ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

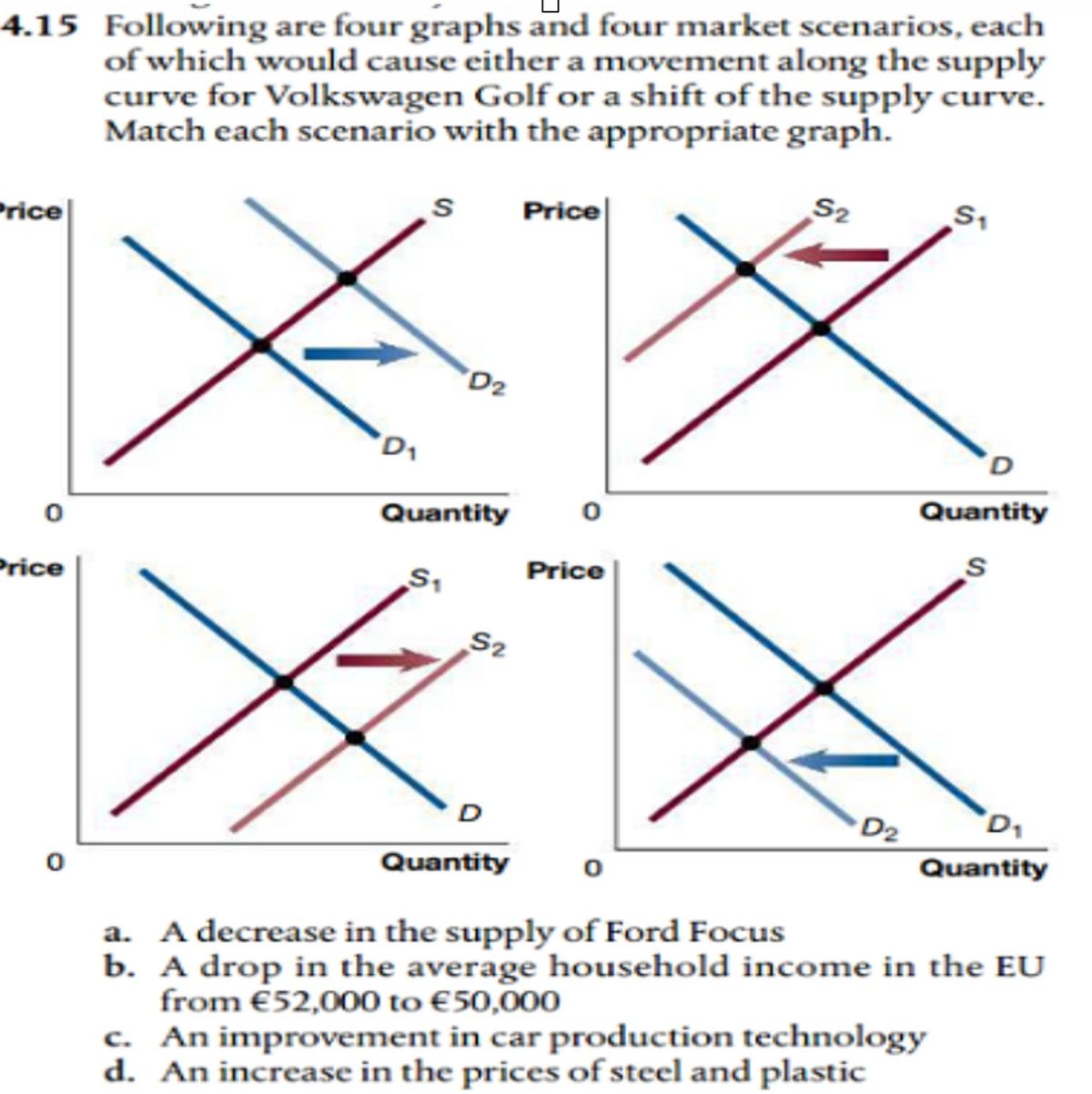

Transcribed Image Text:4.15 Following are four graphs and four market scenarios, each

of which would cause either a movement along the supply

curve for Volkswagen Golf or a shift of the supply curve.

Match each scenario with the appropriate graph.

Price

Price

D₁

S

D₂

Quantity

S₁

S₂

D

Quantity

Price

Price

S2

D2

S₁

D

Quantity

S

D₁

Quantity

a. A decrease in the supply of Ford Focus

b. A drop in the average household income in the EU

from €52,000 to €50,000

c. An improvement in car production technology

d. An increase in the prices of steel and plastic

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- For each of the following changes in the demand or supply curves in the automobile market below, draw a graph showing the old demand and supply curves as well as the new demand or supply curve (whichever shifts). Also, show how the equilibrium price and equilibrium quantity change. Show work on 3 different graphs. The income of consumers rises and automobiles are considered a normal good. Over time, and due to new resource discoveries, gasoline prices fall. The availability and price of public transportation falls.arrow_forwardA cyberattack this week closed the largest fuel pipeline in the U.S., restricting gasoline supplies to the northeast. Use a supply and demand diagram to illustrate the effects on gasoline prices in that region. What is likely to happen to the revenue of gas producers? Explain.arrow_forwardMacmillan Learning Consider two markets: the market for coffee and the market for hot cocoa. The initial equilibrium for both markets is the same, the equilibrium price is $4.50, and the equilibrium quantity is 35.0. When the price is $12.75, the quantity supplied of coffee is 71.0 and the quantity supplied of hot cocoa is 105.0. For simplicity of analysis, the demand for both goods is the same. Using the midpoint formula, calculate the elasticity of supply for hot cocoa. Please round to two decimal places. Incorrect Supply in the market for coffee is less elastic than supply in the market for hot cocoa.arrow_forward

- USE TABLE #1: If the price of electric automobiles dropped by 50% from the market price, the electric automobiles market would be faced with excess demand, or more specifically, a __________ (type either surplus or shortage), which means quantity __________________ (type either demanded or supplied) is greater than the quantity ____________ (type either demanded or supplied). (Spell all words correctly, choosing the correct word to fit the box)arrow_forwardConsider the market for Teslas. The price of gasoline decreases and the cost of producing Tesla batteries decrease. How will the market for Teslas respond? a prices will fall and the equilibrium quantity may or may not change. b prices will fall and the equilibrium quantity will decrease. c prices will fall and the equilibrium quantity will increase. d There is not enough information to answer the questionarrow_forwardDiscuss the determinants of demand and supply and how they affect the equilibrium price and quantity in a market.arrow_forward

- Below are the supply and demand schedules for a video game. Price $200 $180 $160 $140 $120 $110 $100 $90 $80 $60 Quantity Demanded 10 15 20 25 30 35 40 45 50 55 Quantity Supplied 100 90 80 70 60 50 40 30 20 10 a) What is the equilibrium price? $ b) What is the equilibrium quantity? Assume that this video game receives a poor rating and consumers decide to purchase 45 less at each price. c) What is the new equilibrium price? $ d) What is the new equilibrium quantity? 100 40 units unitsarrow_forwardChapter 2 Problem #5. Suppose the demand and supplycurves for a product are given by QD= 500 −2PQS=−100 + 3Pa. Graph the supply and demand curves.b. Find the equilibrium price and quantity.Qd= Q3500-2P= -100+3PP= Pe = 120 & Qe=260The equilibrium price is $120 and the quantity is 260c. If the current price of the product is $100, what is thequantity supplied and the quantity demanded? How would you describe thissituation, and what would you expect to happen in this market?d. If the current price of the product is $150, what is thequantity supplied and the quantity demanded? How would you describe thissituation, and what would you expect to happen in this market?e. Suppose that demand changes to QD= 600 – 2P.Find the new equilibrium price and quantity, and show this on your graph.***PLEASE SHOW ALL EQUATIONS AND METHODS,arrow_forwardEquilibrium: Where Supply Meets Demand - End of Chapter Problem rise and the equilibrium price will a. If the supply of green tea rises, the equilibrium quantity will is because the equilibrium quantity moves down the demand curve to a lower price and a higher quantity demanded b. Shift the appropriate curve or curves below to show the effect of this change. Market for Green Tea S fall . Thisarrow_forward

- Suppose Disney+ changes its monthly subscription price from $7 to $9 per month. Graphically show the impact of this price change in the following markets: a. Popcorn, pizza, and other movie snacks Instructions: Drag the supply or demand curve to its new position. b. Netflix Instructions: Drag the supply or demand curve to its new position.arrow_forwardThe demand and supply curves for a product are given by: Qd = 600 - 2P Qs = 300 + 4P Find the equilibrium price and the equilibrium quantity. Carefully draw a graph to illustrate your answer. Make sure to write out the intercepts. Show the equilibrium price and the equilibrium quantity on your graph.arrow_forwardUSE TABLE #1: The supply curve intersects with the price axis at $_____. (Remember to use a comma, if a comma is needed and to include the decimal point and two numbers to the right of the decimal point).arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education