ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

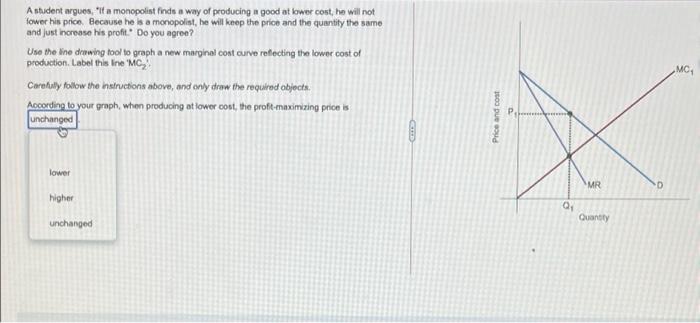

Transcribed Image Text:A student argues, "it a monopolist finds a way of producing a good at lower cost, he will not

lower his price. Because he is a monopolist, he will keep the price and the quantity the same

and just increase his profit." Do you agree?

Use the line drawing tool to graph a new marginal cost ourve reflecting the lower cost of

production. Label this Ine MC,

MC,

Carefully follow the instructions above, and only draw the required objects.

According to your graph, when producing at lower cost, the proft-maximizing price is

unchanged

lower

MR

higher

Quantity

unchanged

Price and cost

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardCompare the efficiency of monopoly and perfect competition. Which is more efficient? Explain your reasoning and illustrate with a hypothetical example.arrow_forwardExplain how economies of scale can be a barrier to entry.arrow_forward

- Draw an example of a monopoly with a linear demand curve and a constant marginal cost curve. a. Show the profit-maximizing price and output and and identify the areas of consumer surplus, producer surplus, and deadweight loss. Also show the quantity that would be produced if the monopoly were to act like a price taker. b. Now suppose that the demand curve is a smooth concave-to-the-origin curve (whose ends hit the axes) that is tangent to the original demand curve at the point Explain why the monopoly equilibrium will be the same as with the linear demand curve. Show how much output the firm would produce if it acted like a price taker. Show how the welfare areas change. c. Repeat the exercises in part b if the demand curve is a smooth convex-to-the-origin curve (whose ends hit the axes) that is tangent to the original demand curve at the pointarrow_forwardSuppose 2 gas stations must post their prices for regular gasoline at 6am each morning and cannot change their price during the day. Each gas station has a choice: charge a relatively “low” price or charge a relatively “high” price. The following shows their profit for the day of each gas station depending upon which price each gas station chooses: Gas Station B Low Price High Price Gas Station A Low Price $2000, $900 $500, $1500 High Price $1200, $1800 $300, $2100 Assume that this is a "one shot" game: 4. Does this game represent a prisoner’s dilemma situation? Why or why not? 5. If the gas stations can talk the night before making their pricing decision and discuss their pricing strategies, what pricing strategy would each gas station choose the next morning? Assuming both gas stations act rationally, what will be the outcome of the game? Explain.arrow_forwardThe figure shows what type of market? >>Please add an explanation of how natural monopoly differs in graph vs. normal monopoly.arrow_forward

- In the attached graph is a depiction of a monopoly. At what output should he or she produce? What price should they charge for the product? Is the firm making profits or losses?arrow_forwardSuppose that there are 7 potential purchasers of a Krustyburger. Each individual will buy at most one burger and Krustyburger has a monopoly. The table below lists their maximum willingness to pay and their ages. The cost of production for each Krustybarger is zero Name, age Maximum Willingness to Pay $4 Marge, 34 Homer, 38 $10 $3 Lisa, 7 Maggie, 2 Ned, 46 Quimby, 50 Bart, 9 $1 $3 $7 $3 Suppose that instead, they have two prices: one price for adults (over the age of 12) and one for children. What price will they set for each? a. The price for adults will be 57 and the price for children will be $3 Ob. The price for adults will be $3 and the price for children will be $1 O The price for adults will be $4 and the price for children will be $3 Od. The price for adults will be $10 and the price for children will be $3arrow_forwardSuppose 2 gas stations must post their prices for regular gasoline at 6am each morning and cannot change their price during the day. Each gas station has a choice: charge a relatively “low” price or charge a relatively “high” price. The following shows their profit for the day of each gas station depending upon which price each gas station chooses: Gas Station B Low Price High Price Gas Station A Low Price $2000, $900 $500, $1500 High Price $1200, $1800 $300, $2100 Assume that this is a "one shot" game: Which strategy should Gas Station A choose? Is it a dominant strategy? Explain why or why not. Which strategy should Gas Station B choose? Is it a dominant strategy? Explain why or why not What is the outcome for each Gas Station? How much profits will each Gas Station earn? Explain. Does this game represent a prisoner’s dilemma situation? Why or why not? If the gas stations can talk the night before making their pricing decision and discuss their pricing…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education