm expects to earn profit of $120, but if it is successfully sued, its profit will be only $20. Lucy believes that the probability of a successful suit is 20%. If fair insurance is available and Lucy is risk averse, how much insurance will she buy? Lucy will buy insurance that costs her $ when not successfully sued. (Enter your response as a whole number.)arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education