Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:l Turk Telekom

11:27

ni %40

bartleby.com

שיגסרב

/ Finance / Q&A Library / Finance Question

e Question

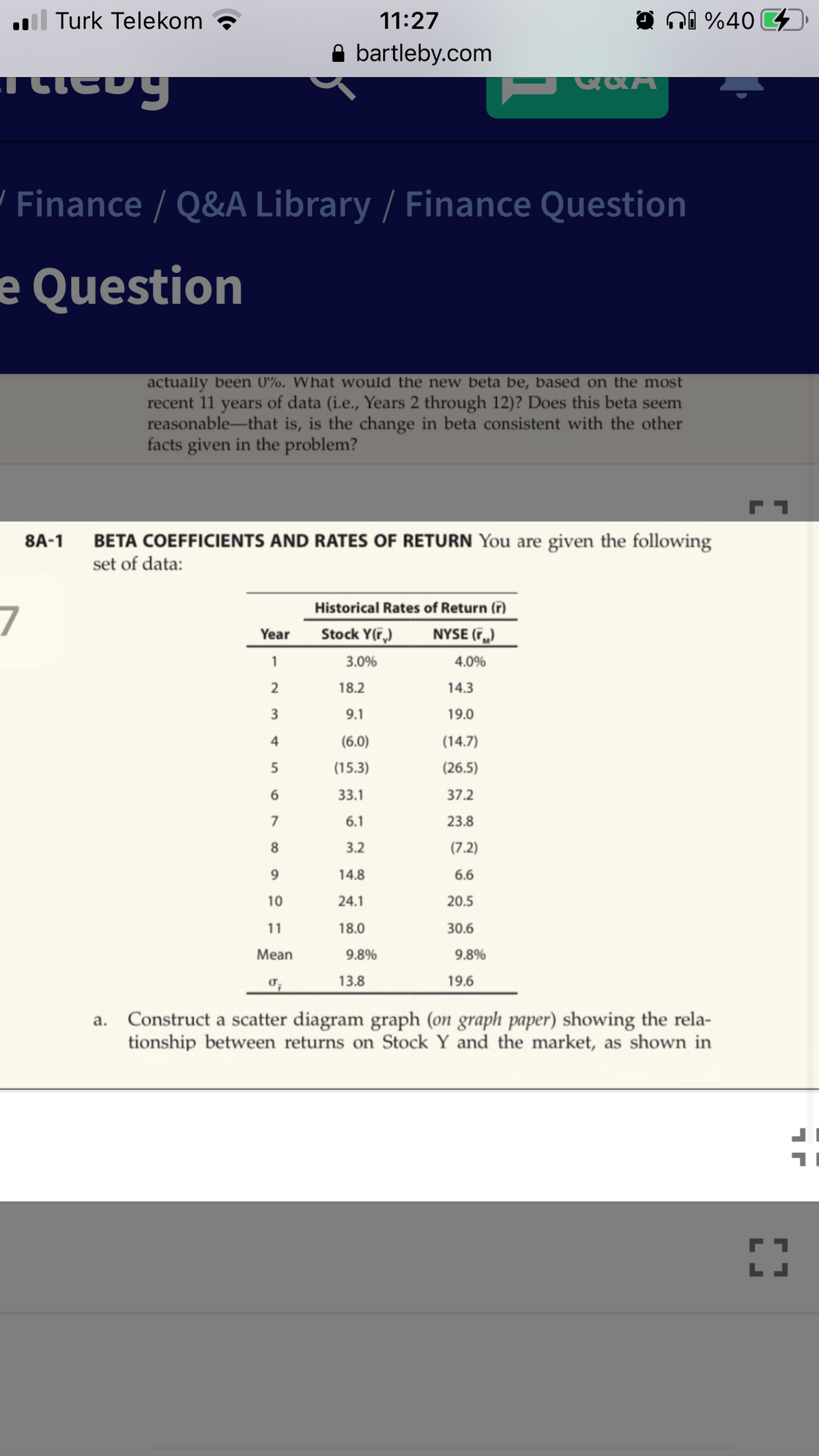

actually been 0%. What would the new beta be, based on the most

recent 11 years of data (i.e., Years 2 through 12)? Does this beta seem

reasonable-that is, is the change in beta consistent with the other

facts given in the problem?

BETA COEFFICIENTS AND RATES OF RETURN You are given the following

set of data:

8A-1

7

Historical Rates of Return (r)

Stock Y(F,)

NYSE (r.)

Year

1

3.0%

4.0%

18.2

14.3

3

9.1

19.0

4

(6.0)

(14.7)

(15.3)

(26.5)

33.1

37.2

7

6.1

23.8

8.

3.2

(7.2)

14.8

6.6

10

24.1

20.5

11

18.0

30.6

Mean

9.8%

9.8%

13.8

19.6

a. Construct a scatter diagram graph (on graph paper) showing the rela-

tionship between returns on Stock Y and the market, as shown in

Transcribed Image Text:l Turk Telekom

11:27

ni %40 4

A bartleby.com

ance / Q&A Library / Finance Question

uestion

Figure 8A.1; then draw a freehand approximation of the regression

line. What is the approximate value of the beta coefficient? (If you have

a calculator with statistical functions, use it to calculate beta.)

b. Give a verbal interpretation of what the regression line and the beta

coefficient show about Stock Y's volatility and relative riskiness as

compared with other stocks.

c. Suppose the scatter of points had been more spread out, but the

regression line was exactly where your present graph shows it. How

would this affect (1) the firm's risk if the stock were held in a one-

asset portfolio and (2) the actual risk premium on the stock if the

CAPM held exactly? How would the degree of scatter (or the correla-

tion coefficient) affect your confidence that the calculated beta will

hold true in the years ahead?

d. Suppose the regression line had been downward sloping and the beta

coefficient had been negative. What would this imply about (1) Stock

Y's relative riskiness and (2) its probable risk premium?

Construct an illustrative probability distribution graph of returns (see

Figure 8.3) for portfolios consisting of (1) only Stock Y, (2) 1% each

of 100 stocks with beta coefficients similar to that of Stock Y, and (3)

all stocks (i.e., the distribution of returns on the market). Use as the

expected rate of return the arithmetic mean as given previously for

both Stock Y and the market, and assume that the distributions are

normal. Are the expected returns "reasonable"; that is, is it reasonable

that f, = fM = 9.8%?

е.

f. Now, suppose that in the next year, Year 12, the market return was

27%, but Firm Y increased its use of debt, which raised its perceived

risk to investors. Do you think that the return on Stock Y in Year 12

could be approximated by this historical characteristic line?

î, = 3.8% + 0.62(r,) = 3.8% + 0.62(27%) = 20.5%

g. Now, suppose r, in Year 12, after the debt ratio was increased, had

actually been 0%. What would the new beta be, based on the most

recent 11 years of data (i.e., Years 2 through 12)? Does this beta seem

reasonable-that is, is the change in beta consistent with the other

facts given in the problem?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- 4 Skipped Use the following data for Questions 3-5: Value 12500 17500 20000 Stock A B C Exp. Return 8.5% 9.2% 10.6% Beta 0.8 1.2 1.4 Question 4: What is the portfolio's Beta? ENTER YOUR ANSWER ROUNDED TO 2 DECIMAL PLACESarrow_forwardStock i’s standard deviation35.00%Market’s standard deviation32.00%Correlation between Stock i and the market0.65Beta coefficient of Stock i:arrow_forwardForecasted returns for Stock A: State of the Economy Prob. of State Return in State Prosperity 35% 5% Normal 45% 14% Recession 20% -3% What is the standard deviation of the stock’s returns?arrow_forward

- Consider the following information on two stocks: P(State) Stock A Stock B Boom 20% 30% 20% Normal 50% 12% -5% Slow 15% 4% 8% Recession 15% -10% 10% Calculate the correlation (A,B). (Enter percentages as decimals and round to 4 decimals)arrow_forwardQ2 - Returns on stocks X and Y are listed below: Period 1 2 3 4 5 6 7Stock X 4% -2% 5% -1% 10% 7% 12%Stock Y -3% 7% 4% 2% 2% 8% -3% Consider a portfolio of 10% stock X and 90% stock Y. What is the mean of portfolio returns? Please specify your answer in decimal terms and round your answer to the nearest thousandth (e.g., enter 12.3 percent as 0.123).arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education