ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:Б

ces

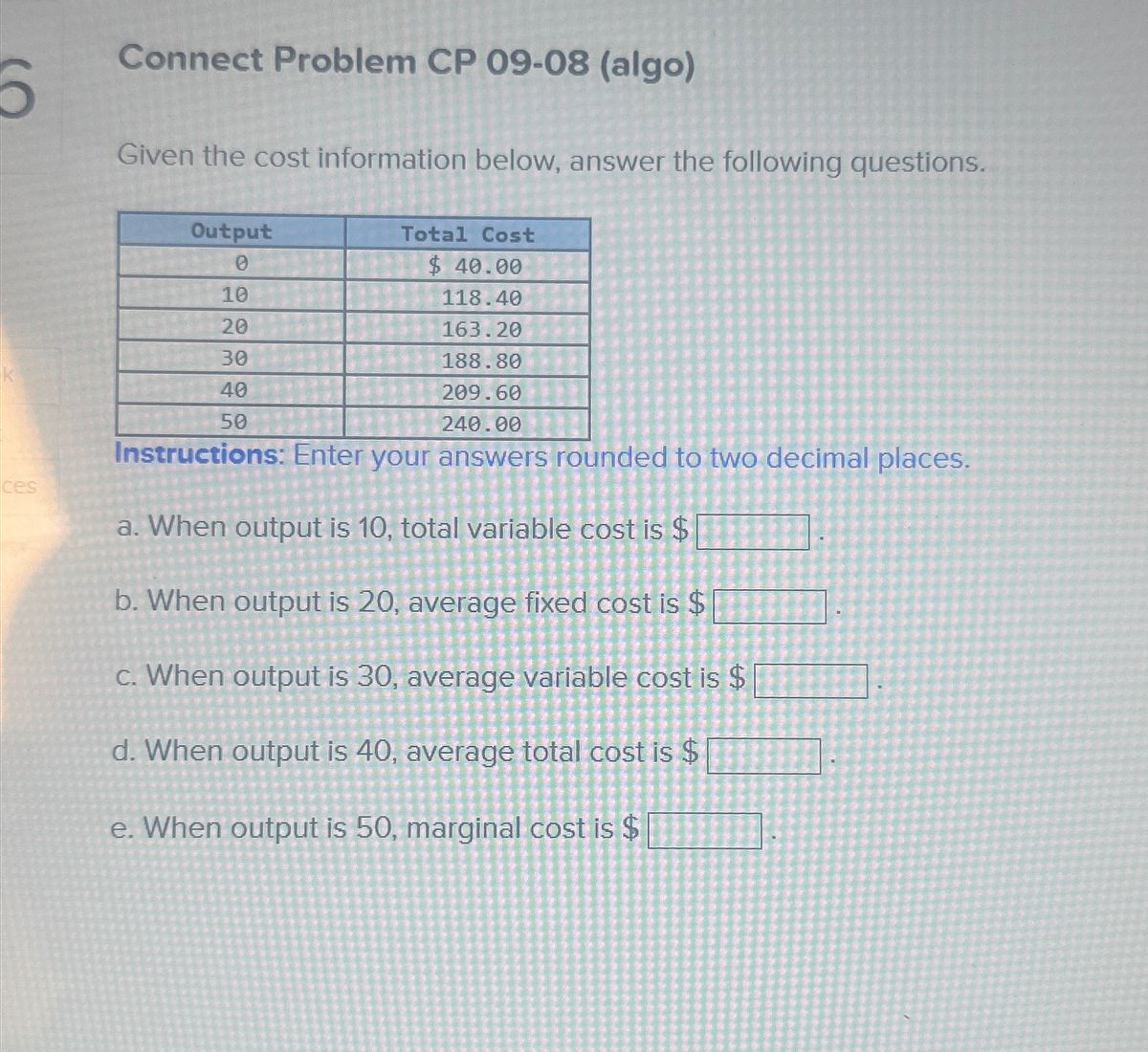

Connect Problem CP 09-08 (algo)

Given the cost information below, answer the following questions.

Output

0

10

20

30

40

50

Total Cost

$ 40.00

118.40

163.20

188.80

209.60

240.00

Instructions: Enter your answers rounded to two decimal places.

a. When output is 10, total variable cost is $

b. When output is 20, average fixed cost is $

c. When output is 30, average variable cost is $

d. When output is 40, average total cost is $

e. When output is 50, marginal cost is $

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Calculate marginal cost if change in total cost is $630 and the change in output is $17arrow_forwardMacmillan Learning a. In the accompanying diagram, place the points labeled Minimum AVC and Minimum ATC in their correct places. Marginal cost, average cost ($ per unit) True False Minimum AVC Minimum ATC F MC Quantity b. Average variable cost reaches its minimum point at a lower level of output than average total cost.arrow_forwardAt the minimum-cost output A. average variable cost must equal marginal cost. B. average fixed cost must equal marginal cost. C. average total cost must equal marginal cost. D. Answers (a), (b), and (c) are all true.arrow_forward

- Assume workers in labour market M are qualified to work in an alternative competitive labour market N, and vice versa. What will happen to the wage rate and level of employment in market M if there is an increase in the demand for labour in market N?arrow_forwardThe marginal cost curve intersects the short-run average total cost curve where: A. average variable costs are maximized in the short run. B. average variable costs are minimized in the short run. C. average total costs are minimized in the short run. D. marginal cost is minimized in the short run.arrow_forwardAs long as marginal cost is below average cost, average cost will be a. falling b. rising. c. constant. d. changing in a direction that cannot be determined without more information.arrow_forward

- Which of the following statement is correct? a. Marginal cost will equal average total cost when marginal cost is at its lowest point. b. When marginal cost is less than average total cost, average total cost will rise. C. When marginal cost is greater than average total cost, average total cost will fall. d. Marginal cost will equal average total cost when average total cost is at its lowest point.arrow_forwardThe government imposes a $1,000 one-time license fee on all pizza restaurants. As a result, which of the following cost curves shift, and why or why not?a. Average total cost.b. Marginal Cost.c. Average Variable Cost.arrow_forwardSolve for the missing entries in the above table. Enter whole dollar values for Total and Marginal Cost calculations. Round all average cost calculations to the nearest cent. Enter your answers in the following format: A. $5 B. $18 C. $40 etc. (Note, this is just an example, these are NOT the correct answers.)arrow_forward

- If the marginal cost of production is greater than the average cost, in what direction must the average cost be changing if any? A. The average cost must be rising. B. The average cost would equal 0. C. The average cost must be falling. D. The average cost is unaffected. E. The average cost would become non-existent.arrow_forwardQuestion 19 of 20 > (TC is total cost; VC is variable cost; Q is quantity.) ΔΤC . а. b. The amount by which total cost increases when an AQ additional unit is produced: Marginal cost Average (total) cost Average variable cost TC d. The total cost divided by the quantity of output: с. e. The change in total cost divided by the change VC f. in output: g. The sum of all costs that change as output changes divided by the number of units produced:arrow_forwardGiven the cost information below, answer the following questions. Output Total Cost $10.00 10 88.40 20 133.20 30 158.80 40 179.60 50 210.00 Instructions: Enter your answers rounded to two decimal places. a. When output is 10, total variable cost is $ b. When output is 20, average fixed cost is $ c. When output is 30, average variable cost is $ d. When output is 40, average total cost is $ e. When output is 50, marginal cost is $arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education