ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

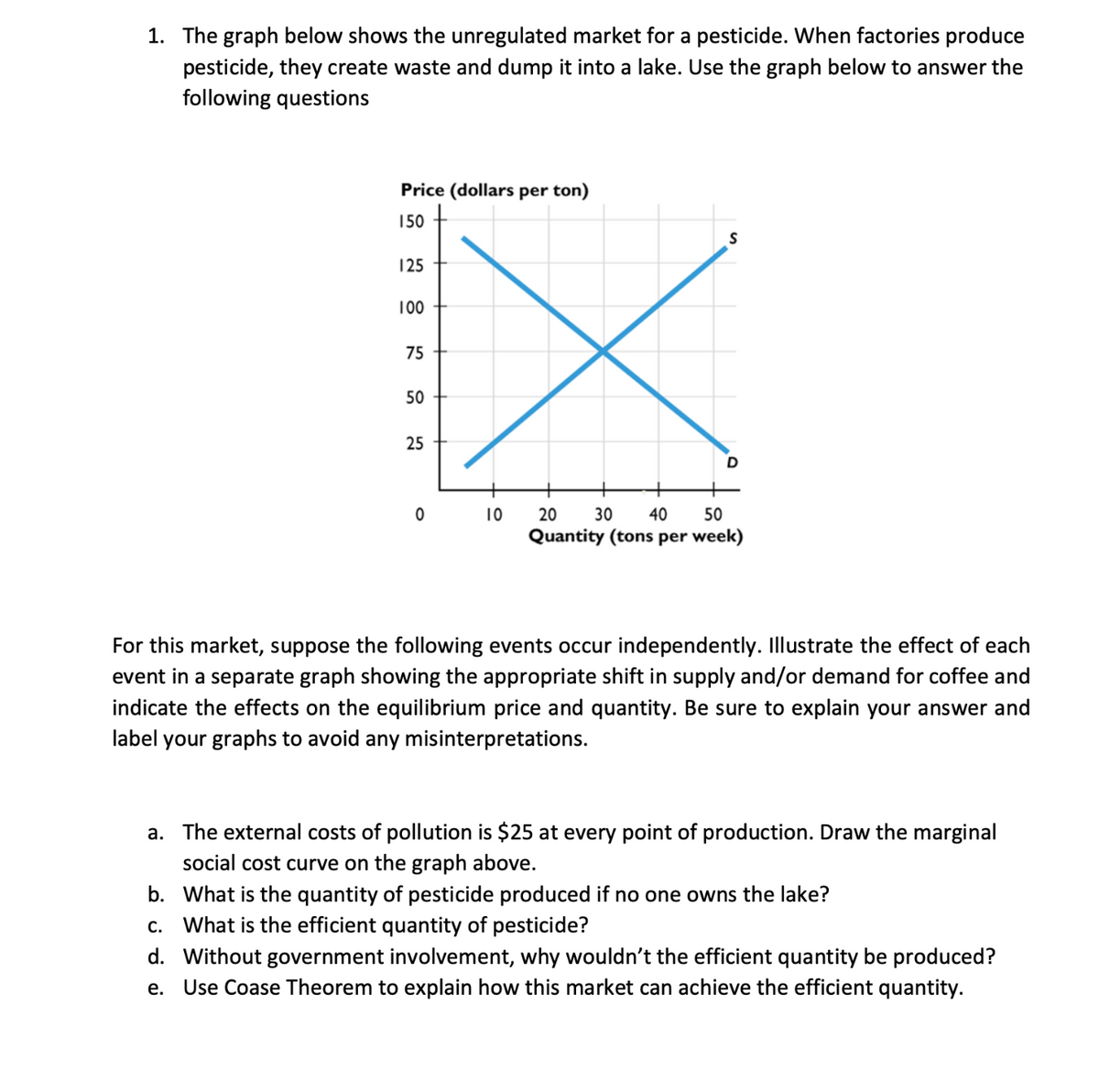

Transcribed Image Text:1. The graph below shows the unregulated market for a pesticide. When factories produce

pesticide, they create waste and dump it into a lake. Use the graph below to answer the

following questions

Price (dollars per ton)

150

125

100

75

50

25

25

S

50

30 40

Quantity (tons per week)

0 10

20

For this market, suppose the following events occur independently. Illustrate the effect of each

event in a separate graph showing the appropriate shift in supply and/or demand for coffee and

indicate the effects on the equilibrium price and quantity. Be sure to explain your answer and

label your graphs to avoid any misinterpretations.

a. The external costs of pollution is $25 at every point of production. Draw the marginal

social cost curve on the graph above.

b. What is the quantity of pesticide produced if no one owns the lake?

c. What is the efficient quantity of pesticide?

d. Without government involvement, why wouldn't the efficient quantity be produced?

e.

Use Coase Theorem to explain how this market can achieve the efficient quantity.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The following graph illustrates the weekly demand curve for motorized scooters in Roanoke. Use the green rectangle (triangle symbols) to compute total revenue at various prices along the demand curve. Note: You will not be graded on any changes made to this graph. PRICE (Dollars per scooter) 300 275 250 200 175 150 125 100 75 50 0 0 + 3 6 9 x 4 * B Demand 12 15 18 21 24 27 QUANTITY (Scooters) 30 33 36 39 Total Revenue ?arrow_forwardQuestion 1 Consider a rice farmer planting two (2) types of rice, white and brown rice, concurrently in his rice field using the same resources and technology and harvesting them at the same time. Given that consumers like to mix both white and brown rice in their daily consumption, explain the effect on the white rice market when the price of brown rice increases. Support your answers with suitable white rice market diagrams. Consider a farmer that produces both white and brown rice. It is discovered that the demand for brown rice is relatively more inelastic compared to the demand for white rice. Initially the price of both white and brown rice is the same and the farmer produces the same quantity of white and brown rice. Now there is an improvement in agricultural technologies that affect both white and brown rice equally. Employ the demand and supply model to compare and contrast the effects on the equilibrium price and quantity of both white and brown rice…arrow_forwardPlease help me with all the requirements. It's all one question. Thank you!arrow_forward

- This not a grade Question to go with picture: Label the new Equilibrium E1 What is the new equilibrium price? What is the new equilibrium quantity? Was the result of a change in supply or quantity supply? Was the change an increase or decrease? As a result, did the equilibrium price increase or decrease? As a result did the equilibrium quantity increase or decrease?arrow_forwardLast year, a man shared a video on TikTok of himself longboarding to work while drinking a bottle of OceanSpray juice. This resonated with the online community and kicked off a challenge to reproduce the scene using the same drink. Use the Four-Step method and draw a supply/demand graph to predict the effect on equilibrium price and quantity for OceanSpray. Clearly label your graph and upload it to the dropbox labeled (you may draw it on paper and take a picture, or use some other software).arrow_forwardThe market demand for productXis given by: \[ Q_{d}=6-1 / 2 P \text { or } P d=12-2 Q \] The market supply for goodXis given by: \[ Q_{s}=-14+2 P \text { or } P s=7+1 / 2 Q \] whereP=price per unit andQis number of units. Draw a supply-and-demand graph with these curves. 1.) Using the line drawing tool, draw the supply and demand curves. Properly label your lines. 2.) Using the point drawing tool, plot the equilibrium point. Label your point 'E'. Note: Carefully follow the instructions above and only draw the required objects. The equilibrium price is$and the equilibrium quantity is unit(s). (Enter your responses as integers.) A per-unit excise tax is imposed on suppliers of productX, and the market supply with the tax is now given by: \[ Q_{s}=-19+2 P \text { or } P s=9.50+1 / 2 Q \] Using the graph on the right, show this supply curve. 1.) Using the line drawing tool, draw the new supply curve. Label your line 'S1+tax'.1. Note: Carefully follow the instructions above and only draw…arrow_forward

- The blue curve on the following graph represents the demand curve facing a firm that can set its own prices. Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to this graph. Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly. # 345470 10 QUANTITY (Unita) *** TO QUANTITY (Number of units) Graph Input Tool Market for Goods Quantity Demanded (Lv) Demand Price (Dollars per unit) On the graph input tool, change the number found in the Quantity Demanded field to determine the prices that correspond to the production of 0, 2, 4, 5, 6, 8, and 10 units of output. Calculate the total revenue for each of these production levels. Then, on the following graph, use the green points (triangle symbo) to plot the results. Total Revenue QUANTITY() Ⓒ 50.00 Calculate the total revenue if the firm produces 2 versus 1 units. Then, calculate the marginal revenue of…arrow_forwardThis problem involves solving demand and supply equations together to determine price and quantity. a. Consider a demand curve of the form QD=-2P+20, where QD is the quantity demanded of a good and P is the price of the good. Graph this demand curve. Also draw a graph of the supply curve Qs =2P-4, where Qs is the quantity supplied. Be sure to put P on the vertical axis and Q on the horizontal axis. Assume that all the Qs and Ps are nonnegative for parts a, b, and c. At what values of P and Q do these curves intersect-that is, where does QD = Qs ? b. Now, suppose at each price that individuals demand four more units of output-that the demand curve shifts to QD - 2P+24. Graph this new demand curve. At what values of P and Q does the new demand curve intersect the old supply curve-that is, where does QD = Qs ? c. Now finally, suppose the supply curve shifts to Q's=2P-8. Graph this new supply curve. At what values of P and Q does QD=Q's? Show all working calculations and label garph with…arrow_forwardpls, solve this ques within 10-15 minutes with clear explanations and also explain why other options are wrong I'll give you multiple upvotes.arrow_forward

- Use the information/statement below to answer questions: 10. Because of exceptionally good weather conditions, this year's supply of-eucumber in Batinah is 20% greater than last year's supply. Assume that once cucumber is grown, the supply curve for cucumber is perfectly inelastic. Also assume that the demand curve for cucumber is the same this year as it was last year. If the price of cucumber is 25% lower this year than it was last year, what can we conclude? 10. The price elasticity of demand for cucumber is: a. -1.25 b. -1.00 © - 0.80 d. -0.25arrow_forward) Show graphically, in one graph, what would happen to the demand for bananas if it was recently discovered that they shortene colds, eliminated cancer, and could be used for clean burning fuel in a Volkswagen yellow convertible bug.arrow_forwardAssume that the graphs show a competitive market for the product stated in the question. Price aa 0 Price a a 0 2₁*Q₂ Quantity Graph A Graph A E₁ Q₁ Q₂ Quantity Graph C Graph B Graph C E₂ KE₁ Graph D D₁ S₁ U None of the above 52 Price 0 Price E₂ E₁ Q₂ Q₁ Quantity Graph B E2 KE₁ Q₂ Q₁ Quantity Graph D D₁ Select the graph above that best shows the change in the market specified in the following situation: In the market for ramen noodles (an inferior good), when consumers experience a substantial fall in income due to an economic recession. D₂ S₂ O 55arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education