Concept explainers

Videos

Analyzing

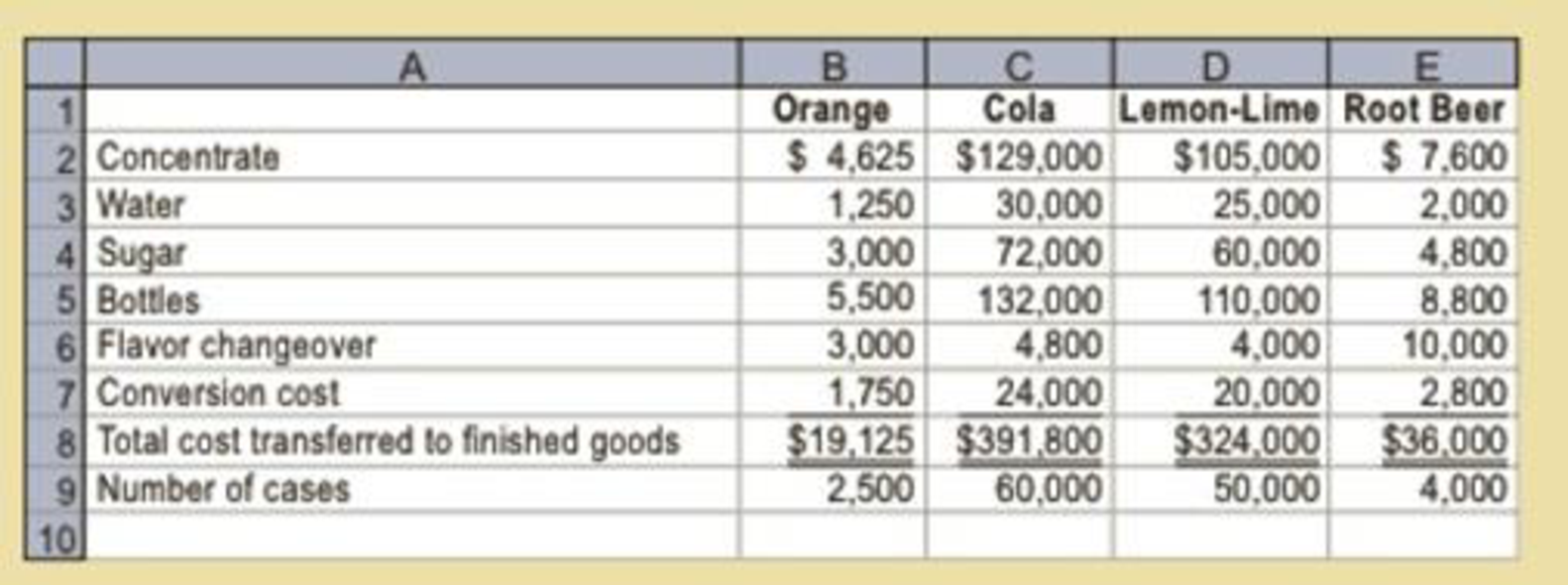

Mystic Bottling Company bottles popular beverages in the Bottling Department. The beverages are produced by blending concentrate with water and sugar. The concentrate is purchased from a concentrate producer. The concentrate producer sets higher prices for the more popular concentrate flavors. A simplified Bottling Department cost of production report separating the cost of bottling the four flavors follows:

Beginning and ending work in process inventories are negligible, so they are omitted from the cost of production report. The flavor changeover cost represents the cost of cleaning the bottling machines between production runs of different flavors. A production ran of a new flavor is produced after a flavor changeover from the previous flavor. Higher-demand flavors are produced in larger production runs, while smaller-demand flavors are produced in smaller production runs.

Prepare a memo to the production manager, analyzing this comparative cost information. In your memo, provide recommendations for further action, along with supporting schedules showing the total cost per case and cost per case by cost element. Round supporting calculations to the nearest cent.

Want to see the full answer?

Check out a sample textbook solution

Chapter 3 Solutions

Managerial Accounting

- Larsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forwardBenson Pharmaceuticals uses a process-costing system to compute the unit costs of the over-the-counter cold remedies that it produces. It has three departments: mixing, encapsulating, and bottling. In mixing, the ingredients for the cold capsules are measured, sifted, and blended (with materials assumed to be uniformly added throughout the process). The mix is transferred out in gallon containers. The encapsulating department takes the powdered mix and places it in capsules (which are necessarily added at the beginning of the process). One gallon of powdered mix converts into 1,500 capsules. After the capsules are filled and polished, they are transferred to bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label. Each bottle receives 50 capsules. During March, the following results are available for the first two departments: Overhead in both departments is applied as a percentage of direct labor costs. In the mixing department, overhead is 200% of direct labor. In the encapsulating department, the overhead rate is 150% of direct labor. Required: 1. Prepare a production report for the mixing department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to two decimal places for the unit cost.) 2. Prepare a production report for the encapsulating department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to four decimal places for the unit cost.) 3. CONCEPTUAL CONNECTION Explain why the weighted average method is easier to use than FIFO. Explain when weighted average will give about the same results as FIFO.arrow_forwardGood Scent, Inc., produces two colognes: Rose and Violet. Of the two, Rose is more popular. Data concerning the two products follow: The company uses a conventional costing system and assigns overhead costs to products using direct labor hours. Annual overhead costs follow. They are classified as fixed or variable with respect to direct labor hours. Required: 1. Using the conventional approach, compute the number of cases of Rose and the number of cases of Violet that must be sold for the company to break even. 2. Using an activity-based approach, compute the number of cases of each product that must be sold for the company to break even.arrow_forward

- Trail Outfitters has this information for its manufacturing: Its income statement under absorption costing is as follows: Prepare an income statement with variable costing and a reconciliation statement between both methods.arrow_forwardProcess activity analysis The Brite Beverage Company bottles soft drinks into aluminum cans. The manufacturing process consists of three activities: 1. Mixing: water, sugar, and beverage concentrate are mixed. 2. Filling: mixed beverage is filled into 12-oz. cans. 3. Packaging: properly filled cans are boxed into cardboard fridge packs. The activity costs associated with these activities for the period are as follows: The activity costs do not include materials costs, which are ignored for this analysis. Each can is expected to contain 12 ounces of beverage. Thus, after being filled, each can is automatically weighed. If a can is too light, it is rejected, or kicked, from the filling line prior to being packaged. The primary cause of kicks is heat expansion. With heat expansion, the beverage overflows during filling, resulting in underweight cans. This process begins by mixing and filling 6,300,000 cans during the period, of which only 6,000,000 cans are actually packaged. Three hundred thousand cans are rejected due to underweight kicks. A process improvement team has determined that cooling the cans prior to filling them will reduce the amount of overflows due to expansion. After this improvement, the number of kicks is expected to decline from 300,000 cans to 63,000 cans, thus increasing the number of filled cans to 6,237,000 [6,000,000 + (300,000 63,000)]. A. Determine the total activity cost per packaged can under present operations. B. Determine the amount of increased packaging activity costs from the expected improvements. C. Determine the expected total activity cost per packaged can after improvements. Round to three decimal places.arrow_forwardIn a manufacturing company, overhead allocations are made for three reasons: (1) to determine the full cost of a product; (2) to encourage efficient resource usage; and (3) to compare alternative courses of action for management purposes. 1. Why must overhead be considered a product cost under generally accepted accounting principles? 2. Ayam Company makes plastic dog carriers. The manufacturing process is highly automated and the machine time needed to make any size crate is approximately the same. Ayam’s management decides to begin producing plastic lawn furniture and, to do so, two additional pieces of automated equipment are acquired. Annual depreciation on the new pieces of equipment is P38,000. Should the new overhead cost be allocated over all products manufactured by Ayam? Explain.arrow_forward

- [The following information applies to the questions displayed below.] Victory Company uses weighted average process costing. The company has two production processes. Conversion cost is added evenly throughout each process. Direct materials are added at the beginning of the first process. Additional information for the first process follows. Beginning work in process inventory Units started this period Units completed and transferred out Ending work in process inventory. Beginning work in process inventory. Direct materials Conversion Costs added this period Direct materials Conversion Total costs to account for Cost per equivalent unit of production Units Total costs + Equivalent units of production (from part 1) Cost per equivalent unit of production 78,000 876,000 760,000 194,000 $ 496,080 87,640 3,319,920 1,665, 160 Direct Materials. Percent Complete 100% 100% 2. Compute cost per equivalent unit of production for both direct materials and conversion. Costs EUP $ 583,7: 4,985,0…arrow_forwardAssume that a company has recently switched to JIT manufacturing. Each manufacturing cell produces a single product or major subassembly. Cell workers have been trained to perform a variety of tasks. Additionally, many services have been decentralized. Costs are assigned to products using direct tracing, driver tracing, and allocation. For each cost listed, indicate the most likely product cost assignment method used before JIT and after JIT. Set up a table with three columns: Cost Item, Before JIT, and After JIT. You may assume that direct tracing is used whenever possible, followed by driver tracing, with allocation being the method of last resort. Inspection costs Power to heat, light, and cool plant Minor repairs on production equipment Salary of production supervisor (department/cell) Oil to lubricate machinery Salary of plant supervisor Costs to set up machinery Salaries of janitors Power to operate production equipment Taxes on plant and equipment Depreciation on production…arrow_forwardClassifying Costs The following is a list of costs incurred by several manufacturing companies. Classify each of the following costs as product cost or period cost. Indicate whether each product cost is a direct materials cost, a direct labor cost, or a factory overhead cost. Indicate whether each period cost is a selling expense or an administrative expense. Costs Classification a. Bonus for vice president of marketing b. Costs of operating a research laboratory c. Cost of unprocessed milk for a dairy d. Depreciation of factory equipment e. Entertainment expenses for sales representatives f. Factory supplies g. First-aid nurse for factory workers h. Health insurance premiums paid for factory workers i. Hourly wages of warehouse laborers j. Lumber used by furniture manufacturer k. Maintenance costs for factory equipment l. Microprocessors for a microcomputer manufacturer m. Packing supplies for products sold, which are…arrow_forward

- LogicCO is a fast-growing manufacturer of computer chips. Direct materials are added at the start of the production process. Conversion costs are added evenly during the process. Some units of this product are spoiled as a result of defects not detectable before inspection of finished goods. Spoiled units are disposed of at zero net disposal value. uses the FIFO method of process costing. Summary data and weighted-average data for are as follows: Requirements : 1. For each cost category, compute equivalent units. Show physical units in the first column. 2. Summarize total costs to account for; calculate cost per equivalent unit for each cost category; and assign costs to units completed and transferred out (including normal spoilage), to abnormal spoilage, and to units in ending work in process. 3. Should 's managers choose the weighted-average method or the FIFO method? Explain.arrow_forwardUse the following information for the Quick Study below. (Algo) [The following information applies to the questions displayed below.] Zia Company makes flowerpots from recycled plastic in two departments, Molding and Packaging. Zia uses the weighted average method, and units completed in the Molding department are transferred to the Packaging department. Production unit Information for the Molding department follows. Molding-Direct Materials Beginning work in process inventory Units started this period Ending work in process inventory Production cost information for the Molding department for the same period follows. Units Beginning work in process inventory (direct materials) Direct materials added this period 3,900 27,500 3,000 Req A Req B and C Percent Complete QS 16-18 (Algo) Weighted average: Computing equivalent units and cost per EUP (direct materials) LO P1arrow_forwardWeighted Average Method, Nonuniform Inputs, MultipleDepartmentsBenson Pharmaceuticals uses a process-costing system to compute the unit costs of the overthe-counter cold remedies that it produces. It has three departments: mixing, encapsulating,and bottling. In mixing, the ingredients for the cold capsules are measured, sifted, and blended(with materials assumed to be uniformly added throughout the process). The mix is transferredout in gallon containers. The encapsulating department takes the powdered mix and places it incapsules (which are necessarily added at the beginning of the process). One gallon of powderedmix converts into 1,500 capsules. After the capsules are filled and polished, they are transferredto bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label.Each bottle receives 50 capsules.During March, the following results are available for the first two departments: Overhead in both departments is applied as a percentage of…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College