ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Solute question4 please

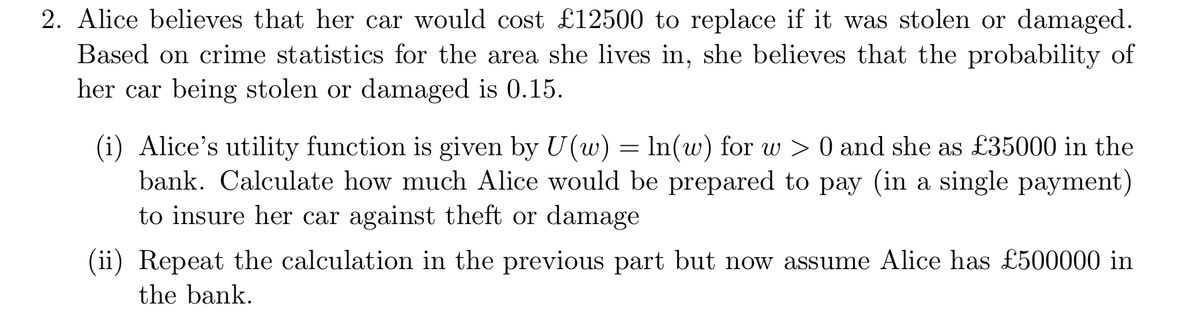

Transcribed Image Text:2. Alice believes that her car would cost £12500 to replace if it was stolen or damaged.

Based on crime statistics for the area she lives in, she believes that the probability of

her car being stolen or damaged is 0.15.

(i) Alice's utility function is given by U(w) = ln(w) for w > 0 and she as £35000 in the

bank. Calculate how much Alice would be prepared to pay (in a single payment)

to insure her car against theft or damage

(ii) Repeat the calculation in the previous part but now assume Alice has £500000 in

the bank.

Transcribed Image Text:4. Assume that a risk-free money market account is added to the market described in Q2.

The continuously compounded rate of return on the money market account is 0% per

period.

(i) Use the method of Lagrange multipliers to determine the proportions of wealth

invested in the three assets available for the minimum variance portfolio with

expected return μ. Your answer must express the proportions as a function of µ.

(ii) Recall that the market portfolio has highest Sharpe ratio. Formulate the optimi-

sation problem which characterises the market portfolio. You don't have to solve

this optimisation problem.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- How is elasticity related to logarithms?arrow_forwardC Get Homework Help With Chegg X Content O bblearn.uca.edu/ultra/courses/_130806_1/cl/outline?legacyUrl=-2Fwebapps-2Fcalendar-2Flaunch-2Fattempt-2F_blackboard.platform.gradeb. e ☆ E Apps I mylJCA M khapper2cubuc. H O Alpha Sigma Alpha. É iClaud O Pinterest b View My Activity I Olher bokmarks Micrasoft Office Ho. Blarkb:ard ECON 2320-TBA 0000-PRINCIPLES OF MACROECONOMICS - 31353.202220 Smartwork5: Ch. 11: Homework * SUBMIT ANSWER 15 OF 17 QUESTIONS COMPLETED 2:52 PM P Type here to search 20% O 69"F Mostly cloudy 描 3/6/2022arrow_forwardplz solve both parts within 30-40 mins I'll give upvotearrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education