FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

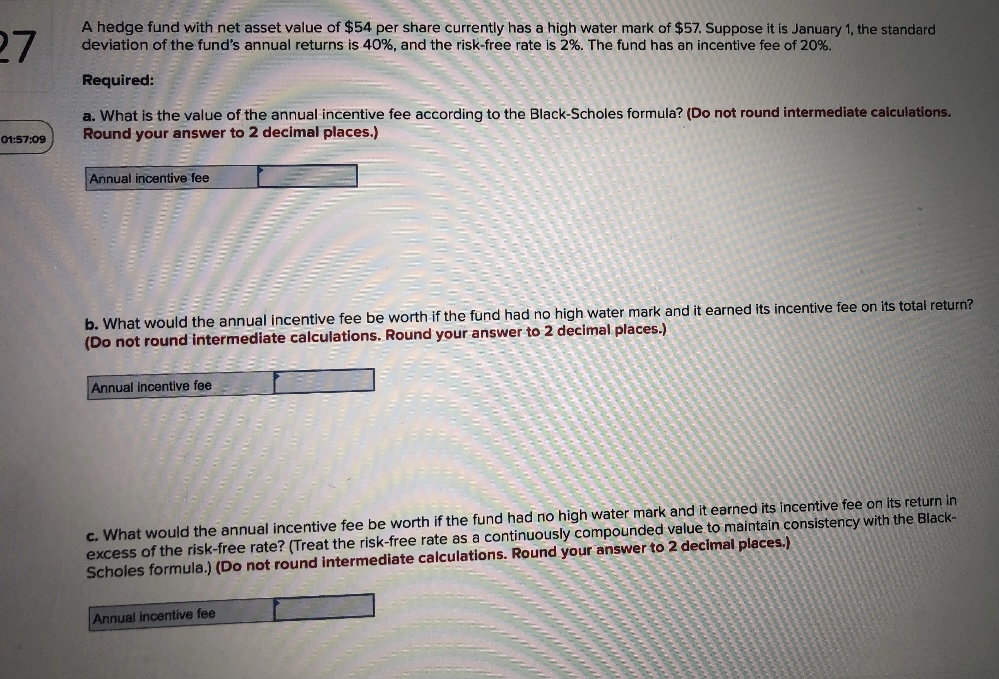

Transcribed Image Text:27

A hedge fund with net asset value of $54 per share currently has a high water mark of $57. Suppose it is January 1, the standard

deviation of the fund's annual returns is 40%, and the risk-free rate is 2%. The fund has an incentive fee of 20%.

Required:

a. What is the value of the annual incentive fee according to the Black-Scholes formula? (Do not round intermediate calculations.

Round your answer to 2 decimal places.)

01:57:09

Annual incentive fee

b. What would the annual incentive fee be worth if the fund had no high water mark and it earned its incentive fee on its total return?

(Do not round intermediate calculations. Round your answer to 2 decimal places.)

Annual incentive fee

c. What would the annual incentive fee be worth if the fund had no high water mark and it earned its incentive fee on its return in

excess of the risk-free rate? (Treat the risk-free rate as a continuously compounded value to maintain consistency with the Black-

Scholes formula.) (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Annual incentive fee

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- 2. Suppose you are the money manager of a $4.96 million investment fund. The fund consists of four stocks with the following investments and betas: Stock Investment Beta A $ 580,000 1.50 B 800,000 (0.50) C 980,000 1.25 D 2,600,000 0.75 If the market's required rate of return is 11% and the risk-free rate is 5%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places.arrow_forwardA pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term bond fund, and the third is a money market fund that provides a safe return of 4%. The characteristics of the risky funds are as follows: Expected Return Standard Deviation Stock fund (S) 19 % 34 % Bond fund (B) 10 18 The correlation between the fund returns is 0.11. What is the Sharpe ratio of the best feasible CAL?arrow_forwardThank youarrow_forward

- Please step by step answer.arrow_forwardSuppose you are the money manager of a $5.08 million investment fund. The fund consists of four stocks with the following investments and betas: Stock Investment Beta $ 440,000 A B C D 0.75 If the market's required rate of return is 10% and the risk-free rate is 6%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places. 500,000 1,140,000 3,000,000 1.50 (0.50 ) 1.25arrow_forwardA pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term bond fund, and the third is a money market fund that provides a safe return of 7%. The characteristics of the risky funds are as follows: Expected Return Standard Deviation Stock fund (S) 23% 28% Bond fund (B) 15 17 The correlation between the fund returns is 0.12. Solve numerically for the proportions of each asset and for the expected return and standard deviation of the optimal risky portfolio. (Do not round intermediate calculations. Write your answers as decimals rounded to 4 places.)arrow_forward

- Suppose you are the money manager of a $4.88 million investment fund. The fund consists of four stocks with the following investments and betas: Stock Investment A $ 260,000 B 640,000 с 1,180,000 D 2,800,000 0.75 If the market's required rate of return is 10% and the risk-free rate is 3%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places. % Beta 1.50 (0.50) 1.25arrow_forwardPlease do not provide answer in image formate thank you.arrow_forwardA pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term bond fund, and the third is a money market fund that provides a safe return of 4%. The characteristics of the risky funds are as follows: Expected Return Stock fund (S) Bond fund (B) The correlation between the fund returns is 0.10. Sharpe ratio Standard Deviation 37% 23 22% 14 What is the Sharpe ratio of the best feasible CAL? Note: Do not round intermediate calculations. Enter your answer as a decimal rounded to 4 places.arrow_forward

- You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Year 2018 Fund -18.80% Market -36.50% Risk-Free 1% 2019 25.10 20.70 6 2020 13.60 13.00 2 2021 2022 7.00 -1.92 8.40 -4.20 6 2 Calculate Jensen's alpha for the fund, as well as its information ratio. Note: Do not round intermediate calculations. Enter the alpha as a percent rounded to 2 decimal places. Round the ratio to 4 decimal places. Jensen's alpha Information ratio Answer is not complete. 3.69 %arrow_forwardYou have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.93. Year 2018 2019 2020 2021 2022 Fund -23.60% 25.10 14.40 7.00 -2.40 Market -44.50% 21.50 15.40 Jensen's alpha Information ratio 9.20 -6.20 Risk-Free 18 3 Calculate Jensen's alpha for the fund, as well as its information ratio. Note: Do not round intermediate calculations. Enter the alpha as a percent rounded to 2 decimal places. Round the ratio to 4 decimal places. 2 6 %arrow_forwardA pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term bond fund, and the third is a money market fund that provides a safe return of 8%. The characteristics of the risky funds are as follows: Standard Deviation Stock fund (S) Bond fund (B) 30% 15 The correlation between the fund returns is 0.10. You require that your portfolio yield an expected return of 14%, and that it be efficient, that is, on the steepest feasible CAL. Required: a. What is the standard deviation of your portfolio? b. What is the proportion invested in the money market fund and each of the two risky funds? Expected Return 20% 12 Complete this question by entering your answers in the tabs below. Required A Money market fund Stocks Bonds Required B What is the proportion invested in the money market fund and each of the two risky funds? Note: Round your answers to 2 decimal places. Proportion Invested % %arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education