Concept explainers

Videos

San Mateo Optics, Inc., specializes in manufacturing lenses for large telescopes and cameras used in space exploration. As the specifications for the lenses are determined by the customer and vary considerably, the company uses a job-order costing system.

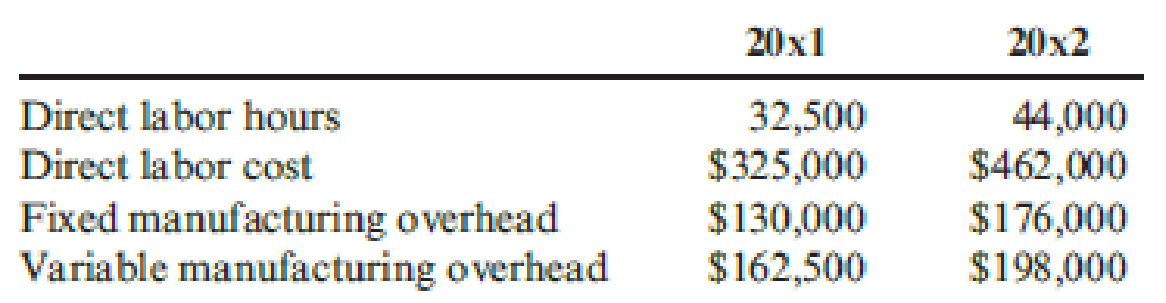

Manufacturing overhead is applied to jobs on the basis of direct labor hours, utilizing the absorption- or full-costing method. San Mateo’s predetermined overhead rates for 20x1 and 20x2 were based on the following estimates.

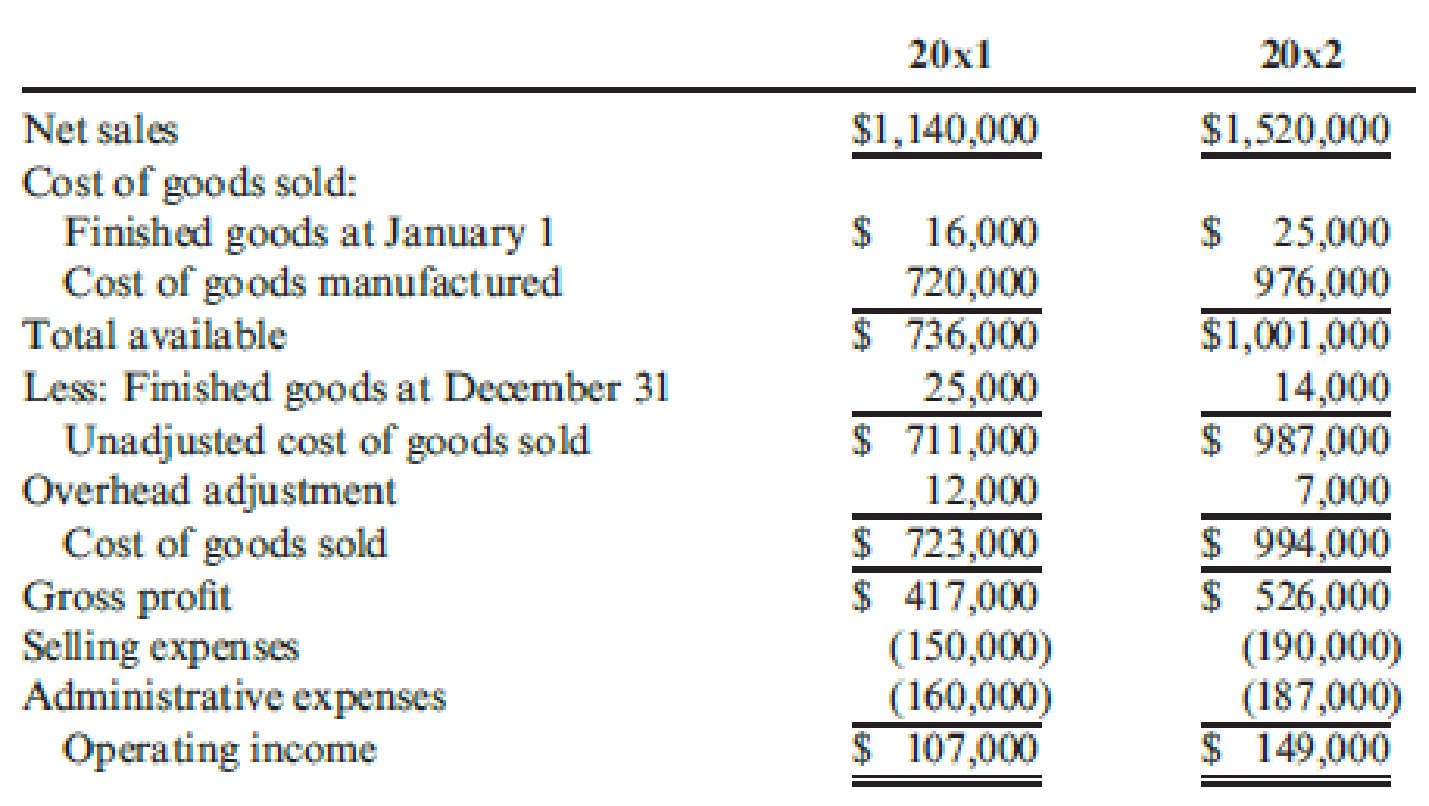

Jim Cimino, San Mateo’s controller, would like to use variable (direct) costing for internal reporting purposes as he believes statements prepared using variable costing are more appropriate for making product decisions. In order to explain the benefits of variable costing to the other members of San Mateo’s management team, Cimino plans to convert the company’s income statement from absorption costing to variable costing. He has gathered the following information for this purpose, along with a copy of San Mateo’s 20x1 and 20x2 comparative income statement.

San Mateo Optics, Inc. Comparative Income Statement For the Years 20x1 and 20x2

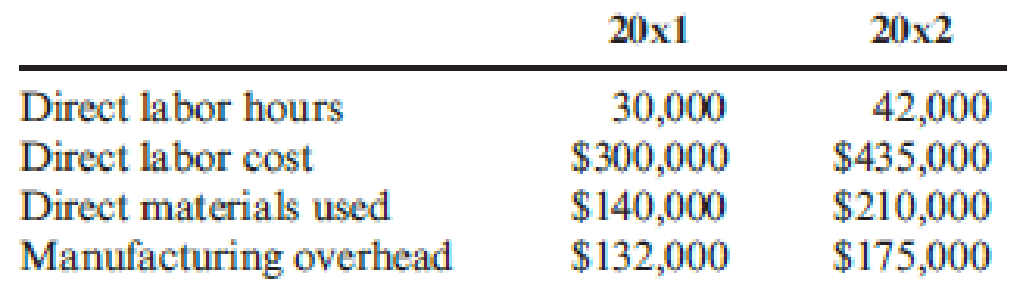

San Mateo’s actual manufacturing data for the two years are as follows:

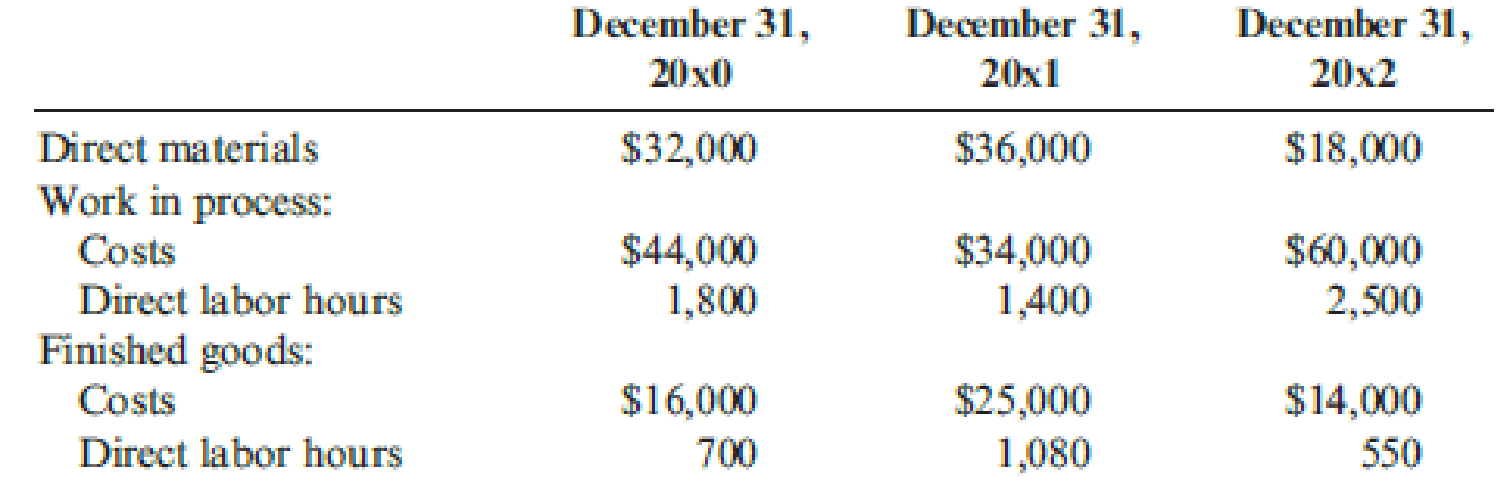

The company’s actual inventory balances were as follows:

For both years, all administrative expenses were fixed, while a portion of the selling expenses resulting from an 8 percent commission on net sales was variable. San Mateo reports any over-or underapplied overhead as an adjustment to the cost of goods sold.

Required:

- 1. For the year ended December 31, 20x2, prepare the revised income statement for San Mateo Optics, Inc., utilizing the variable-costing method. Be sure to include the contribution margin on the revised income statement.

- 2. Describe two advantages of using variable costing rather than absorption costing. (CMA adapted)

Trending nowThis is a popular solution!

Chapter 18 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Geneva, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountants before making any allocations: The total cost of purchasing and receiving parts used in manufacturing is 60,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were 48,000 and 12,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?arrow_forwardBrees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for 66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows: Prior to making a decision, the companys CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following: 3 setups1,160 each (The setups would be avoided, and total spending could be reduced by 1,160 per setup.) One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is 12,300 and could be totally avoided if the part were purchased. Engineering work: 470 hours, 45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.) 75 fewer material moves at 30 per move. Required: 1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier. 2. Now, using the special study data, repeat the analysis. 3. Discuss the qualitative factors that would affect the decision, including strategic implications. 4. After reviewing the special study, the controller made the following remark: This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs? Is the controller right?arrow_forwardHigh Desert Potteryworks makes a variety of pottery products that it sells to retailers such as Home Depot. The company uses a job-order costing system in which predetermined overhead rates are used to apply manufacturing overhead cost to jobs. The predetermined overhead rate in the Molding Department is based on machine-hours, and the rate in the Painting Department is based on direct labor-hours. At the beginning of the year, the company's management made the following estimates: Department Molding Painting Direct labor-hours 39,500 51,200 Machine-hours 87,000 33,000 Direct materials cost $186,000 $196,000 Direct labor cost $277,000 $513,000 Fixed manufacturing overhead cost $243,600 $465,920 Variable manufacturing overhead per machine-hour $2.60 - Variable manufacturing overhead per direct labor-hour - $4.60 Job 205 was started on August 1 and completed on August 10.…arrow_forward

- Garza Corporation has two production departments, Casting and Customizing. The company uses a job-order costing system and computes a predetermined overhead rate in each production department. The Casting Department's predetermined overhead rate is based on machine-hours and the Customizing Department's predetermined overhead rate is based on direct labor-hours. At the beginning of the current year, the company had made the following estimates: Machine-hours Direct labor-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour The estimated total manufacturing overhead for the Customizing Department is closest to: Casting 13,000 19,000 $ 62,400 $ 1.20 Customizing 16,000 4,000 $ 16,400 4.50arrow_forwardCollini Corporation has two production departments, Machining and Customizing. The company uses a job-order costing system and computes a predetermined overhead rate in each production department. The Machining Department’s predetermined overhead rate is based on machine-hours and the Customizing Department’s predetermined overhead rate is based on direct labor-hours. At the beginning of the current year, the company had made the following estimates: Machining Customizing Machine-hours 17,000 15,000 Direct labor-hours 3,000 6,000 Total fixed manufacturing overhead cost $ 102,000 $ 61,200 Variable manufacturing overhead per machine-hour $ 1.70 Variable manufacturing overhead per direct labor-hour $ 4.10 During the current month the company started and finished Job T268. The following data were recorded for this job: Job T268: Machining Customizing Machine-hours 80 30 Direct labor-hours 30 50 Direct materials $ 720 $ 380 Direct labor cost $ 900…arrow_forwardBulla Corporation has two production departments, Machining and Customizing. The company uses a job-order costing system and computes a predetermined overhead rate in each production department. The Machining Department’s predetermined overhead rate is based on machine-hours and the Customizing Department’s predetermined overhead rate is based on direct labor-hours. At the beginning of the current year, the company had made the following estimates: Machining Customizing Machine-hours 18,000 20,000 Direct labor-hours 1,000 2,000 Total fixed manufacturing overhead cost $ 90,000 $ 88,000 Variable manufacturing overhead per machine-hour $ 2.00 Variable manufacturing overhead per direct labor-hour $ 4.00 During the current month the company started and finished Job K369. The following data were recorded for this job: Job K369: Machining Customizing Machine-hours 70 40 Direct labor-hours 40 60 Required: Calculate the total amount of overhead…arrow_forward

- Bulla Corporation has two production departments, Machining and Customizing. The company uses a job-order costing system and computes a predetermined overhead rate in each production department. The Machining Department’s predetermined overhead rate is based on machine-hours and the Customizing Department’s predetermined overhead rate is based on direct labor-hours. At the beginning of the current year, the company had made the following estimates: Machining Customizing Machine-hours 30,000 10,000 Direct labor-hours 3,000 10,000 Total fixed manufacturing overhead cost $ 141,000 $ 47,000 Variable manufacturing overhead per machine-hour $ 2.50 Variable manufacturing overhead per direct labor-hour $ 5.00 During the current month the company started and finished Job K369. The following data were recorded for this job: Job K369: Machining Customizing Machine-hours 50 20 Direct labor-hours 30 50 Required: Calculate the total amount of overhead…arrow_forwardMahon Corporation has two production departments, Casting and Customizing. The company uses a job-order costing system and computes a predetermined overhead rate in each production department. The Casting Department's predetermined overhead rate is based on machine-hours and the Customizing Department's predetermined overhead rate is based on direct labor-hours. At the beginning of the current year, the company had made the following estimates: Machine-hours Direct labor-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Job T138: Machine-hours Direct labor-hours Casting During the current month the company started and finished Job T138. The following data were recorded for this job: Casting Customizing 80 50 9 100 17, 200 5,600 $111,800 $ 1.80 Customizing 13,200 6,600 $67,320 $ 3.50 The amount of overhead applied in the Customizing Department to Job T138 is closest to: (Round your…arrow_forwardMahon Corporation has two production departments, Casting and Customizing. The company uses a job-order costing system and computes a predetermined overhead rate in each production department. The Casting Department's predetermined overhead rate is based on machine-hours and the Customizing Department's predetermined overhead rate is based on direct labor-hours. At the beginning of the current year, the company had made the following estimates: Machine-hours Direct labor-hours Total fixed manufacturing overhead cost Job T138: Machine-hours. Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour During the current month the company started and finished Job T138. The following data were recorded for this job: Customizing 50 80 Direct labor-hours The amount of overhead applied in the Customizing Department to Job T138 is closest to: Note: Round your intermediate calculations to 2 decimal places. Multiple Choice Casting 60 12 $770.00 Casting…arrow_forward

- White Company has two departments, Cutting and Finishing. The company uses job-order costing and computes a predetermined overhead rate in each department. The Cutting Department bases its rate on machine-hours, and the Finishing Department bases its rate on direct labor-hours. At the beginning of the year, the company made the following estimates: Direct labor-hours Machine-hours Direct materials Direct labor cost Direct labor-hours Machine-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per machine-hour Variable manufacturing overhead per direct labor-hour Required: 1. Compute the predetermined overhead rate for each department. 2. The Job cost sheet for Job 203, which was started and completed during the year, showed the following: Department Cutting 4 87 $ 730 $ 84 Finishing 15 6 Predetermined overhead rate Required 3 $ 370 $ 315 Required 1 Required 2 Compute the predetermined overhead rate for each department. Note: Round your answers to 2 decimal…arrow_forwardJannsen Industries manufactures parts for aircraft engines. It uses a job-order costing system with a single plantwide predetermined overhead rate based on direct labor-hours. The company based its predetermined overhead rate for the current year on the following data: Total direct labor-hours Total fixed manufacturing overhead cost Variable manufacturing overhead per direct labor-hour Recently, Jannsen completed job F2232 for one of their customers in Taiwan. Here is some information about the job: Number of units in the job Total direct labor-hours Direct materials Direct labor cost 105,000 $399,000 $ 2.00 50 100 $ 730 $10,500 The unit product cost for Job F2232 is closest to: (Round your intermediate calculations to 2 decimal places.)arrow_forwardGarza Corporation has two production departments, Casting and Customizing. The company uses a job-order costing system and computes a predetermined overhead rate in each production department. The Casting Department's predetermined overhead rate is based on machine-hours and the Customizing Department's predetermined overhead rate is based on direct labor-hours. At the beginning of the current year, the company had made the following estimates: Casting Customizing Machine-hours 20,000 13,000 Direct labor-hours 1,000 7,000 Total fixed manufacturing overhead cost $ 152,000 $ 68,600 Variable manufacturing overhead per machine-hour $ 2.10 Variable manufacturing overhead per direct labor-hour $ 4.30 The predetermined overhead rate for the Casting Department is closest to: $9.70 per machine-hour $7.60 per machine-hour $27.71 per machine-hour $2.10 per machine-hourarrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning