ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

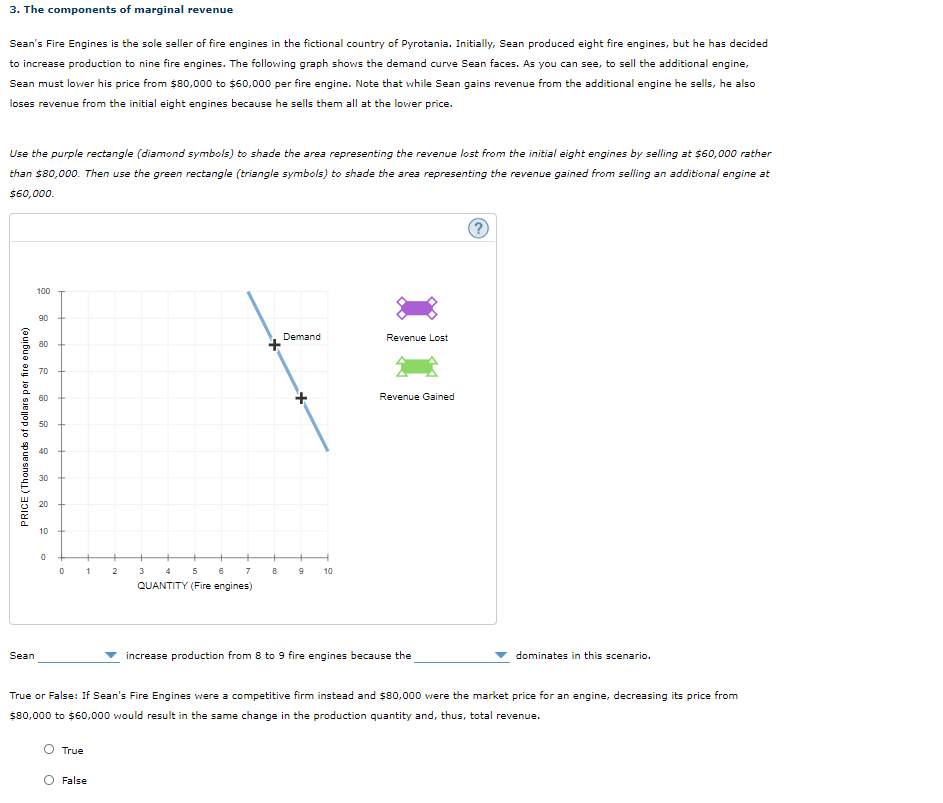

Transcribed Image Text:3. The components of marginal revenue

Sean's Fire Engines is the sole seller of fire engines in the fictional country of Pyrotania. Initially, Sean produced eight fire engines, but he has decided

to increase production to nine fire engines. The following graph shows the demand curve Sean faces. As you can see, to sell the additional engine,

Sean must lower his price from $80,000 to $60,000 per fire engine. Note that while Sean gains revenue from the additional engine he sells, he also

loses revenue from the initial eight engines because he sells them all at the lower price.

Use the purple rectangle (diamond symbols) to shade the area representing the revenue lost from the initial eight engines by selling at $60,000 rather

than $80,000. Then use the green rectangle (triangle symbols) to shade the area representing the revenue gained from selling an additional engine at

$60,000.

PRICE (Thousands of dollars per fire engine)

Sean

100

90

80

70

40

10 ++

0

0

1

True

+

2

False

3 4 5

QUANTITY (Fire engines)

6

7

8

Demand

9 10

Revenue Lost

Revenue Gained

increase production from 8 to 9 fire engines because the

?

True or False: If Sean's Fire Engines were a competitive firm instead and $80,000 were the market price for an engine, decreasing its price from

$80,000 to $60,000 would result in the same change in the production quantity and, thus, total revenue.

dominates in this scenario.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Suppose she runs a small business that manufactures teddy bears. Assume that the market for teddy bears is a competitive market, and the market price is $20 per teddy bear.arrow_forwardSub : EconomicsPls answer very fast.I ll upvote. Thank Youarrow_forward10. Figure 5 shows the graph of the short-run cost curves for Tim-T-Shirts, a firm operating in a perfectly competitive market. P* denotes the current price for Tim T-Shirts. Based on the information in the graph, which of the following should we expect in the long run? a) New firms will enter the market. b) The number of firms in the market will remain unchanged. c) Gray Sweaters will increase the current price of sweaters. d) There is not enough information to answer the question. Figure 5 Price and Costs P* MC ATC AVC Quantityarrow_forward

- Hand written solutions are strictly prohibitedarrow_forwardWhat is a price taker? A price taker is A. a firm with a perfectly inelastic demand curve. B. a firm that has the ability to charge a price greater than marginal cost. C. a firm that is unable to affect the market price. D. a firm that does not seek to maximize profits. E. a firm with a downward-sloping demand curve. When are firms likely to be price takers? A firm is likely to be a price taker when A. it has market power. B. firms in the industry collude. C. it sells a differentiated product. D. it represents a small fraction of the total market. E. barriers to entry are substantial.arrow_forwardThe graph below plots the firm's total revenue curve: that is, the relationship between quantity and total revenue given by the two right columns in the table above. The five choices are also labeled. Finally, two black lines are shown; these lines are tangent to the green curve at points B and D. 90 81 72 63 54 В D 45 36 27 18 A E 100 200 300 400 500 600 700 800 QUANTITY (Dishwashers per year) TOTAL REVENUE (Thousands of dollars per year)arrow_forward

- 20. Paulina sells beef in a competitive market where the price is $6 per pound. Her total revenue and total costs are given in the table below. Fill out the table. At what quantity does marginal revenue equal marginal cost? What is the profit-maximizing quantity?arrow_forwardPlease do fast and add explanation , diagramarrow_forwardAustin is a dot-com entrepreneur who has established a Web site at which people can design and buy awatch. Austin pays $900 a month for a Web server and Internet connection. The watches that customers design are made to order by another firm, and Austin pays this firm $120 a watch. Austin has no other costs. The table shows the demand schedule for Austin's watches. Austin is making an economic profit. In the long run, the demand for Austin's watches OA. decreases; incurs an economic loss OB. increases; makes zero economic profit C. increases, increases his economic profit D. decreases; makes zero economic profit OE. decreases; shuts down and in long-run equilibrium, Austin MIER Price (dollars per watch) 200 160 120 80 40 0 Quantity (watches per month) 0 40 80 120 160 200arrow_forward

- For “Developing a Sampling Plan for a New Menu Initiative Survey,” page 163 Owners of the Santa Fe Grill realize that in order to remain competitive in the restaurant industry, new menu items need to be introduced periodically to provide variety for current customers and to attract new customers. Recognizing this, the owners of the Santa Fe Grill believe three issues need to be addressed using marketing research. The first is should the menu be changed to include items beyond the traditional southwestern cuisine? For example, should they add items that would be considered standard American. Italian. or European cuisine? Second, regardless of the cuisine to be explored, how many new items (e.g., appetizers, entrées, or desserts) should be included on the survey? And third, what type of sampling plan should be developed for selecting respondents, and who should those respondents be? Should they be current customers, new customers, and/or old customers? Determine the appropriate sample…arrow_forwardUse the above figure. Total revenue at the profit-maximizing output isarrow_forwardThe figure below depicts the market supply and demand for the perfectly competitive rollerblade industry. S Price per pair of Rollerblades 1,140 070 50 150 Number of pairs of Rollerblades per week Based on the figure above, if the current quantity demanded of rollerblades is 150 per week, you accurately predict that in the short run, Q Select one: a. price and quantity supplied will increase and quantity demanded will decrease. b. price and quantity supplied will decrease and quantity demanded will increase. c. price, quantity supplied and quantity demanded will increase. d. price, quantity supplied and quantity demanded will decrease.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education