FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

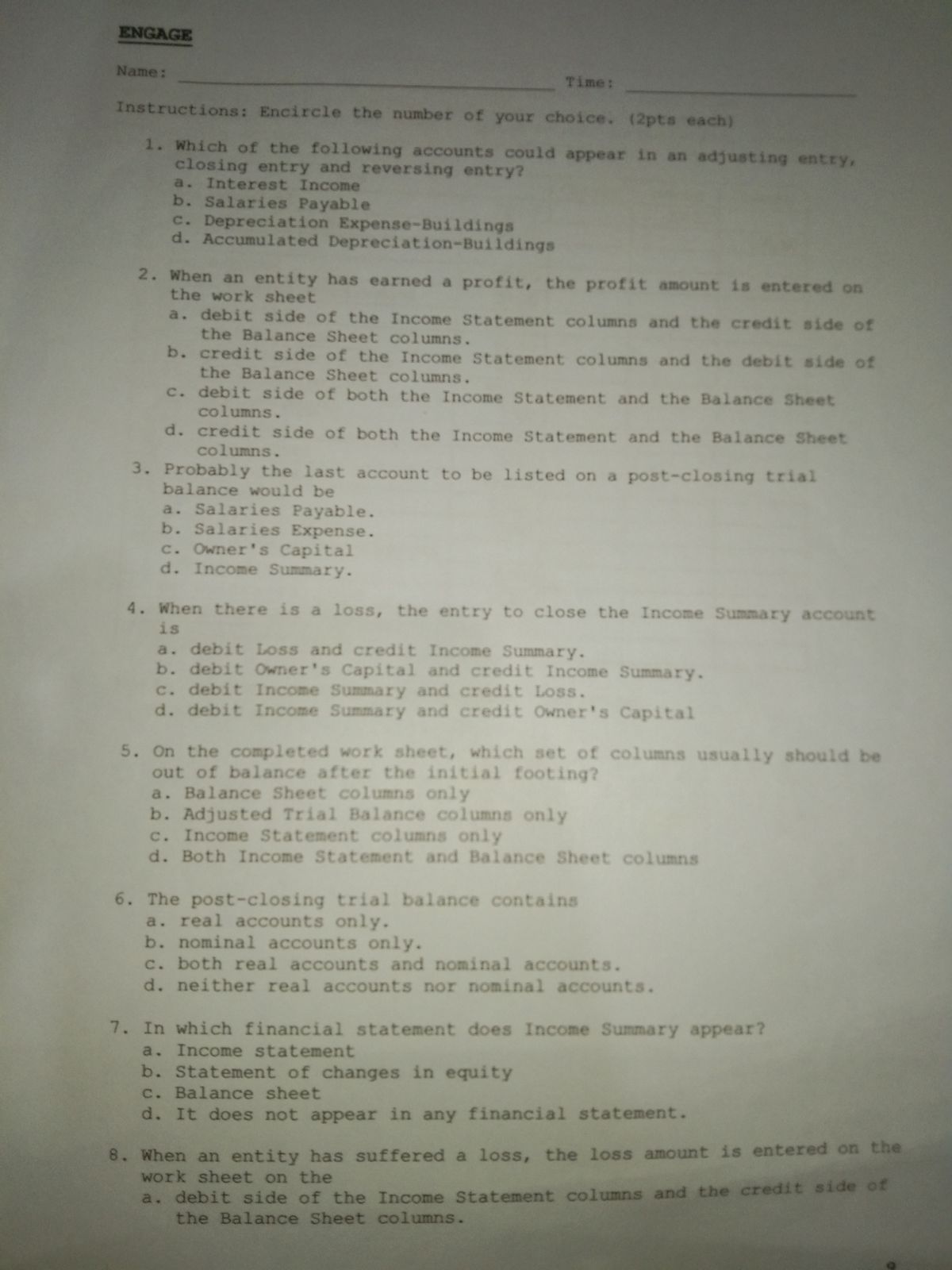

Transcribed Image Text:ENGAGE

Name:

Time:

Instructions: Encircle the number of your choice. (2pts each)

1. Which of the following accounts could appear in an adjusting entry,

closing entry and reversing entry?

a. Interest Income

b. Salaries Payable

c. Depreciation Expense-Buildings

d. Accumulated Depreciation-Buildings

2. When an entity has earned a profit, the profit amount is entered on

the work sheet

a. debit side of the Income Statement columns and the credit side of

the Balance Sheet columns.

b. credit side of the Income Statement columns and the debit side of

the Balance Sheet columns.

c. debit side of both the Income Statement and the Balance Sheet

columns.

d. credit side of both the Income Statement and the Balance Sheet

columns.

3. Probably the last account to be listed on a post-closing trial

balance would be

a. Salaries Payable.

b. Salaries Expense.

c. Owner's Capital

d. Income Summary.

4. When there is a loss, the entry to close the Income Summary account

is

a. debit Loss and credit Income Summary.

b. debit Owner's Capital and credit Income Summary.

c. debit Income Summary and credit Loss.

d. debit Income Summary and credit Owner's Capital

5. On the completed work sheet, which set of columns usually should be

out of balance after the initial footing?

a. Balance Sheet columns only

b. Adjusted Trial Balance columns only

c. Income Statement columns only

d. Both Income Statement and Balance Sheet columns

6. The post-closing trial balance contains

a. real accounts only.

b. nominal accounts only.

c. both real accounts and nominal accounts.

d. neither real accounts nor nominal accounts.

7. In which financial statement does Income Summary appear?

a. Income statement

b. Statement of changes in equity

c. Balance sheet

d. It does not appear in any financial statement.

8. When an entity has suffered a loss, the loss amount is entered on the

work sheet on the

a. debit side of the Income Statement columns and the credit side ot

the Balance Sheet columns.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- A change in depreciation method is a______. Select one: a. change in accounting standard b. change in accounting estimate c. change in accounting method d. change in accounting policyarrow_forwardThe adjusting entry to record depreciation includes a. a debit to an expense account. O b. a debit to a liability account. O c. a credit to stockholders' equity account. O d. a debit to an asset account.arrow_forwardRecording depreciation for a plant asset conforms to which accounting principle/assumption? OA. Matching Principle B. Time Period Assumption OC. Full Disclosure Principle OD. Revenue Recognition Principle***arrow_forward

- Explain an example to record the adjusting entry for accrued revenue.arrow_forwardDescribe the accounting changes in depreciation.arrow_forwardWhich of the following accounts could be part of a regular journal entry, an adjusting entry, a closing entry, and a reversing entry? interest revenue account receivable depreciation expense unearned revenue prepaid insurancearrow_forward

- Accounting Changes A material, prior period error impacting repairs expense.will affect which account(s) in subsequ O current liabilities O current assets O retained earnings operating expense Save for Later 12arrow_forwardOn the balance sheet, accumulated depreciation is: Group of answer choices subtracted from property and equipment. added to total liabilities. added to property and equipment. subtracted from total liabilities.arrow_forwardWhich of the following are all temporary accounts? a.Liabilities and assets b.Liabilities, revenue, and expenses c.Assets, liabilities, and owner's Drawing d.Revenue, expenses, and the Owner's Drawing e.Revenue, liabilities, and the owner's Drawingarrow_forward

- How would accumulated depreciation be classified on the balance sheet? current asset fixed asset current liability O long term liabilityarrow_forwardHow is the account Land classified and what kind of balance should it have? Group of answer choices fixed, credit current asset, debit fixed, debit current asset, creditarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education