ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

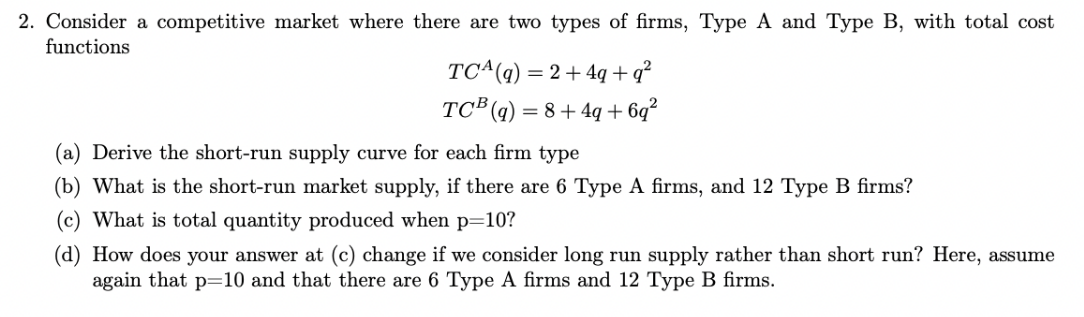

Transcribed Image Text:2. Consider a competitive market where there are two types of firms, Type A and Type B, with total cost

functions

TC(q) = 2+4q+q²

TCB (q) = 8+4q+6q²

(a) Derive the short-run supply curve for each firm type

(b) What is the short-run market supply, if there are 6 Type A firms, and 12 Type B firms?

What is total quantity produced when p=10?

(d) How does your answer at (c) change if we consider long run supply rather than short run? Here, assume

again that p=10 and that there are 6 Type A firms and 12 Type B firms.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Please no written by hand solution Question 1: The wheat market is perfectly competitive, and the market supply and demand curves are given by the following equations: QD = 20,000,000 - 4,000,000P QS = 7,000,000 + 2,500,000P, where QD and QS are quantity demanded and quantity supplied measured in bushels, and P = price per bushel. a. Determine consumer surplus at the equilibrium price and quantity. Provide a fully labelled diagram to support your answer. Show all intercepts, equilibrium label axis and curves fully.arrow_forwardPROBLEM (4) The short run market supply for shirts is QS = 50P – 1000 and the market demand isQD = 2800 – 50P Let a typical firm operating in a perfectly competitive industry has short-run total cost and marginal cost curves: TC(q) = 100 + 20q + q2 and MC(q) = 20 + 2q (a) Determine the short run market equilibrium price and quantity for this type of shirt.(b) Determine how much the typical firm will produce at the equilibrium price you found in (a).(c) If all firms had the same cost structure, how many firms should be operating in this industry at the moment? (d) Calculate the profit or loss of each firm at the short-run market equilibrium. If they are making losses, why are they still producing in the short run? In the long run, will there be entry into the market or exit from it?(e) What would the price be in the long run equilibrium, assuming constant cost industry?(f) In the long run equilibrium, how many shirts would each firm produce? What would be a firm’s net profit?(g) How…arrow_forwardWhich of the following properties characterizes a perfectly competitive market? [(i) through (iv) are the properties; you will choose from options a, b, c, or d as your answer]. (i) Many buyers and many sellers. (ii) Perfectly inelastic demand curves for the individual producers. (iii) Goods offered for sale are identical with perfect substitutes. (iv) All producers are price takers.arrow_forward

- 4. Consider two markets for the same good: markets 1 and 2. The demand for the good on these markets are: P₁ = 20 2Q₁ and P2 = 40-2Q2 The total cost of producing any output Q is c(Q) = 10 + 8Q where Q = 9₁ +92. (a) Suppose these two markets are completely separated but each is served by a per- fectly competitive industry. What will be the prices and outputs supplied to cach of the two markets?arrow_forward2.- A company that works in a perfectly competitive market has a total cost function: TC = Q3 - 52.5Q2 + 1,050Q + 6,750 The supply and demand functions in that market are: QS = 2P -704 Qd = 5,260 - 5P d) Calculate the market consumer surplus. e) Validate the utilities by calculating them as the area of the rectangle on the graph.arrow_forwardConsider a perfectly competitive market for a product Y and assume that the market is at the long run equilibrium. (a) Examine the cost structure and demand faced by an individual Y producer. Relate that producer to the Y market at the perfectly competitive long run equilibrium. Support with market and individual producer diagrams. (b) Analyze the effects of the following news on price and quantity in the Y market as well as the profit and output of the individual Y producer “It is discovered that consuming Y is beneficial to health and can prolong your life”. Explain both the short run and the long run equilibria and support your answers with suitable diagrams. Hi, I have the answer sheet but may I request for a more detailed explanation for part b? Thank you.arrow_forward

- 3] Assume several identical firms have the short run production function Q = √40L and pay a wage of 10 for each unit of labor employed. Fixed costs for each firm are 100. The market demand for the good is Qd = 100,000.25P. How many firms are in the industry in the long run?arrow_forwardConsider a competitive market where there are two types of firms, Type A and Type B, with total cost functions TC^(q) =1+2q + q² TC (g) = 6+2q + 3q? (a) Derive the short-run supply curve for each firm type (b) What is the short-run market supply, if there are 10 Type A firms, and 6 Type B firms? (c) What is total quantity produced when p=5? (d) How does your answer at (c) change if we consider long run supply rather than short run? Here, assume again that p=5 and that there are 10 Type A firms and 6 Type B firms.arrow_forward1.- A company that works in a perfectly competitive market has a total cost function: TC = Q3 - 36Q2 + 540Q + 600 The supply and demand functions in that market are: QS = 5P -500 Qd = 4,000 -10P a) How much should you produce to maximize your profits? b) Find what benefit you will get c) Calculate the closing point for the company d) Represent graphically the market equilibrium and that of the company, including the closing point e) Locate the rectangle that represents profits on the company's equilibrium graph. Calculate your área considering the values taken by the base and the height. Validate that it reaches the same result (or very close) to the one obtained in part b).arrow_forward

- 27) A firm in a perfectly competitive market has no control over price because A) there is free entry and exit from the industry. B) every firm's product is a perfect substitute for every other firm's product, and there is a very large number of firms in the industry. C) the government imposes price ceilings on the products produced in perfectly competitive industries. D) the market demand for products produced in perfectly competitive industries is perfectly elastic.arrow_forwardPROBLEM (4) The market for plastic toys is perfectly competitive, and it is composed of many identical firms, each with the total cost function TC(q) = ½ q² + 40q + 2,450 (a) What is the short run shut down price and the long run entry/exit price for this market? (b) Carefully draw the short run supply graph of an individual firm, and separately the long run aggregate (market) supply graph for this industry. (c) What is the optimal quantity to produce for the firm and the corresponding net profit, if the market price is (i) %3D $30? (ii) $70? Now, suppose in addition that the market demand is Q = 18,000 - 100p. (d) In the long run equilibrium, what is the market price and quantity? How many units does each firm in the market produce, and what is its net profit? How many firms are there in the long run equilibrium? (e) Suppose the government imposes a $14 per unit tax on plastic toys. Re-answer part (d) %3Darrow_forwardAssume that the cost data in the following table are for a purely competitive producer: Average Average Average Total Variable Marginal Cost Total Fixed Product Cost Cost Cost 1 $60.00 $45.00 $105.00 $ 45.00 30.00 42.50 72.50 40.00 3 20.00 40.00 60.00 35.00 4 15.00 37.50 52.50 30.00 12.00 37.00 49.00 35.00 6. 10.00 37.50 47.50 40.00 7 8.57 38.57 47.14 45.00 7.50 40.63 48.13 55.00 9. 6.67 43.33 50.00 65.00 10 6.00 46.50 52.50 75.00 Instructions: If you are entering any negative numbers be sure to include a negative sign (-) in front of those numbers. Select "Not applicable" and enter a value of "0" for output if the firm does not produce. a. At a product price of $57.00 (i) Will this firm produce in the short run? (Click to select) V (ii) If it is preferable to produce, what will be the profit-maximizing or loss-minimizing output? |(Click to select V output = units per firm (iii) What economic profit or loss will the firm realize per unit of output? |(Click to select v per unit = $ b.…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education