ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

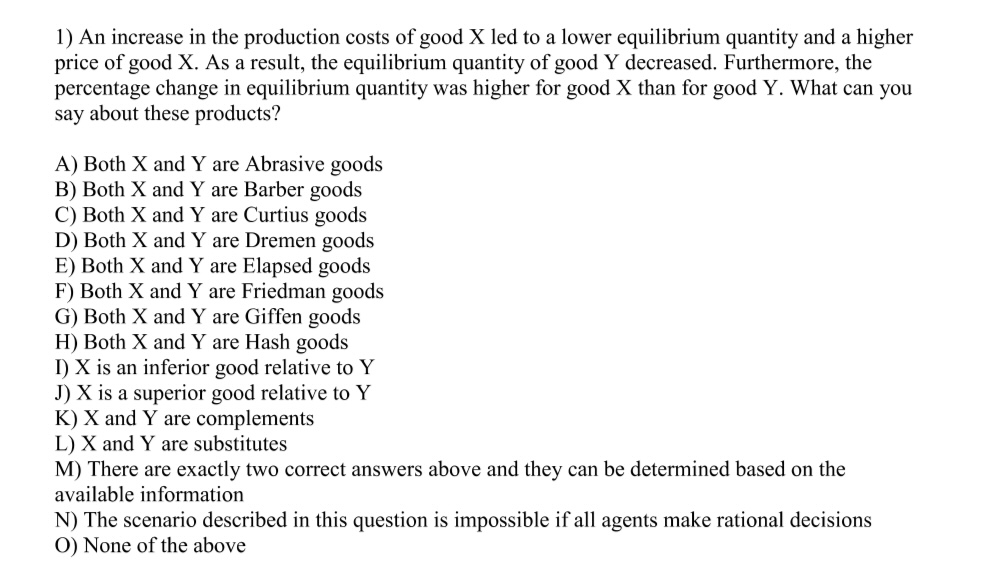

Transcribed Image Text:1) An increase in the production costs of good X led to a lower equilibrium quantity and a higher

price of good X. As a result, the equilibrium quantity of good Y decreased. Furthermore, the

percentage change in equilibrium quantity was higher for good X than for good Y. What can you

say about these products?

A) Both X and Y are Abrasive goods

B) Both X and Y are Barber goods

C) Both X and Y are Curtius goods

D) Both X and Y are Dremen goods

E) Both X and Y are Elapsed goods

F) Both X andY are Friedman goods

G) Both X and Y are Giffen goods

H) Both X and Y are Hash goods

I) X is an inferior good relative to Y

J) X is a superior good relative to Y

K) X and Y are complements

L) X and Y are substitutes

M) There are exactly two correct answers above and they can be determined based on the

available information

N) The scenario described in this question is impossible if all agents make rational decisions

O) None of the above

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- If the demand for a good increases when incomes rise and decreases when incomes fall, the good is called a normal good. See 3-2: Demand True Falsearrow_forwardIf an increase in income leads to an increase in the demand for sushi, then sushi is a normal good. a neutral good. a complement. a necessity.arrow_forwardConsider two markets: the market for waffles and the market for pancakes. The initial equilibrium for both markets is the same, the equilibrium price is $6.50, and the equilibrium quantity is 35.0. When the price is $9.75, the quantity supplied of waffles is 57.0 and the quantity supplied of pancakes is 101.0. For simplicity of analysis, the demand for both goods is the same. Using the midpoint formula, calculate the elasticity of supply for pancakes. Please round to two decimal places. Supply in the market for waffles isarrow_forward

- Now suppose that the good is an inferior good. Would the demand schedule still be valid for an inferior goodarrow_forwardDraw a graph to analyze the market for agricultural products (food). Label your price and quantity axes properly. In your graph, draw a supply curve for agricultural products (food) that obeys the law of supply. Label (S). In the same graph, draw a demand curve for food that obeys the law of demand. Label (D). Identify the market equilibrium point in your graph and label (E). Also, label the equilibrium price (PE) and the Equilibrium quantity (QE): 1. The federal government instituted acreage restriction programs in an attempt to eliminate the surpluses resulting from the price support program. Using the graph above, explain and illustrate how acreage restrictions, if effective might reduce or eliminate food surpluses. Label and explain clearly.arrow_forwardUse the graph to answer the question that follows. Price ($) P₂ Q₂ Q₁ Quantity ·D₂ An increase in income when good A is an inferior good Which of the following best explains the shift from D1 to D2 for Good A in this graph? An increase in the number of consumers in the market An increase in the price of a substitute good for good A A decrease in the number of producing firms An increase in the price of a key input, like oil. S₁ 1arrow_forward

- An increase in the price of good B caused an increase in the demand for good C. This indicates thatarrow_forwardAnswer question 2 pleasearrow_forwardIf the cross-price elasticity of demand for good X with respect to good Y equals 0, how is that value interpreted? These goods are complements, and the quantity demanded of good X increases if the price of good Y decreases. These goods are unrelated, and a change in the price of good Y has no effect on the quantity of good X demanded. These goods are normal goods, and a change in buyers income increases the quantity demanded of good X. These goods are substitutes, and the quantity demanded of good X decreases if the price of good Y decreases.arrow_forward

- What is the difference between substitutes and complements? Indicate two goods that are substitutes for each other. Indicate two goods that are complements.arrow_forwardThe nature of demand indicates that as the price of a good increases: suppliers wish to sell less of it. more of it is produced. more of it is desired. buyers desire to purchase less of it.arrow_forwardWhen an economist states the supply of a product has decreased, he or she has concluded that a) A smaller quantity will be produced at every price b) The price is too high for equilibrium c)a greater quanity will produced at every price d) the price is too low equilibrium. e) demand was too high for producers to make a profit.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education