ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

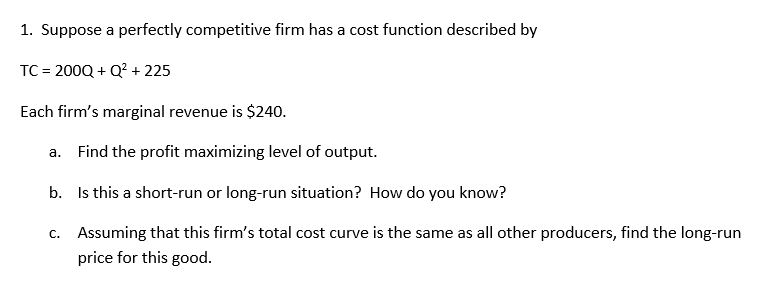

Transcribed Image Text:1. Suppose a perfectly competitive firm has a cost function described by

TC = 200Q+Q² +225

Each firm's marginal revenue is $240.

a. Find the profit maximizing level of output.

b.

Is this a short-run or long-run situation? How do you know?

c. Assuming that this firm's total cost curve is the same as all other producers, find the long-run

price for this good.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Which of the following offers the best explanation of why “marginal revenue equals marginal cost” is the rule that indicates the profit-maximizing output level? a. If output were reduced from the profit-maximizing level, then the firm would be gaining marginal revenue that exceeds marginal cost, and thus increasing the level of profit. b. The marginal revenue is equal to the marginal cost at all levels of output for a perfectly competitive firm. c. If output were increased from the profit-maximizing level, then the firm would be gaining marginal revenue that is less than the marginal cost incurred in producing this additional unit, and thus reducing the level of profit. d. Because the firm colludes with other similar firms to set price equal to marginal cost.arrow_forwardAt its current level of production a profit-maximizing firm in a competitive market receives $15 for each unit it produces, and faces an average cost of $10. At the market price of $15, the firm’s marginal cost curve crosses the marginal revenue curve at an output level of 1,000 units. A. Draw a diagram that depicts the typical firm in this market. B. What is the firm’s current profit? C. What changes are likely to occur in this market and why?arrow_forwardI need 11 and 12 please!!arrow_forward

- 2. Consider a market with 90 firms, each firm has a short-run total cost function as follows: TC(q) = 5q2, and a marginal cost function: MC(q) = 10q. Market demand is given by equation Qd(p) = 200 - p. a. Solve for the short-run equilibrium outcome: P*, Q* and q*. b. What is one firm's economic profit in this market? c. Consider a different market structure, where there is only one firm, interpreted as a monopolist, and then critically discuss the impact on equilibrium price and quantity. Discuss total surplus for these two types of market structures.arrow_forwardM10arrow_forwardwhy does price equal marginal revenue for the perfectly competitive firm? what is the relationship to the demand curve for the firm?arrow_forward

- 2. A firm sells its product in a perfectly competitive market where other firms charge a price of $80 per unit. The firm's total costs are CQ)=40+8Q+ 20%. a. How much output should the firm produce in the short run? b. What price should the firm charge in the short run? c. What are the firm's short-run profits? d. What adjustments should be anticipated in the long run?arrow_forwarda.Suppose a perfectly competitive firm can produce10000 bushels of corn a year at an output at which marginal revenue is equal to marginal cost. The market price of corn per bushel is $2. The firm's total costs per year are $30000 and fixed costs per year are $15000. Show and explain which of the following is true: In the short run, this firm should a) Produce 20000 bushels to try to increase economic profit. b) Produce 10000 bushels of corn because, although they are losing money, they are losing less than if they shut down. c)Shut down. d) Continue producing until the price of corn increases. b.A perfectly competitive firm, with MC=q operates in a market character,zed by the following market demand and supply conditions: Demand: Q=20000-100P Supply: Q=100P How much output does this competitive firm produce to maximize profit? Show your work graphically and algebraically.arrow_forward68. In a perfectly competitive market, industry demand is given by Q = 1000 – 20P. The typical firm’s average cost is TC = 300 + Q2 /3, and marginal cost by MC = (2/3)Q. What is the market price? A.$40 B. $32 C. $28.57 D. $30arrow_forward

- 1. If the average cost function of a firm producing a good in perfectly 40 competitive industry is AC = 2Q +9+, where Q is output level and the industry price is given to be P = $25. a) Derive the short-run supply curve for this firm b) Calculate the optimal level of production by this firm. c) Find the maximum profit of the firm. d) Should the firm produce in the short run or shut down? Justify.arrow_forwardQuestion 35 Suppose all firms in a perfectly competitive industry have marginal cost of producing q units is MC = 8 + 16q. The industry demand curve is given by P = 488 – Q. The price of the good is $200. What is this firm’s optimal short-run quantity and how many firms produce this good in the short run? 12 units and 12 firms 48 units and 24 firms 192 units and 24 firms 12 units and 24 firmsarrow_forward5. Suppose the market is perfectly competitive. The market equilibrium market price P = $20. A consumer's willingness to pay (WTP) is 30 - q. how much will this consumer buy and why? A firm's MC= 2q. What is the profit maximizing quantity this firm will produce? can you tell if this firm is making positive, negative, or zero economic profit?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education