Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

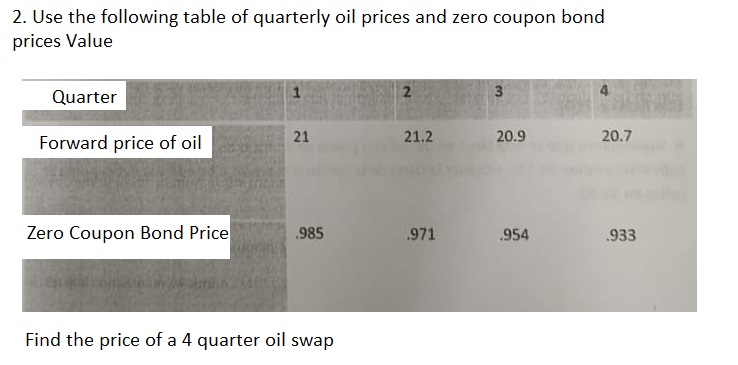

Transcribed Image Text:2. Use the following table of quarterly oil prices and zero coupon bond

prices Value

Quarter

Forward price of oil

Zero Coupon Bond Price

21

.985

Find the price of a 4 quarter oil swap

2

21.2

.971

3

20.9

.954

20.7

.933

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Consider the following quote for a for a treasury bond. Maturity Coupon Bid Ask Chg Ask Yield 5/15/2030 6.250 132.8984 132.9609 0.4688 2.949 What was the bid-ask spread? Respuesta:arrow_forwardQ2. Consider 3 zero coupon bond: Maturity Yld: 10 1.50%; 20 2.00%; 30 2.25% Q2a. calculate duration and convexity, dollar duration and dollar convexity for all three Q2b. how to hedge the duration risk of a 100M position in 20Y with 10Y and with 30Y respectively? Q2c. What is the dur and convexity effect of 5 bps steepening caused by 10Y up 10 bps; 20Y up 15 bps for the 10 vs 20Y trade?? Q2d. What is the dur and convexity effect of 5 bps flattening caused by 20Y up 15 bps; 30Y up 10 bps for the 20 vs 30Y trade?arrow_forwardQ12arrow_forward

- Consider the prices of the following three Treasury issues as of February 24, 2021: Maturity Bid Change Yield -15 5.34 May 2025 May 2025 Ask 118:16 118:18 103:16 103:18 134:20 134:26 -5 5.30 May 2025 -15 5.38 Coupon 6.920 8.370 12.180 The bond in the middle is callable in February 2022. What is the implied value of the call feature? (Hint: Is there a way to combine the two non-callable issues to create an issue that has the same coupon as the callable bond?) (Do not round intermediate calculations. Round the final answer to 2 decimal places. Omit $ sign in your response.) Call value GA 19.41arrow_forward3. Interest rate swap. Consider a portfolio of floating-rate bonds that all mature in three years. What is the fixed coupon rate for a fairly priced fixed-for-floating interest rate swap given the following discount factors? Years 2. 0.,95 06'0 0.86arrow_forwardaa.4arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education