ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

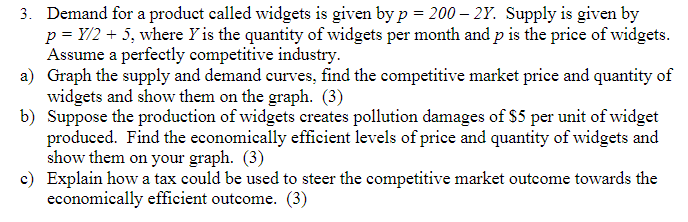

Transcribed Image Text:3. Demand for a product called widgets is given by p= 200 - 2Y. Supply is given by

p = Y/2 + 5, where Y is the quantity of widgets per month and p is the price of widgets.

Assume a perfectly competitive industry.

a) Graph the supply and demand curves, find the competitive market price and quantity of

widgets and show them on the graph. (3)

b) Suppose the production of widgets creates pollution damages of $5 per unit of widget

produced. Find the economically efficient levels of price and quantity of widgets and

show them on your graph. (3)

c) Explain how a tax could be used to steer the competitive market outcome towards the

economically efficient outcome. (3)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 5 steps with 5 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A large share of the world supply of cocoa beans comes from Ghana and Ivory Coast. Suppose that the marginal cost of producing cocoa beans is constant at GHC1000 per bag and the demand for cocoa beans is described by the following schedule. Price (GHC) Quantity (bags) 5000 6000 7000 8000 9000 10000 11000 12000 8000 7000 6000 5000 4000 3000 2000 1000 a) If there were many suppliers of cocoa beans, what would be the price and quantity? b) If there were only one supplier of cocoa, what would be the price and quantity? c) At a meeting in October 2017 in Accra, the leaders of the two leading producers of cocoa beans discussed the possibility of cooperating to boost the price of cocoa. If Ghana and Ivory Coast formed a cartel, what would be the price and quantity? If the countries split the market evenly, what would be Ghana's production and profit? f) What would happen to Ghana's profit if it increased its production by 1000 cocoa while Ivory Coast stuck to the cartel agreement? g) Use your…arrow_forward1. There are two brands of cigarettes X, Y. The demand for each is as follows: Qx = 80 - 2p Qy = 60 - 0.5p Assume that the marginal cost of producing cigarette X is $10, the marginal cost of producing cigarette Y is $8, and that the market for both cigarettes is perfectly competitive. Assume that each pack of cigarette X smoked does $5 worth of health damage to the smoker, and a total of $4 worth of health damage to the smoker’s neighbors via second-hand smoke. Each pack of cigarette Y smoked does $6 worth of health damage to the smoker, and $5 health damage to the smoker’s neighbors. (a) Explain why the public supply curves differ from the private supply curves, and how this represents the externality from second-hand smoke. Highlight the area(s) of your diagram that represents a social loss. (b) Calculate the social loss for both. (c) Suppose the government decides to pursue a Pigouvian solution to eliminate social loss. What's amount of tax or subsidy would the government…arrow_forwardOnly part (b) please, thank you!arrow_forward

- 4. Consider two markets for the same good: markets 1 and 2. The demand for the good on these markets are: P₁ = 20 2Q₁ and P2 = 40-2Q2 The total cost of producing any output Q is c(Q) = 10 + 8Q where Q = 9₁ +92. (a) Suppose these two markets are completely separated but each is served by a per- fectly competitive industry. What will be the prices and outputs supplied to cach of the two markets?arrow_forwardSolve all this question......you will not solve all questions then I will give you down?? upvote....arrow_forwardSuppose that pig farming in a region is a perfectly compet- itive industry. However, one negative consequence of this activity is that it creates water pollution that adversely affects the health of the residents in the nearby communities that rely on the water sources that are contaminated by the pig farms. The market supply curve for pigs (or hogs) is given by H^S = 6p where H^S is the quantity of hogs supplied to the market by farmers in this region. The market demand for hogs is given by H^P = 300 – 4p. The government estimates that the additional medical costs (M) imposed on the nearby communities is given by M = 5H, where H is the quantity of hogs produced and sold in the market. Q: In the absence of clearly defined property rights over water use or con- ventions or some form of government intervention, derive the market equilibrium for hogs and the DWL resulting from the additional medical costs associated with hog production. Please show the formula, thank you.arrow_forward

- The tables (below) show the willingness to pay by three (competitive) consumers for additional units of some good, and the marginal costs of three (competitive) firms that produce that good. a) Compute the competitive equilibrium quantity and price for this market. Also, compute each consumer's surplus and each firm's profits. b) Now suppose that you have access to the same technology (and competitive input markets) as that of Firm 3. Entering the market (that is, launching a fourth firm) means a fixed (yes, sunk too) cost of $10. Would you decide to enter? (Entry has effects on the market, of course.) c) With the same data, suppose that all three firms merge. That is, now a single corporation controls (and decides on output for) all three firms (now, plants of one single firm). Obtain the output (or, equivalently, the price) that this monopolistic corporation will choose, and evaluate the consequences for the consumers (that is, the effect on the consumer surplus) and for the profits…arrow_forwardQ8. What role does the U.S. government play with respect to market competition? a.) It preserves competition by regulating prices and intervening in the price and output decisions of businesses. b.) It preserves competition by maintaining abundant government-owned firms to ensure consumer-friendly pricing. c.) It polices anticompetitive behavior and prohibits contracts that restrict competition.arrow_forwardAnswer the following for the given example (for a perfectly competitive market): Your neighbours holding a physical gathering during the pandemic (a) Does an externality exist? If so, is it positive/negative (or both) (b) Use Coase’s framework to identify the cause of the externality (c) If an externality exists, determine whether the Coase theorem applies (i.e. is it possible/feasible to assign property rights and solve the problem?). Provide reasoning. (d) If an externality exists and the Coase theorem does not apply, discuss a government/institutional solution that can mitigate the problem of externality. Provide reasoning.arrow_forward

- Let’s consider an economy where all firms are favouring remote work to favour physical distancing and avoid the spread of a virus. To achieve these goals all firms receive a subsidy to equip their workers with a laptop. Consider that the market for laptops is in perfect competition and initially at the equilibrium. Explain the impact of the pandemic on the supply, demand, equilibrium on market of computers. Give a graphical representationarrow_forwardSketch the microeconomics graph of the article, Industrial Demand for platinum driving significant supply shortfallarrow_forwardPlease help me with this question correctly. Thank youarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education