Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

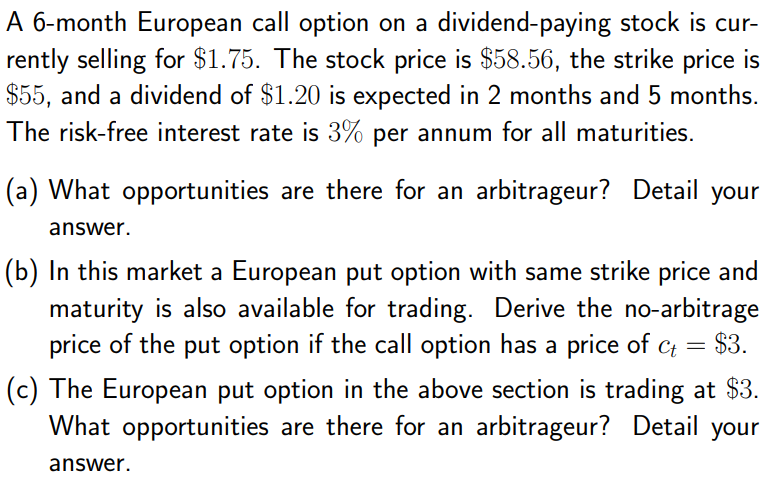

Transcribed Image Text:A 6-month European call option on a dividend-paying stock is cur-

rently selling for $1.75. The stock price is $58.56, the strike price is

$55, and a dividend of $1.20 is expected in 2 months and 5 months.

The risk-free interest rate is 3% per annum for all maturities.

(a) What opportunities are there for an arbitrageur? Detail your

answer.

(b) In this market a European put option with same strike price and

maturity is also available for trading. Derive the no-arbitrage

$3.

price of the put option if the call option has a price of c =

%3D

(c) The European put option in the above section is trading at $3.

What opportunities are there for an arbitrageur? Detail your

answer.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The following 1-year European call options are available on the stock of Vega International, whose stock is trading at €72.50: Strike Price Call Price (€) (€) 60 8.00 75 3.00 90 2.00 What is the maximum profit realised at maturity from a long butterfly spread created from these call options? Assume a risk-free rate of 5%.arrow_forwardThe price of a European call option on a stock with a strike price of $50.9 is $5.6. The stock price is $40.1, the continuously compounded risk-free rate (all maturities) is 5.2% and the time to maturity is one year. A dividend of $0.6 is expected in six months. What is the price of a one-year European put option on the stock with a strike price equal to the call's strike price? Please state the formula and steps, thanksarrow_forwardWhat is the value of d, of a European call option on a non-dividend-paying stock when the stock price is $60, the strike price is $59, the risk-free interest rate is 5% per annum the volatility (Standard Deviation) is 30% per annum, and the time to maturity is three months? c=SN(d,)-Ke-N(₂) where and O√T OA02704 OB0.2167 *√T OC.0.3561 OD.0.1204arrow_forward

- Melbourne Capital Ltd considers selling European call options on ANZ Bank Ltd for $1.50 per option. The current market price is $17.70 on 28th September 2020, the exercise price is $20, and the maturity of each call option is 6 months. (i) Under what circumstances does the investor make a profit? (ii) Under what circumstances will the option be exercised? (iii) How many call options should the investor sell to raise a total capital of $1,260,000?arrow_forwardConsider a two-period binomial model in which a non-dividend-paying stock currently trades at £35. Over each of the next two six-month periods, the share price is expected to go up by 12% or down by 9%. The risk-free interest rate is 6% per annum with continuous compounding. Calculate the value of a one-year European put option with a strike price of £36, using a two-period binomial tree method.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education