ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

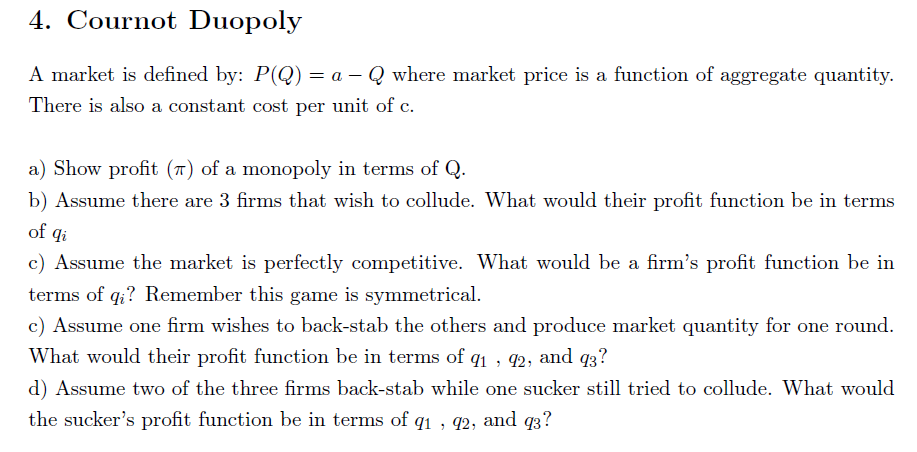

Transcribed Image Text:4. Cournot Duopoly

A market is defined by: P(Q) = a – Q where market price is a function of aggregate quantity.

There is also a constant cost per unit of c.

a) Show profit (π) of a monopoly in terms of Q.

b) Assume there are 3 firms that wish to collude. What would their profit function be in terms

of qi

c) Assume the market is perfectly competitive. What would be a firm's profit function be in

terms of qi? Remember this game is symmetrical.

c) Assume one firm wishes to back-stab the others and produce market quantity for one round.

What would their profit function be in terms of q1, 92, and 93?

d) Assume two of the three firms back-stab while one sucker still tried to collude. What would

the sucker's profit function be in terms of 91, 92, and 93?

SAVE

AI-Generated Solution

info

AI-generated content may present inaccurate or offensive content that does not represent bartleby’s views.

Unlock instant AI solutions

Tap the button

to generate a solution

to generate a solution

Click the button to generate

a solution

a solution

Knowledge Booster

Similar questions

- 3. Demand for a good produced by a duopoly is given by P = 100 - Q. Both firms have constant marginal costs, MC = 20 and zero fixed costs. Firms can choose to maximize profit or revenue. Suppose firm 1 choose to maximise profit and firm 2 choose to maximise revenue. Determine the equilibrium price and quantity of each firm.arrow_forward17. Demand is given by Q = 220 P. Marginal cost is $120. Calculate the market equilibrium price, output, and any profits for: a. b. C. a monopoly context ? a Bertrand duopoly a Cournot duopolyarrow_forwardCan you help me solve this please?arrow_forward

- Consider the following two industries the yogurt and automobile industry. Which industry would fit best into the category of monopolistic competition? Make sure you relate the most relevant economic concepts and theory to justify arguments.arrow_forward1. Consider a Cournot duopoly with the inverse demand P = 260 - 2Q. Two firms compete choosing their quantities. Both firms have constant. marginal and average cost MC = AC = 20. a. Find each firm's best response function. b. Find the Cournot equilibrium. c. Plot the best response curves and illustrate the equilibrium point.arrow_forwardnot use ai pleasearrow_forward

- MONOPOLISTIC COMPETITION 1. Suppose that the cost of production is given by the following function: CT = 100 + Q2 and that the demand is given by P = 80 - Q. a. Determine the level of maximization.b. Determine the value of CT and ITc. Check that the IMg = CMg CT (Total cost) IMg (marginal income) CMg (marginal cost) Algebraically if the demand curve in the monopoly is a function of quantity, the demand curve is a straight line. P = a - bQWhere a is the ordinate to the origin, b the slope and Q the quantitySo if IT = P x QWe have that (a - bQ) Q = aQ - bQ2IT = aQ - bQ2And therefore the marginal income is the derivative of IT or what is equal to the variation of total income between the variation of the quantity.Therefore the IMg = derive the quantity in the function aQ - bQ2IMg = a - 2bQ Consider these functions when conducting monopoly exercises.arrow_forwardConsider the following scenario in a duopoly with homogeneous products: Marginal cost: $21 Market demand: 972 units Competitor's price: $41 Your price: $44 Assuming your competitor maintained their price, what would be your pricing response, and how many units would you expect to sell at that new price? (Enter dollar amounts to the nearest penny and units to the nearest whole number.) Pricing response: Sales: $ unitsarrow_forwardquestion d e farrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education