Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:ferences

Mailings

Review View

Help RCM

Acrobat

Foxit Reader PDF

Foxit PDF

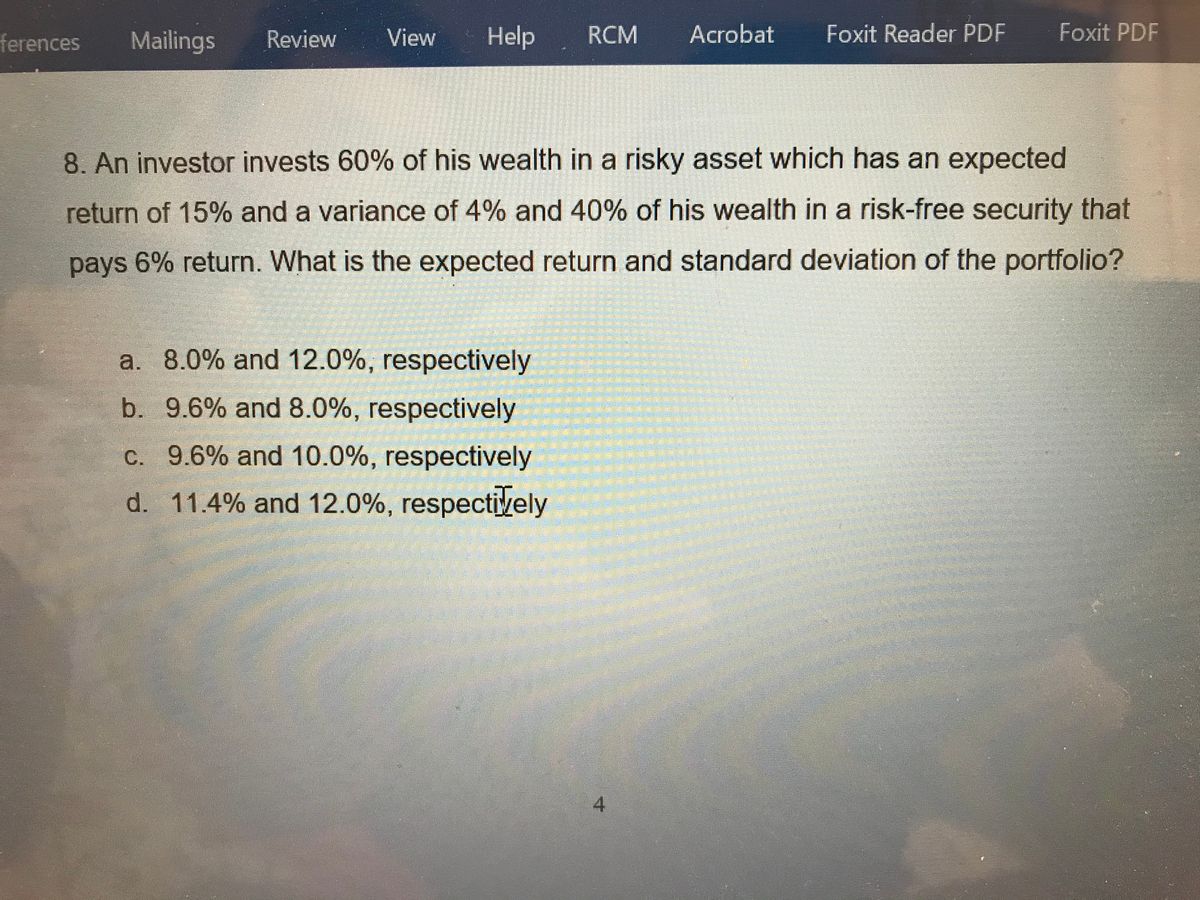

8. An investor invests 60% of his wealth in a risky asset which has an expected

return of 15% and a variance of 4% and 40% of his wealth in a risk-free security that

pays 6% return. What is the expected return and standard deviation of the portfolio?

a. 8.0% and 12.0%, respectively

b. 9.6% and 8.0%, respectively

C. 9.6% and 10.0%, respectively

d. 11.4% and 12.0%, respectively

4.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The beta on risky asset A is 1.8 and the beta on risky asset B is 1.1. The expected return on the market portfolio is 10% and the risk free rate of return is 4%. Consider a portfolio comprising the two risky assets and the risk-free asset where you invest 50% in risky asset A and 30% in risky asset B. What is (i) the beta of a portfolio and (ii) the expected return of the portfolio? a None of the above b (i) 0.97 and (ii) 9.82% c (i) 1.23 and (ii) 9.82% d (i) 1.23 and (ii) 11.38% e (i) 0.97 and (ii) 11.38%arrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Y Z Market Risk-free Rp 16.00% бр 32.00% 15.00 27.00 7.30 17.00 11.30 5.80 22.00 0 Bp 1.90 1.25 0.75 1.00 0 Assume that the tracking error of Portfolio X is 13.40 percent. What is the information ratio for Portfolio X? Note: A negative value should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to 4 decimal places. Information ratioarrow_forwardAn investor invests 30 percent of his wealth in a risky asset with an expected rate of return of 0.14 and a standard deviation of .35 and 70 percent in a T-bill that pays 3 percent. His portfolio's expected return and standard deviation are __________ and __________, respectively. Please show the formulaarrow_forward

- The expected return for asset A is 4.00% with a standard deviation of 9.00%, and the expected return for asset B is 6.75% with a standard deviation of 3.00%. Based on your knowledge of efficient portfolios, fill in the blanks in the following table with the appropriate answers. Proportion of Portfolio in Security A WA 1.00 0.75 0.50 0.25 0.00 Proportion of Portfolio in Security B WB 0.00 0.25 0.50 0.75 1.00 Expected Portfolio Return FP 4.00% 4.69% 6.06% 6.75% Standard Deviation Op Case I (PAB= -0.4) 6.5 4.1 2.5 3.0 Standard Deviation op Case II (PAB= 0.3) 9.0 5.2 3.6 3.0 The minimum risk portfolio allocation to asset A within the portfolio for case III is. Therefore, you are better off Standard Deviation op Case III (PAB=0.8) 9.0 7.4 5.8 ▼ 3.0arrow_forwardAn investor invests 70% of his wealth in a risky asset with an expected rate of return of 0.15 and a variance of 0.04. He also places 30% of his wealth in a T-bill that pays 5%. His portfolio's expected return and standard deviation are __________ and __________, respectively. Group of answer choices 0.120; 0.14 0.087; 0.06 0.295; 0.12 0.087; 0.12 0.895; 0.11arrow_forwardQ6. ) A portfolio is formed by investing 32% in Asset-1; 28% in Asset-2; and 40% in Asset-3. The covariances of the three assets with the market portfolio are 24, 36, and 48. The variance of the market portfolio is 40. If the risk - less rate is 7.5%, and the expected return on the market portfolio is 12.5%, what is the expected return of this portfolio, assuming that the CAPM is valid?arrow_forward

- 1. A stock has a beta of 1.15 and an expected return of 14 percent. A risk-free asset Currently earns 4.2 percent. a . What is expected return on a portfolio that is equally in inverted assets? b. if portfolio of the two assets has beta of 75, what are the portfolio weights? C. if a portfolio of the two assets has an expected return of 8 percent .what is its beta? the twoarrow_forward1. Suppose you have n risky assets you can combine in a portfolio. Each risky asset has an expected return of 8% and a standard deviation of 30%. The risky assets are uncorrelated with each other. (a) Consider an equally weighted portfolio of 2 of these securities. What is its expected return? What will its standard deviation be? (b) Consider an equally weighted portfolio of 30 of these securities. What is its expected return? What will its standard deviation be? (c) Suppose we let the number of these securities increase without bound. That is, n→ ∞o. What happens to the standard deviation of an equally weighted portfolio of these securities as the number of assets in the portfolio becomes extremely large? What will the riskless rate be in this case, and why? -int IDEarrow_forwardConsider a T-bill with a rate of return of 6% and the following risky securities: Security A: E(r) = 9%; Standard Deviation = 9% Security B: E(r) = 10%; Standard Deviation = 11% security C: E(r)= 16%; Standard Deviation = 20% Security D: E(r) = 18%; Standard Deviation = 26% From which set of portfolios, formed with the T-bill and any one of the four risky securities, woulda risk-averse investor always choose his portfolio? Select one: A. The set of portfolios formed with the T-bill and security D. B.The set of portfolios formed with the T-bill and security A. oC. The set of portfolios formed with the T-bill and security B. D. The set of portfolios formed with the T-bill and security c. E. Cannot be determined.arrow_forward

- Asset B has a beta of 1.2 and an expected return of 16%. The risk-free rate is 4%. If you wish to hold a portfolio with a beta equal to 1.0, what is the expected return of the portfolio? 13.0% 10.0 % 15.0 % 12.0% 14.0%arrow_forwardAn investment has probabilities 0.15, 0.34, 0.44, 0.67, 0.2 and 0.15 of giving returns equal to 50%, 39%, -4%, 20%, -25%, and 42%. What are the expected returns and the standard deviations of returns?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education