Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

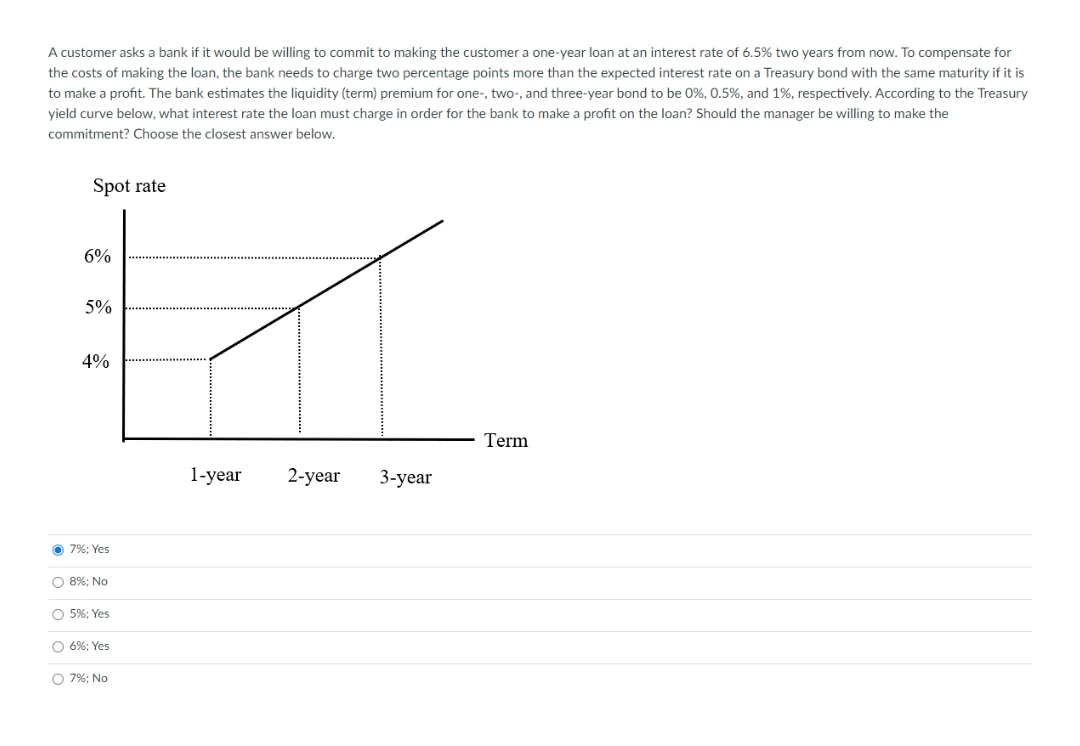

Transcribed Image Text:A customer asks a bank if it would be willing to commit to making the customer a one-year loan at an interest rate of 6.5% two years from now. To compensate for

the costs of making the loan, the bank needs to charge two percentage points more than the expected interest rate on a Treasury bond with the same maturity if it is

to make a profit. The bank estimates the liquidity (term) premium for one-, two-, and three-year bond to be 0%, 0.5%, and 1%, respectively. According to the Treasury

yield curve below, what interest rate the loan must charge in order for the bank to make a profit on the loan? Should the manager be willing to make the

commitment? Choose the closest answer below.

Spot rate

6%

5%

4%

Term

1-year

2-year

3-year

O 7%; Yes

O 8%; No

O 5%: Yes

O 6%; Yes

O 7%; No

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- A firm has obtained a 3-year floating rate loan paying a premium of 2%. Given the prime rate is 5%. Immediately after the loan is taken, the prime rate increases to 6%. Which of the following is TRUE? Question 49 options: 1) The interest rate payable is 3%. 2) The interest rate payable is 5%. 3) The interest rate payable is 7%. 4) The interest rate payable is 8%.arrow_forwardFor the next three questions (1-3) assume what follows: Assume that you acquired a previously issued debt instrument. According to its specifications, it promised to pay $1,000 precisely in two years from the day of its original issue. At the time it was issued, investors anticipated 8.00% in interest on instruments with similar characteristics and risk level. *Note, standard rounding rules apply to all calculations! Q1. What price did you have to pay for this security - under assumption that you acquired it in a secondary market precisely three months after its original issuing, and taking into account that at the time of your acquisition investors anticipated to earn 10.00% in interest on securities with similar features and risk characteristics? A). $857.34 B). $846.37 3000K ASarrow_forwardWhat would the effect of the failure in the ratio measurement?arrow_forward

- A bank has issued a six-month, $1.0 million negotiable CD with a 0.53 percent quoted annual interest rate (iCD, sp). a. Calculate the bond equivalent yield and the EAR on the CD. b. How much will the negotiable CD holder receive at maturity? c. Immediately after the CD is issued, the secondary market price on the $1 million CD falls to $998,900. Calculate the new secondary market quoted yield, the bond equivalent yield, and the EAR on the $1.0 million face value CD. Required A: Bond Equivalent Yield ___ EAR____ (Use 365 days in a year. Do not round intermediate calculations. Round your answers to 3 decimal places.) Required B: CD Holder will receive at maturity_____(Do not round intermediate calculations. Round your answer to nearest whole number.) Required C: Bond Equivalent Yield____ Secondary Market Quoted Yield______ EAR_____ (Use 365 days in a year. Do not round intermediate calculations. Round your answers to 4 decimal places.arrow_forwardA bank has assets of $500,000,000 and equity of $40,000,000. The assets have an average duration of 5.5 years, and the liabilities have an average duration of 2.5 years. An 8-year fixed-rate T-bond with the same coupon as the fixed-rate on the swap has a duration of 6 years, and the duration of a floating-rate bond that reprices annually is one year. The bank wishes to hedge its balance sheet with swap contracts that have notional contracts of $100,000. What is the optimal number of swap contracts into which the bank should enter? 2,500 contracts. 2,760 contracts. 13,800 contracts. 3,200 contracts. None of the above.arrow_forwardIf the owners choose to invest in bonds instead, they look at a $136,125.00 bond set to mature in 9 years with a bond rate of 2.00%, payable semi-annually. The market rate is 5.40%, compounded semi-annually. The owners will only purchase the bond if they can afford it with their savings ($123,750.00), and they can get the bond at a discount because they think the market rate will go down, potentially making the bond more valuable in the future. 2. Calculate the purchase price of the bond if it is purchased today (9 years before maturity). 3. Do the owners have enough money to buy their bond? Will they make the purchase?arrow_forward

- Select all that are true with respect to historical data on risk and return in the U.S. financial markets since about 1926, Group of answer choices A portfolio of small stocks has earned higher returns than large stocks, with less risk A portfolio of small stocks has earned higher returns that large stocks, with higher risk Stocks have outperformed government bonds, albeit with higher risk With respect to a diversified stock portfolio, the longer the holding period, the higher the risk. With respect to a diversified stock portfolio, the longer the holding period, the lower the risk.arrow_forwardA bank is considering a debt-for-equity swap to slavage a $5 million loan that is in default. They expect to recover $2.7 million after liquidation ane legal fees. A turnaround expert has recommended the following cassh flow analysis if the bank chooses the debt-for-equirt swap. Initial Investment $5,000,000 in year 0 Expected cash flows after turnaround $1,750,000 in years 2-6 Sale of Equity (Exit) $3,500,000 in year 6 Equity ownership 70% Cost of capital 12% Should they engage in the debt-for-equity swap? A Yes, they should engage in the debt-for-equity swap B No, they should not because the NPV after the turnaround is greater than the liquidation value C Yes, they should engage in the debt-for-equity swap only if the cost of capital is 10% D No, they should not engage in the…arrow_forwardDesert Trading Company has issued $100 million worth of long-term bonds at a fixed rate of 10%. The firm then enters into an interest rate swap where it pays SOFR and receives a fixed 5% on notional principal of $100 million. What is the firm's effective interest rate on its borrowing? Only typing answer Please answer explaining in detail step by step without table and graph thankyouarrow_forward

- Desert Trading Company has issued $100 million worth of long-term bonds at a fixed rate of 10%. The firm then enters into an interest rate swap where it pays SOFR and receives a fixed 5.2% on notional principal of $100 million. What is the firm's effective interest rate on its borrowing? Note: Enter value as positive amount. Round your answer to 1 decimal place. Effective interest rate %arrow_forwardWhich of the following are characteristics of Treasury bills (T- bills)? Check all that apply. There is a secondary market for T - bills. Institutional investors can purchase T - bills. Individuals can purchase T- bills. T - bills have maturities of 28, 91, and 182 days. Suppose Mr. Smith buys a 30-day T - bill with a face value of $1,000 at a price of $ 996. The discount rate yield (DRY) would be, whereas the investment return yield (IRY) would be.arrow_forwardSuppose a bank enters a repurchase agreement in which it agrees to buy Treasury securities from a correspondent bank at a price of $31,950,000, with the promise to buy them back at a price of $32,000,000. a. Calculate the yield on the repo if it has a 5-day maturity. b. Calculate the yield on the repo if it has a 15-day maturity. (For all requirements, use 360 days in a year. Do not round intermediate calculations. Round your percentage answers to 5 decimal places. (e.g., 32.16161)) a. b. X Answer is complete but not entirely correct. Yield on the repo Yield on the repo 1.02857 % 0.34286 %arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education