Concept explainers

Videos

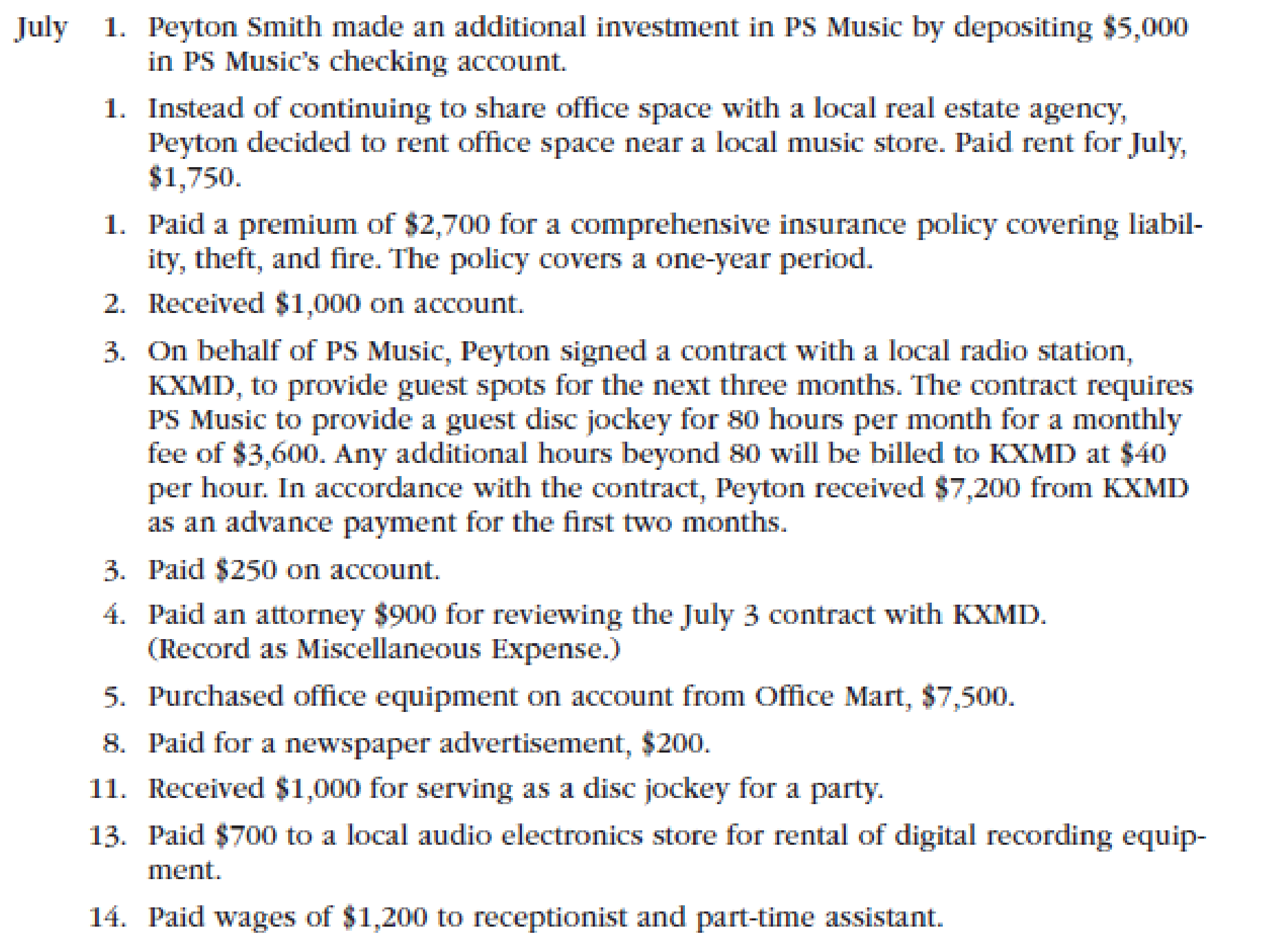

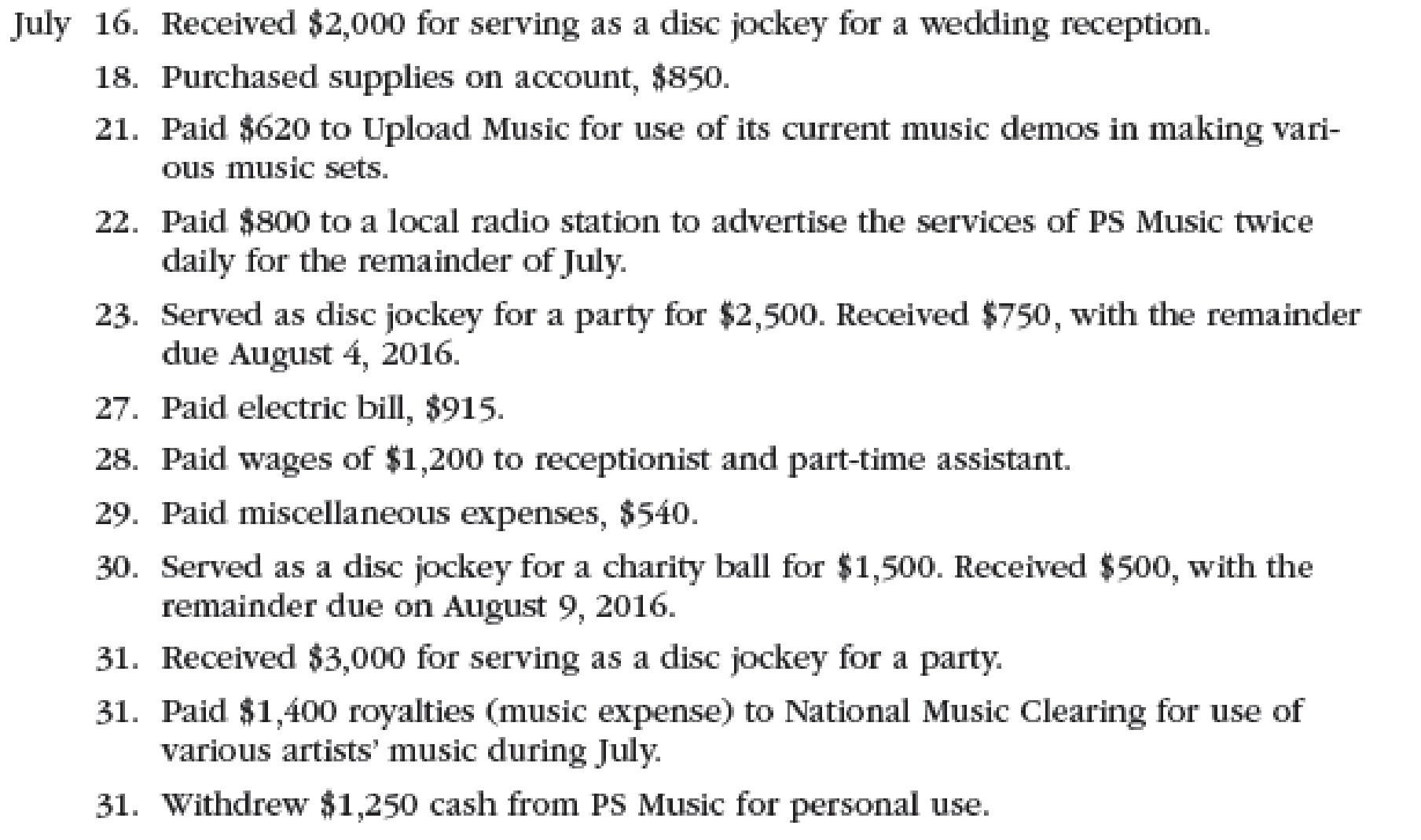

The transactions completed by PS Music during June 2016 were described at the end of Chapter 1. The following transactions were completed during July, the second month of the business’s operations:

Enter the following transactions on Page 2 of the two-column journal:

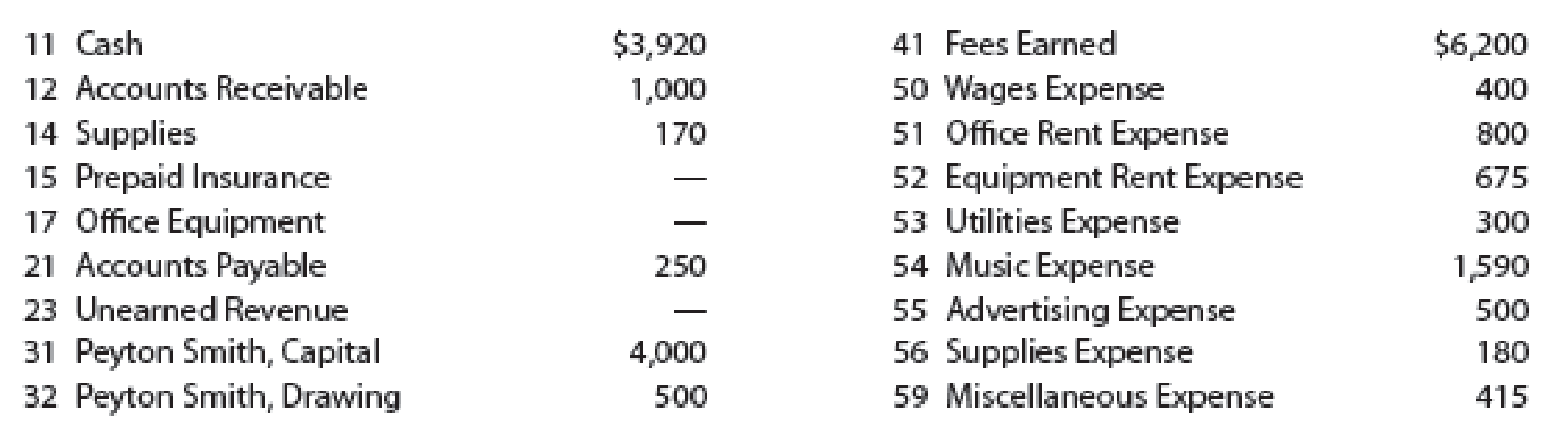

PS Music’s chart of accounts and the balance of accounts as of July 1, 2016 (all normal balances), are as follows:

Instructions

- 1. Enter the July 1, 2016, account balances in the appropriate balance column of a four-column account. Write Balance in the Item column, and place a check mark (✓) in the Posting Reference column. (Hint: Verify the equality of the debit and credit balances in the ledger before proceeding with the next instruction.)

- 2. Analyze and journalize each transaction in a two-column journal beginning on Page 1, omitting

journal entry explanations. - 3. Post the journal to the ledger, extending the account balance to the appropriate balance column after each posting.

- 4. Prepare an unadjusted

trial balance as of July 31, 2016.

(2) and (3)

Journalize the transactions of July in a two column journal beginning on page 18.

Explanation of Solution

Journal:

Journal is the book of original entry. Journal consists of the day today financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

Rules of debit and credit:

“An increase in an asset account, an increase in an expense account, a decrease in liability account, and a decrease in a revenue account should be debited.

Similarly, an increase in liability account, an increase in a revenue account and a decrease in an asset account, a decrease in an expenses account should be credited”.

Journalize the transactions of July in a two column journal beginning on page 18.

| Journal Page 1 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2016 | Cash | 11 | 5,000 | ||

| July | 1 | Person P’s Capital | 31 | 5,000 | |

| (To record the owner’s investment) | |||||

| 1 | Office Rent expense | 51 | 1,750 | ||

| Cash | 11 | 1,750 | |||

| (To record the payment of rent for the month of July) | |||||

| 1 | Prepaid insurance | 15 | 2,700 | ||

| Cash | 11 | 2,700 | |||

| (To record the payment of insurance premium) | |||||

| 2 | Cash | 11 | 1,000 | ||

| Accounts receivable | 12 | 1,000 | |||

| (To record the receipt of cash from customers) | |||||

| 3 | Cash | 11 | 7,200 | ||

| Unearned revenue | 23 | 7,200 | |||

| (To record the cash received for the service yet to be provide) | |||||

| 3 | Accounts payable | 21 | 250 | ||

| Cash | 11 | 250 | |||

| (To record the payment made to creditors on account) | |||||

| 4 | Miscellaneous expense | 59 | 900 | ||

| Cash | 11 | 900 | |||

| (To record the payment made for Miscellaneous expense) | |||||

| 5 | Office equipment | 17 | 7,500 | ||

| Accounts payable | 21 | 7,500 | |||

| (To record the purchase of equipment on account) | |||||

| 8 | Advertising expense | 55 | 200 | ||

| Cash | 11 | 200 | |||

| (To record the payment of advertising expense) | |||||

| 11 | Cash | 11 | 1,000 | ||

| Fees earned | 41 | 1,000 | |||

| (To record the receipt of cash) | |||||

| 13 | Equipment rent expense | 52 | 700 | ||

| Cash | 11 | 700 | |||

| (To record the payment made to equipment) | |||||

| 14 | Wages expense | 50 | 1,200 | ||

| Cash | 11 | 1,200 | |||

| (To record the payment of wages) | |||||

Table (1)

| Journal Page 2 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2016 | 16 | Cash | 11 | 2,000 | |

| July | Fees earned | 41 | 2,000 | ||

| (To record the receipt of cash) | |||||

| 18 | Supplies | 14 | 850 | ||

| Accounts payable | 21 | 850 | |||

| (To record the purchase of supplies) | |||||

| 21 | Music expense | 54 | 620 | ||

| Cash | 11 | 620 | |||

| (To record the payment incurred for music) | |||||

| 22 | Advertising expense | 55 | 800 | ||

| Cash | 11 | 800 | |||

| (To record the payment of advertising expense) | |||||

| 23 | Cash | 11 | 750 | ||

| Accounts receivable | 12 | 1,750 | |||

| Fees earned | 41 | 2,500 | |||

| (To record the receipt of cash for the service performed party for cash and party on account) | |||||

| 27 | Utilities expense | 53 | 915 | ||

| Cash | 11 | 915 | |||

| (To record the payment of electricity) | |||||

| 28 | Wages expense | 50 | 1,200 | ||

| Cash | 11 | 1,200 | |||

| (To record the payment made for salary and commission expense) | |||||

| 29 | Miscellaneous expense | 59 | 540 | ||

| Cash | 11 | 540 | |||

| (To record the revenue earned and billed) | |||||

| 30 | Cash | 11 | 500 | ||

| Accounts receivable | 12 | 1,000 | |||

| Fees earned | 41 | 1,500 | |||

| (To record the purchase of land party for cash and party on signing a note) | |||||

| 31 | Cash | 11 | 3,000 | ||

| Fees earned | 41 | 3,000 | |||

| (To record the receipt of cash) | |||||

| 31 | Music expense | 54 | 1,400 | ||

| Cash | 11 | 1,400 | |||

| (To record the payment incurred for music) | |||||

| 31 | Person P’s Drawing | 32 | 1,250 | ||

| Cash | 11 | 1,250 | |||

| (To record the withdrawal of cash for personal use) | |||||

Table (2)

(1) and (3)

Record the balance of each account in the appropriate balance column of a four-column account and post them to the ledger.

Explanation of Solution

T-account: An account is referred to as a T-account, because the alignment of the components of the account resembles the capital letter ‘T’. An account consists of the three main components which are as follows:

- The title of the account.

- The left or debit side.

- The right or credit side.

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 3,920 | |||

| 1 | 1 | 5,000 | 8,920 | ||||

| 1 | 1 | 1,750 | 7,170 | ||||

| 1 | 1 | 2,700 | 4,470 | ||||

| 2 | 1 | 1,000 | 5,470 | ||||

| 3 | 1 | 7,200 | 12,670 | ||||

| 3 | 1 | 250 | 12,420 | ||||

| 4 | 1 | 900 | 11,520 | ||||

| 8 | 1 | 200 | 11,320 | ||||

| 11 | 1 | 1,000 | 12,320 | ||||

| 13 | 1 | 700 | 11,620 | ||||

| 14 | 1 | 1,200 | 10,420 | ||||

| 16 | 2 | 2,000 | 12,420 | ||||

| 21 | 2 | 620 | 11,800 | ||||

| 22 | 2 | 800 | 11,000 | ||||

| 23 | 2 | 750 | 11,750 | ||||

| 27 | 2 | 915 | 10,835 | ||||

| 28 | 2 | 1,200 | 9,635 | ||||

| 29 | 2 | 540 | 9,095 | ||||

| 30 | 2 | 500 | 9,595 | ||||

| 31 | 2 | 3,000 | 12,595 | ||||

| 31 | 2 | 1,400 | 11,195 | ||||

| 31 | 2 | 1,250 | 9,945 | ||||

Table (3)

| Account: Accounts Receivable Account no. 12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 1,000 | |||

| 2 | 1 | 1,000 | – | – | |||

| 23 | 2 | 1,750 | 1,750 | ||||

| 30 | 2 | 1,000 | 2,750 | ||||

Table (4)

| Account: Supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 170 | |||

| 18 | 2 | 850 | 1,020 | ||||

Table (5)

| Account: Prepaid Insurance Account no. 15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | 1 | 2,700 | 2,700 | |||

Table (6)

| Account: Office equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 5 | 1 | 7,500 | 7,500 | |||

Table (7)

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 250 | |||

| 3 | 1 | 250 | – | – | |||

| 5 | 1 | 7,500 | 7,500 | ||||

| 18 | 2 | 850 | 8,350 | ||||

Table (8)

| Account: Unearned Revenue Account no. 23 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 3 | 1 | 7,200 | 7,200 | |||

Table (9)

| Account: Person P’s Capital Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 4000 | |||

| 1 | 1 | 5,000 | 9,000 | ||||

Table (10)

| Account: Person P’s Drawing Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 500 | |||

| 31 | 2 | 1,250 | 1,750 | ||||

Table (11)

| Account: Fees earned Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 6,200 | |||

| 11 | 1 | 1,000 | 7,200 | ||||

| 16 | 2 | 2,000 | 9,200 | ||||

| 23 | 2 | 2,500 | 11,700 | ||||

| 30 | 2 | 1,500 | 13,200 | ||||

| 31 | 2 | 3,000 | 16,200 | ||||

Table (12)

| Account: Wages expense Account no. 50 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 400 | |||

| 14 | 1 | 1,200 | 1,600 | ||||

| 28 | 2 | 1,200 | 2,800 | ||||

Table (13)

| Account: Office rent expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 800 | |||

| 1 | 1 | 1,750 | 2,550 | ||||

Table (14)

| Account: Equipment rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 675 | |||

| 13 | 1 | 700 | 1,375 | ||||

Table (15)

| Account: Utility expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 300 | |||

| 27 | 2 | 915 | 1,215 | ||||

Table (16)

| Account: Music expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 1,590 | |||

| 21 | 2 | 620 | 2,210 | ||||

| 31 | 2 | 1,400 | 3,610 | ||||

Table (17)

| Account: Advertising expense Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 500 | |||

| 8 | 1 | 200 | 700 | ||||

| 22 | 2 | 800 | 1,500 | ||||

Table (18)

| Account: Supplies expense Account no. 56 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 180 | |||

Table (19)

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| July | 1 | Balance | ✓ | 415 | |||

| 4 | 1 | 900 | 1,315 | ||||

| 29 | 2 | 540 | 1,855 | ||||

Table (20)

(4)

Prepare an unadjusted trial balance of Company PS Music at July 31, 2016.

Explanation of Solution

Unadjusted trial balance: The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Prepare an unadjusted trial balance of Company PS Music at July 31, 2016 as follows:

|

PS Music Unadjusted Trial Balance July 31, 2016 | |||

| Particulars |

Account No. | Debit $ | Credit $ |

| Cash | 11 | 9,945 | |

| Accounts receivable | 12 | 2,750 | |

| Supplies | 14 | 1,020 | |

| Prepaid insurance | 15 | 2,700 | |

| Office Equipment | 17 | 7,500 | |

| Accounts payable | 21 | 8,350 | |

| Unearned revenue | 23 | 7,200 | |

| P’s Capital | 31 | 9,000 | |

| P’s Drawings | 32 | 1,750 | |

| Fees earned | 41 | 16,200 | |

| Wages expense | 50 | 2,800 | |

| Office Rent expense | 51 | 2,550 | |

| Equipment Rent expense | 52 | 1,375 | |

| Utilities expense | 53 | 1,215 | |

| Music expense | 54 | 3,610 | |

| Advertising expense | 55 | 1,500 | |

| Supplies expense | 56 | 180 | |

| Miscellaneous expense | 59 | 1,855 | |

| Total | 40,750 | 40,750 | |

Table (21)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $40,750.

Want to see more full solutions like this?

Chapter 2 Solutions

Financial Accounting

- Piedmont Inc. has the following transactions for its first month of business: A. What are the individual account balances, and the total balance, in the accounts payable subsidiary ledger? B. What is the balance in the Accounts Payable general ledger account?arrow_forwardMaddie Inc. has the following transactions for its first month of business. A. What are the individual account balances, and the total balance, in the accounts receivable subsidiary ledger? B. What is the balance in the accounts receivable general ledger (control) account?arrow_forwardThe transactions completed by AM Express Company during March, the first month of the fiscal year, were as follows: Instructions 1. Enter the following account balances in the general ledger as of March 1: 2. Journalize the transactions for March, using the following journals similar to those illustrated in this chapter: single-column revenue journal (p. 35), cash receipts journal (p. 31), purchases journal (p. 37, with columns for Accounts Payable, Maintenance Supplies, Office Supplies, and Other Accounts), cash payments journal (p. 34), and twocolumn general journal (p. 1). Assume that the daily postings to the individual accounts in the accounts payable subsidiary ledger and the accounts receivable subsidiary ledger have been made. 3. Post the appropriate individual entries to the general ledger. 4. Total each of the columns of the special journals and post the appropriate totals to the general ledger; insert the account balances. 5. Prepare a trial balance.arrow_forward

- The transactions completed by Revere Courier Company during December 2016, the first month of the fiscal year, were as follows: Instructions 1. Enter the following account balances in the general ledger as of December 1: 2. Journalize the transactions for December 2016, using the following journals similar to those illustrated in this chapter: cash receipts journal (p. 31), purchases journal (p. 37, with columns for Accounts Payable, Maintenance Supplies, Office Supplies, and Other Accounts), single-column revenue journal (p. 35), cash payments journal (p. 34), and two-column general journal (p. 1). Assume that the daily postings to the individual accounts in the accounts payable subsidiary ledger and the accounts receivable subsidiary ledger have been made. 3. Post the appropriate individual entries to the general ledger. 4. Total each of the columns of the special journals, and post the appropriate totals to the general ledger; insert the account balances. 5. Prepare a trial balance.arrow_forwardThe following account balances were included in Bromley Companγs balance sheet on December 31, 2018: Prepare journal entries to record all the preceding events. Unless otherwise indicated, assume the company makes all payment's in cash.arrow_forwardYou must complete the following tasks below for the month of April in the Excel workbook provided. Required: Part 1. Prepare a journal entry to record each transaction. You must provide a short explanation for each transaction. Part 2. Setup appropriate T-accounts. All accounts begin with 0 balances. Part 3. Record in the T-accounts the effects of each transaction for Sydney Stables in April, referencing each transaction in the accounts with the transaction letter. Show the ending balances in the T-accounts. Part 4. Prepare a trial balance. Part 5. Prepare a statement of earnings, a statement of shareholders’ equity and a statement of financial position for the month ended April 30, 2020.arrow_forward

- Global Services Company had the following transactions during the month of August: a. Record the August revenue transactions for Global Services Company into the following revenue journal format: b. What is the total amount posted to the accounts receivable and fees earned accounts from the revenue journal for August? c. What is the August 31 balance of the Morgan Corp. customer account assuming a zero balance on August 1?arrow_forwardSage Learning Centers was established on July 20, 2016, to provide educational services. The services provided during the remainder of the month are as follows: Instructions 1. Journalize the transactions for July, using a single-column revenue journal and a two-column general journal. Post to the following customer accounts in the accounts receivable ledger, and insert the balance immediately after recording each entry: D. Chase; J. Dunlop; F. Mintz; T. Quinn; K. Tisdale. 2. Post the revenue journal and the general journal to the following accounts in the general ledger, inserting the account balances only after the last postings: 3. a. What is the sum of the balances of the customer accounts in the subsidiary ledger at July 31? b. What is the balance of the accounts receivable controlling account at July 31? 4. Assume Sage Learning Centers began using a computerized accounting system to record the sales transactions on August 1. What are some of the benefits of the computerized system over the manual system?arrow_forwardThe following selected accounts and their current balances appear in the ledger of Kanpur Co. for the fiscal year ended June 30, 2019: 1. Prepare a multiple-step income statement.2. Prepare a statement of owner’s equity.3. Prepare a balance sheet, assuming that the current portion of the note payable is$7,000.4. Briefly explain how multiple-step and single-step income statements differ.arrow_forward

- 2. Journalize the entries to record the transactions, and post to the eight selected accounts. Assume that the closing entry for revenues and expenses has been made and post net income of $1,196,500 to the retained earnings account. Refer to the Chart of Accounts for exact wording of account titles. When required, round your answers to the nearest dollar. PAGE 10 JOURNAL ACCOUNTING EQUATION DATE DESCRIPTION POST. REF. DEBIT CREDIT ASSETS LIABILITIES EQUITY 1 2 3 4 5 6 7 8 9 10 11 12 13 14…arrow_forwardHi pls Journalize the transaction And set up T accounts and post beginning account balances and transactions. Pls also Journalize and post closing entries and Prepare a trial balance for the month ending and Prepare an income statement for the month ending (ignore taxes) and Prepare a statement of retained earning and Prepare an ending balance sheet Problem: The beginning balances in ledger of DBM Corporation for September 01, 2018 were as follows; Account Debit Credit Accounts Payable 2,160 Accounts Receivable 3,070 Paid in capital- common stock 4,990 Cash 3,910 Notes Payable 600 Property, plant, and equipment (at cost) 6,200 Allowances for doubtful accounts 540 Inventories 1,730 Accumulated depreciation 2,800 Prepaid Expenses 1,250 Retained earnings 2,250 Good will 1,000 Estimated tax liability 750 Marketable securities 1,750 Accrued Expense 1,000 Patents and trademarks 500 Bonds payable 2,000 Investment…arrow_forwardWhich one of the following statements is true concerning the company’s accounts receivable as of December 31? see the attached screenshot for optionsarrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College