FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

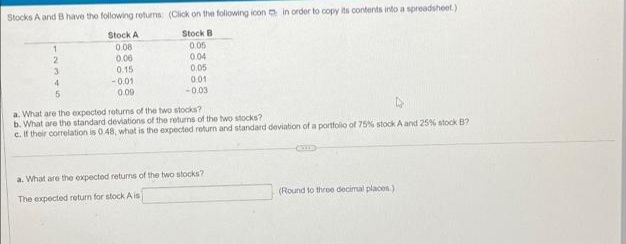

Transcribed Image Text:Stocks A and B have the following returns: (Click on the folowing icon a in order to copy its contents into a spreadsheet.)

Stock A

Stock B

0.08

0.06

0.15

0.05

0.04

0.05

0.01

-0.01

0.09

-0.03

a. What are the expected roturns of the two stocks?

b. What are the standard deviations of the returns of the two stocks?

c. If their correlation is 048, what is the expected return and standard deviation of a portfolio of 75% stock A and 25% stock B?

a. What are the expected returns of the two stocks?

The expected return for stock A is

(Round to three decimal places.)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- In the CAPM world, if Sharpe ratio of the market portfolio is 1.25 and the correlation coefficient between stock i and the market portfolio is 0.60, what is the stock i's Sharpe ratio? → (1) 0.25; (2) 0.45; (3) 0.50; (4) 0.75; (5) 0.80; (6) 1.00; (7) 1.25; 8 (8) 1.50; (9) 1.75; (10) 2.05;arrow_forward14. Risk free asset, the market, and stock X have the expected returns of 2%, 8%, and 12% respectively. If X and the market has a covariance of 0.1503, what is the risk level of the market (as it is measured by the standard deviation)?arrow_forwardVinayarrow_forward

- Consider the following probability distribution for stocks A and B: State Probability Return on Stock A Return on Stock B 1 0.10 10% 8% 2 0.20 13% 7% 3 0.20 12% 6% 4 0.30 14% 9% 5 0.20 15% 8% The coefficient of correlation between A and B is:arrow_forwardGiven the following probability distribution, what are the expected return and the standard deviation of returns for Security J? State Pi ri 1 0.5 11% 2 0.3 8% 3 0.2 5% O 9.40%; 2.04% O 8.90%; 2.34% O 7.40%; 2.94% O 8.40%; 2.64% O 7.90%; 1.74%arrow_forwardStock A and B have the following probability distributions of expected future returns: Probability A B 0.1 (20%) (46%) 0.2 7 0 0.4 15 15 0.2 23 30 0.1 47 50 What is the expected rate of return for Stock A? What is the standard deviation of returns for Stock B?arrow_forward

- The following expected return and the standard deviation of current returns are known: Security (i) Expected Return Standard Deviation βi A 0.20 0.12 1.1 B 0.12 0.10 0.8 T-Bills 0.05 0 0 Market Portfolio 0.20 0.15 1 Required: Determine which of A or B is over-valued or undervalued.arrow_forwardStock A has a correlation with the market of 0.53. Assuming that the standard deviation of returns for Stock A is 24.0% and that the standard deviation of returns for the market is 10.0%, what is beta for stock A? A 1.31 B. 1.27 C. 0.17 D. 0.22arrow_forwardPortfolio theory with two assets E(R1)=0.15 E(01)= 0.10 W1=0.5 E(R2)=0.20 E(02) = 0.20 W2=0.5 Calculate the expected return and the standard deviation of the two portfolios if r1,2 = 0.4 and -0.60 respectively.arrow_forward

- 2. The following table gives information on the return and variance of assets A and B, whose covariance is 0.0003: A B 0} 0,0009 0,0012 E (R₂) 0,05 0,06 a. Does the portfolio (1/3 of A and 2/3 of B) dominate the portfolio (2/3 of A and 1/3 of B)? b. Does the portfolio (1/2, 1/2) belong to the efficient frontier? c. If there were the possibility of lending and borrowing at 2%, would the portfolio (1/2, 1/2) belong to the new efficient frontier?arrow_forwardK -61 =1 2 N (Expected rate of return and risk) Syntex, Inc. is considering an investment in one of two common stocks. Given the information that follows, which investment is better, based on the risk (as measured by the standard deviation) and return? Probability 0.25 0.50 0.25 Common Stock A Probability 0.25 0.25 0.25 0.25 (Click on the icon in order to copy its contents into a spreadsheet.) @ 2 a. Given the information in the table, the expected rate of return for stock A is 16.25 %. (Round to two decimal places.) The standard deviation of stock A is %. (Round to two decimal places.) b. The expected rate of return for stock B is%. (Round to two decimal places.) The standard deviation for stock B is%. (Round to two decimal places.) c. Based on the risk (as measured by the standard deviation) and return of each stock, which investment is better? (Select the best choice below.) 30² F2 W OA. Stock A is better because it has a higher expected rate of return with less risk B. Stock B is…arrow_forwardConsider the following securities: state Probability A B A B H M L 0.2 0.5 0.3 с 6 10 6 3 7 12 2 5 14 1. The expected payoff of A is: 2. The standard deviation of A is: 3. If the price of A is 3, its expected return is: 4. The covariance between A and B is: 5. The correlation coefficient between A and B is: 6. Is it possible to build a portfolio that has zero variance using A and C? YES/ NOarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education