Videos

a.

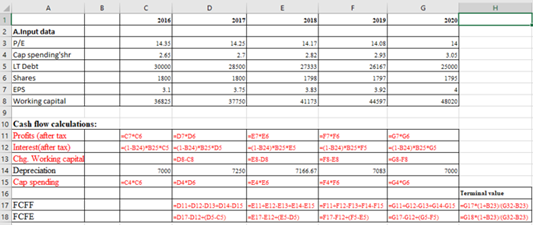

To calculate:The intrinsic value when GE’s P/E ratio starting in 2020 will be 16.

Introduction:

Unlevered Beta: This is also called as asset beta. It is one of the risk measurement unit which is used to compare the risk of company that doesnot have any debts with that of risk of the markets. In other words, risk of the company without dedts and risk of the market is compared.

a.

Answer to Problem 16PS

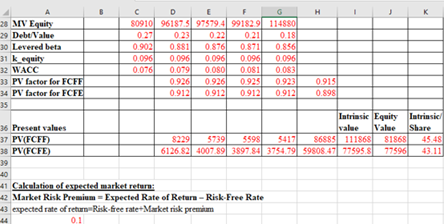

The intrinsic value when P/E ratio in the year 2020 is 16 will be $111868 and of FCFE will be $77595.80.

Explanation of Solution

Given information:

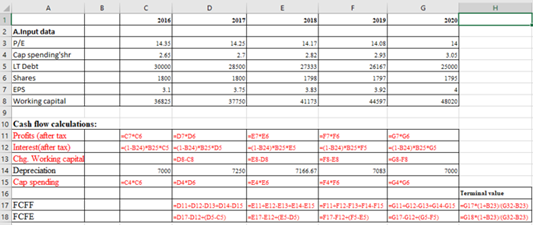

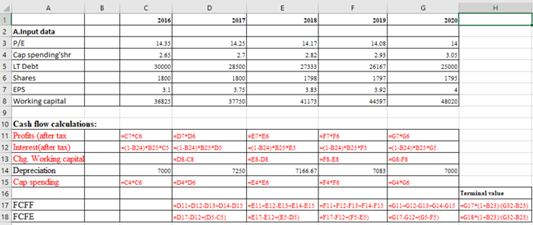

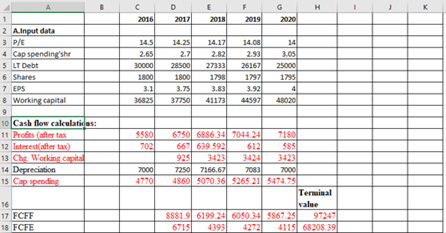

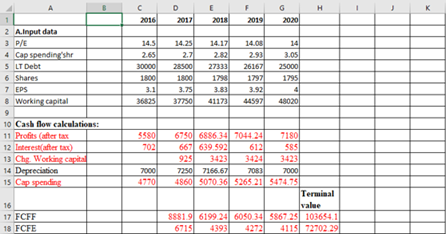

Spreadsheet 18.2 −

| 2016 | 2017 | 2018 | 2019 | 2020 | ||

| A.Input data | ||||||

| P/E | 14.35 | 14.25 | 14.17 | 14.08 | 14 | |

| Cap spending'shr | 2.65 | 2.7 | 2.82 | 2.93 | 3.05 | |

| LT Debt | 30000 | 28500 | 27333 | 26167 | 25000 | |

| Shares | 1800 | 1800 | 1798 | 1797 | 1795 | |

| EPS | 3.1 | 3.75 | 3.83 | 3.92 | 4 | |

| Working capital | 36825 | 37750 | 41173 | 44597 | 48020 | |

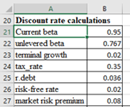

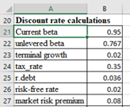

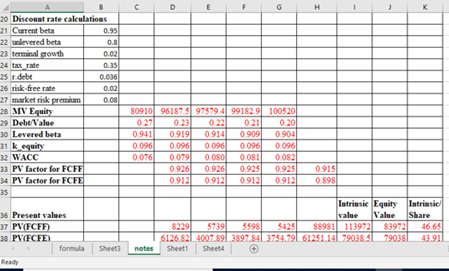

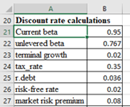

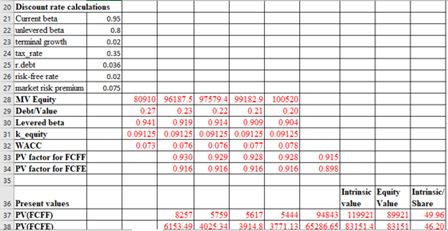

| Discount rate calculations | ||||||

| Current beta | 0.95 | |||||

| unlevered beta | 0.767 | |||||

| terminal growth | 0.02 | |||||

| tax_rate | 0.35 | |||||

| r.debt | 0.036 | |||||

| risk-free rate | 0.02 | |||||

| market risk premium | 0.08 |

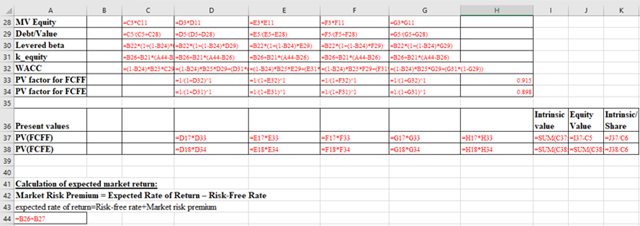

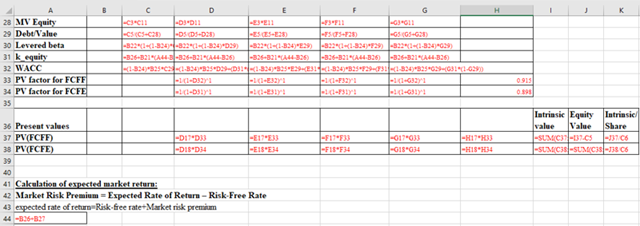

The formulas to be entered in the cells are as follows:

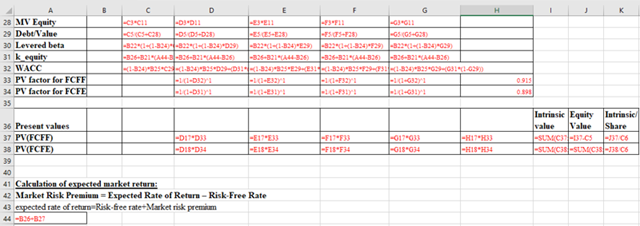

After inputing the required value in the cell related to G3, we get the following values.

Therefore the intrinsic value when P/E ratio in the year 2020 is 16 will be $111868 and of FCFE will be $77595.80

b.

To calculate: The intrinsic value when GE’s unlevered beta is 0.80.

Introduction:

Unlevered Beta: This is also called as asset beta. It is one of the risk measurement unit which is used to compare the risk of company that doesnot have any debts with that of risk of the markets. In other words, risk of the company without dedts and risk of the market is compared.

b.

Answer to Problem 16PS

The intrinsic value of FCFF is $113972 and FCFE is $79038.50.

Explanation of Solution

Given information:

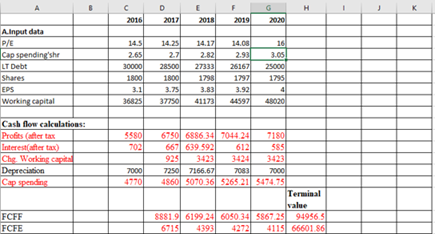

Spreadsheet 18.2 − Free cash flow model

| 2016 | 2017 | 2018 | 2019 | 2020 | ||

| A.Input data | ||||||

| P/E | 14.35 | 14.25 | 14.17 | 14.08 | 14 | |

| Cap spending'shr | 2.65 | 2.7 | 2.82 | 2.93 | 3.05 | |

| LT Debt | 30000 | 28500 | 27333 | 26167 | 25000 | |

| Shares | 1800 | 1800 | 1798 | 1797 | 1795 | |

| EPS | 3.1 | 3.75 | 3.83 | 3.92 | 4 | |

| Working capital | 36825 | 37750 | 41173 | 44597 | 48020 | |

| Discount rate calculations | ||||||

| Current beta | 0.95 | |||||

| unlevered beta | 0.767 | |||||

| terminal growth | 0.02 | |||||

| tax_rate | 0.35 | |||||

| r.debt | 0.036 | |||||

| risk-free rate | 0.02 | |||||

| market risk premium | 0.08 |

The formulas to be entered in the cells are as follows:

We need to change the vaue of unlevered beta from 0.767 to 0.80. After inputing the required value in the cell related to B22, we get the following values.

Therefore, the intrinsic value of FCFF is $113972 and FCFE is $79038.50.

c.

To calculate: Intrinsic value when the market risk premium is 7.5%

Introduction:

Unlevered Beta: This is also called as asset beta. It is one of the risk measurement unit which is used to compare the risk of company that doesnot have any debts with that of risk of the markets. In other words, risk of the company without dedts and risk of the market is compared.

c.

Answer to Problem 16PS

The intrinsic value of FCFF will be$ 119921 and for FCFE it will be $83151.40.

Explanation of Solution

Given information:

Spreadsheet 18.2 − Free cash flow model

| 2016 | 2017 | 2018 | 2019 | 2020 | ||

| A.Input data | ||||||

| P/E | 14.35 | 14.25 | 14.17 | 14.08 | 14 | |

| Cap spending'shr | 2.65 | 2.7 | 2.82 | 2.93 | 3.05 | |

| LT Debt | 30000 | 28500 | 27333 | 26167 | 25000 | |

| Shares | 1800 | 1800 | 1798 | 1797 | 1795 | |

| EPS | 3.1 | 3.75 | 3.83 | 3.92 | 4 | |

| Working capital | 36825 | 37750 | 41173 | 44597 | 48020 | |

| Discount rate calculations | ||||||

| Current beta | 0.95 | |||||

| unlevered beta | 0.767 | |||||

| terminal growth | 0.02 | |||||

| tax_rate | 0.35 | |||||

| r.debt | 0.036 | |||||

| risk-free rate | 0.02 | |||||

| market risk premium | 0.08 |

The formulas to be entered in the cells are as follows:

We need to change the vaue of unlevered beta from 0.08 to 0.075. After inputing the required value in the cell related to B27, we get the following values.

Therefore the intrinsic value of FCFE will be$ 119921 and for FCFE it will be $83151.40.

Want to see more full solutions like this?

Chapter 18 Solutions

EBK INVESTMENTS

- The following graph plots the current security market line (SML) and indicates the return that investors require from holding stock from Happy Corp. (HC). Based on the graph, complete the table that follows: REQUIRED RATE OF RETURN (Percent) 20.0 16.0 Return on HC's Stock X U 12.0 0.5 1.0 RISK (Beta) CAPM Elements Risk-free rate (TRF) Market risk premium (RPM) Happy Corp. stock's beta Required rate of return on Happy Corp. stock 1.5 Value 2.0 (?)arrow_forwardUse the following forecasted financials: (See pictures. Certain cells were left blank on prupose) b) Use the CAPM model to derive the cost of equity capital. Assume beta equals 1.09, the risk-free rate is 1.62%, and the market risk premium is 4.72%. a)Calculate residual income for 2021 and 2022. c) Calculate the present value of residual income for 2024 and 2025.arrow_forward(b) Write the equation of the Security Market Line (SML). Compute and draw the SML when the expected return of the NASDAQ index (market portfolio) is 17% and the return to the risk-free asset is 7% (c) Given the SML in (b), compute the beta and the expected return of the new share Facebook assuming the volatility of the NASDAQ index (market portfo- lio) is 23.86% and its covariance with the share is 0.0655. - (d) Facebook pays a dividend of 5 GBP and the growth of dividends is equal to 4% for the first two years and then rise to 6%. Assuming constant cost of capital as computed in point (c), estimate the price of the Facebook share. (e) Consider investing 20% of your wealth in the Facebook share with beta as in (c). What is the proportion you need to allocate to the Apple share with beta 1.8 in order to replicate the market portfolio? [arrow_forward

- Assume that the risk-free rate of return is 4% and the market risk premium (i.e., Rm- Re) is 8%. If use the Capital Asset Pricing Model (CAPM) to estimate the expected rate of return on a stock with a beta of 128, then this stock's exoected return should be ----- A) 10.53 B) 14.24% C) 2315% D) 6.59%arrow_forwardAssume that the risk-free rate of return is 4% and the market risk premium (ie., Rm - Re) is 89%. If use the Capital Asset Pricing Model (CAPM) to estimate the expected rate of return on a stock with a beta of 128, then this stock's exoected return should be A) 10.53% B) 14.24% 23.15% D) 6.59%arrow_forwardThe rate of return on the market stock index is 13 percent. The rate of return on a risk-freebank account is 1%. The B (beta) of stock XYZ is 1.5. Use the data to answer the questionsbelow.a. What is the market risk premium? Show your work.b. What is the cost of equity for XYZ? Show your work.c. What is the stock XYZ risk premium? Show your work.d. Draw the graph of the Security Market Line and show the stock of XYZ on the graph.The end-of-year dividend on stock ABC is expected to be $0.8. The growth rate of dividend isexpected to be 5 percent for ever. The current price of the ABC stock is $10. Use the data toanswer the questions below.e. What is the cost of equity for stock ABC? Show your work.f. Suppose stock KLM has the same end-of-year dividend, dividend growth rate andprice as stock ABC, but the risk of KLM stock is much greater than of the ABC stock.What is your estimate of the cost of equity of stock KLM using the method at part e?Do you agree with the valuation of the cost of…arrow_forward

- b) You are given the following information about Stock X and the market: The annual effective risk-frec rate is 5%. The expected return and volatility for Stock X and the market are shown in the table below: Expected Return Volatility Stock X 5% 40% Market 8% 25% The correlation between the returns of stock X and the market is -0.25. Assume the Capital Asset Pricing Model holds. Calculate the required return for Stock X and determine if the investor should invest in Stock X.arrow_forward(a) Write the equation of the Security Market Line (SML). Compute and draw the SML when the expected return of the NASDAQ index (market portfolio) is 17% and the return to the risk-free asset is 7%. (b) Given the SML in (b), compute the beta and the expected return of the new share Facebook assuming the volatility of the NASDAQ index (market portfolio) is 23.86% and its covariance with the share is 0.0655. can you help with barrow_forwardConsider the following simplified APT model: Factor Expected Risk Premium Market 6.4% Interest Rate -0.6% Yield Spread 5.1% Factor Risk Exposures Market Interest Rate Yield Spread Stock Stock (b1) (b2) (b3) P 1.0 -2.0 -0.2 P2 1.2 0 0.3 P3 0.3 0.5 1.0 a) Calculate the expected return for the above stocks. Assume risk free rate is 5%. Consider a portfolio with equal…arrow_forward

- Finance The risk-free rate is 3.7 percent and the expected return on the market is 12.3 percent. Stock A has a beta of 1.1and an expected return of 13.1 percent. Stock B has a beta of .86 and an expected return of 11.4 percent. Arethese stocks correctly priced? Why or why not? Use E(Ri) = Rf + βi(E(RM) − Rf).arrow_forwardConsider the following simplified APT model: Factor Expected Risk Premium Market 6.4% Interest Rate -0.6% Yield Spread 5.1% Factor Risk Exposures Market Interest Rate Yield Spread Stock Stock(b1) (b2) (b3) P 1.0 -2.0 -0.2 P2 1.2 0 0.3 P3 0.3 0.5 1.0 Required: 1. Calculate the expected return for the above stocks. Assume risk free rate is 5%. Consider a portfolio with equal investments in stocks P, P2 and P3 2.What are the factor risk exposures for the portfolio? 3.What is the portfolio’s expected return?arrow_forward2b) Write the equation of the Security Market Line (SML). Compute and draw the SML when the expected return of the NASDAQ index (market portfolio) is 17% and the return to the risk-free asset is 7%.arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT