ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

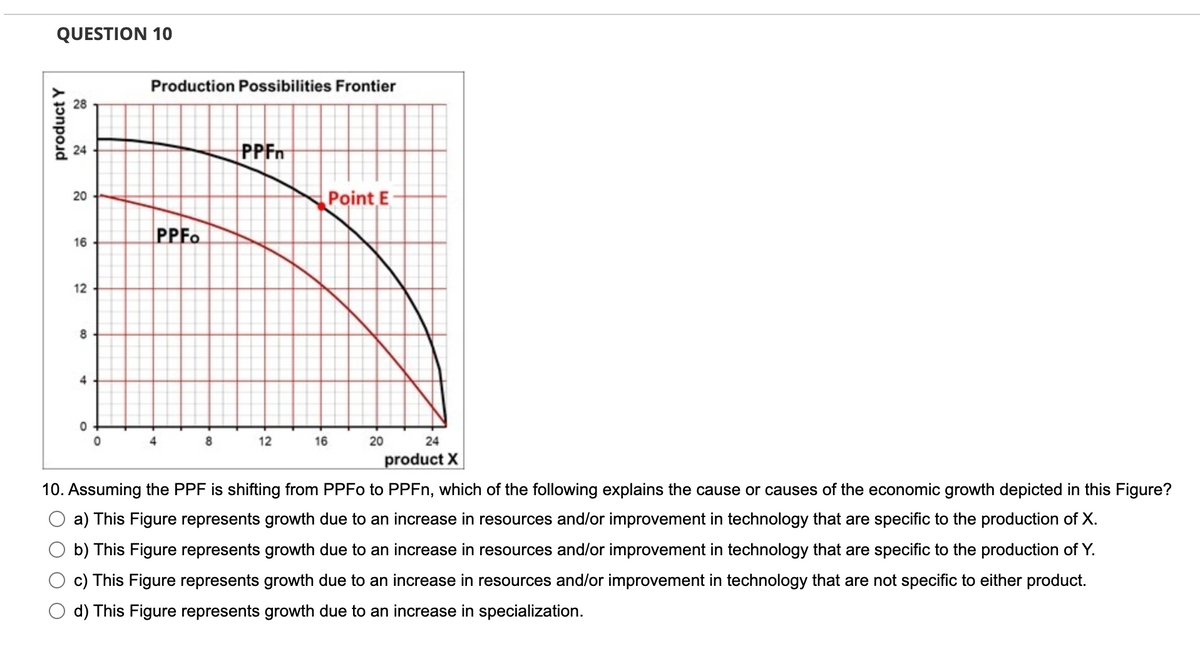

Transcribed Image Text:QUESTION 10

product Y

28

24

20

16

12

8

4

0

0

Production Possibilities Frontier

PPFO

4

8

PPFn

12

16

Point E

20

24

product X

10. Assuming the PPF is shifting from PPFO to PPFn, which of the following explains the cause or causes of the economic growth depicted in this Figure?

a) This Figure represents growth due to an increase in resources and/or improvement in technology that are specific to the production of X.

b) This Figure represents growth due to an increase in resources and/or improvement in technology that are specific to the production of Y.

This Figure represents growth due to an increase in resources and/or improvement in technology that are not specific to either product.

d) This Figure represents growth due to an increase in specialization.

Expert Solution

arrow_forward

Step 1: Define production possibility frontier (PPF):

It can be defined as the graphical representation of the combination of two products that can be produced by an individual or an economy by using the given level of inputs and technology efficiently in a particular period of time.

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- QUESTION 11 Using the Rule of 70, a country will roughly double its GDP in thirty-five years if its annual growth rate is However, if its annual growth rate is 5%, its GDP will roughly double in O 2 percent; 14 years O 7.5 percent; 10 years O 3.5 percent; 5 years O 2.5 percent; 25 yearsarrow_forwardProduction possibilities (alternatives) A Capital goods 5 Consumer goods 0 B 5 achieve economic growth. с 3 9 D 2 12 A achieve the full employment of available resources. B allocate its available resources most efficiently among alternative uses. use its resources more efficiently than the data in the table now indicate. E 1 14 F 0 Refer to the above table. For this economy to produce a total output of 3 units of capital goods and 13 units of consumer goods it must: 15arrow_forwardSuppose that we can produce 10 units of output with 5 units of labour and 5 units of capital. Which assumption on technology implies that this would mean that we can also produce 6 units of outpu with 5 units of labour and 5 units of capital? O Convexity O Non-reversibility O Additivity O Divisibility O Free-disposabilityarrow_forward

- According to the text, European countries' growth rates of real GDP per capita Select one: O a. decreased in the first two decades after 1980 and then increased in the following two decades. O b. decreased during each of the four decades beginning 1980. O c. followed a random pattern during the four decades beginning 1980. O d. remained constant during each of the four decades beginning 1980.arrow_forward1. Economic models Consider the following production possibilities frontier model for an economy that produces only two goods: bartey and cars. 100 80 PPF 20 20 40 60 60 100 BARLEY (Miions of busheis) CARS (Miions)arrow_forwardExplainarrow_forward

- Which of the following statements about the opportunity cost of economic growth is correct? The opportunity cost of economic growth O A. is human capital O B. is capital consumption O C. is greater the faster we make our production grow O D. is zeroarrow_forward3/25/22, 10:54 PM Assignment Print View 3. The graphs below show the production possibilities frontiers for apples and peaches in Italy and Turkey. (i Italy's Production Possibilities 4.0 3.6 3.2 2.8 A 2.4 2.0 1.6 1.2 0.8 0.4 Peaches (millions of tons) https://ezto.mheducation.com/hm.tpx?todo=c15SinglePrintView&singleQuestionNo=3.&postSubmissionView=13252718360410217&wid=13252718466068729&rol... 1/3 5.2 4.8 4.4 Y4.0 3.6 3.2 2.8 2.4 2.0 1.6 0.8 0.4 Apples (millions of tons)arrow_forwardI think my answer is right. How would you read this graph?arrow_forward

- Exhibit: Sugar and Freight Trains Tons of sugar per period 244 225 180 100 23 O 19 tons of sugar. 45 tons of sugar. 80 tons of sugar. O 3 freight trains. 2 3 O 4 Quantity of freight trains per period Suppose the economy is operating at point C. The opportunity cost of producing the fourth freight train would be:arrow_forwardN6arrow_forward1..arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education