ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

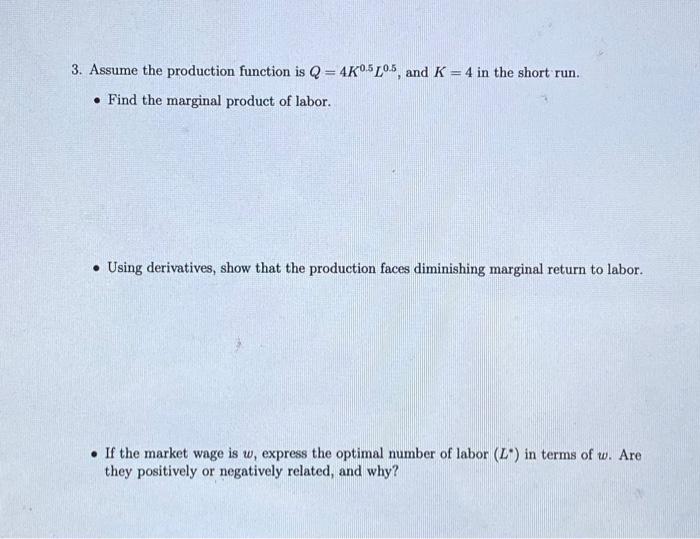

Transcribed Image Text:3. Assume the production function is Q = 4K0.5L05, and K = 4 in the short run.

Find the marginal product of labor.

Using derivatives, show that the production faces diminishing marginal return to labor.

If the market wage is w, express the optimal number of labor (L) in terms of w. Are

they positively or negatively related, and why?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- please helparrow_forwardSolve the exercise with a production function with diminishing returns: In this case, production increases as workers are added, but it increases less and less. a) Calculate the amount of production for each worker and add it to the table, taking into account the production function K 10 1 9. 2 8 3 7 4 6. 4 7 3 8 2 9 10 b) Explain why the production function exhibits diminishing returns to scale.arrow_forwardShow full answers and steps to the exercisearrow_forward

- Suppose the production function of a firm is given as: Q = 5L + 10L2 – 2L3 Find the number of labors that would yield maximum values of TP, AP, and MP? Base on the results on “a”, provide a range of values that would reflect the three stages of production.arrow_forwardIf the marginal product of labor is 25 and the marginal product of capital 10, what is the marginal rate of technical substitution of labor for capital?arrow_forwardprovide me with exact calculation and answers plz! will leave thumbs up if helpsarrow_forward

- Which of the following statements is (are) TRUE?I. If labor and capital are perfect substitutes in production, the isoquant is a downward-sloping line.II. If a company needs to use inputs in fixed proportion such that the capital to labor ratio is always 2, the firm's isoquants are L-shaped.III. If the production function is given by Q = min(14, 7), the firm can produce, at minimum, 21 units of output. IIII, II, and IIIII and II Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardSuppose that production q, capital k and labour 1 satisfy g(q, k, 1) = O. In other words, the production function q(k, I) is defined implicitly, and it satisfies g(q(k, I),k, 1) = 0 identically. How do you think we might calculate the partial derivatives in a manner similar to that developed in this chapter for functions g of only two variables? Illustrate your method by working out the partial derivatives when q is defined by the equation q3k2 +l3 +qkl = O.arrow_forwardthankyouarrow_forward

- A Firm's Optimization with CES Production Function The Constant Elasticity of Substitution (CES) production function is a flexible way to describe how a firm combines capital and labor to produce output, allowing for different levels of substitutability between the two inputs. The elasticity of substitution, denoted by σ, measures how easily the firm can substitute capital for labor (or vice versa) while maintaining the same output level. The parameter p is related to the elasticity of substitution by the formula σ = 1/(1 - p). Now, let's consider a firm that operates for two periods (t and t + 1) and produces output according to the CES production function: F(Kt, Nt) = [aK{ + (1 − a)N]¹º 0arrow_forwardSuppose a production function is given by the equation Q = LVK. 1. Graph the isoquants corresponding to Q = 10, and Q = 20. 2. MP = √K and MP = 0.5(L/VK). Find the Marginal Rate of Technical Substitution LK (MRTSLK). Do these isoquants exhibit diminishing marginal rates of technical substitution? (Does the slope get flatter as L increases?) 3. The cost of labor is w = $5 per labor hour and the cost of capital is r = $15 per machine hour. What is the equation of the $1500 iso-cost curve?arrow_forwardB. Suppose that your production process is characterized by the production function x = f(e) = 100 In ( + 1). For purposes of this problem, assume w > 1 and p > 0.01. a. Set up your profit-maximization problem. b. Derive the labor demand function. C. The labor demand curve is the inverse of the labor demand function with p held fixed. Can you demonstrate what happens to this labor demand curve when p changes? d. Derive the output supply function. e. The supply curve is the inverse of the supply function with w held fixed. What happens to this supply curve as w changes? (Hint: Recall that In x = y implies e' = x, where e ≈ 2.7183 is the base of the natural log.) f. Suppose p = 2 and w profit will you make? = 10. What is your profit-maximizing production plan, and how mucharrow_forwardarrow_back_iosSEE MORE QUESTIONSarrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education