Videos

Financial Reporting of Depreciation, Write-off, Bond Issuance and Common Stock Issuance, Purchase, Reissuance, and Cash Dividends (Chapters 4, 8, 9, 10, and 11)

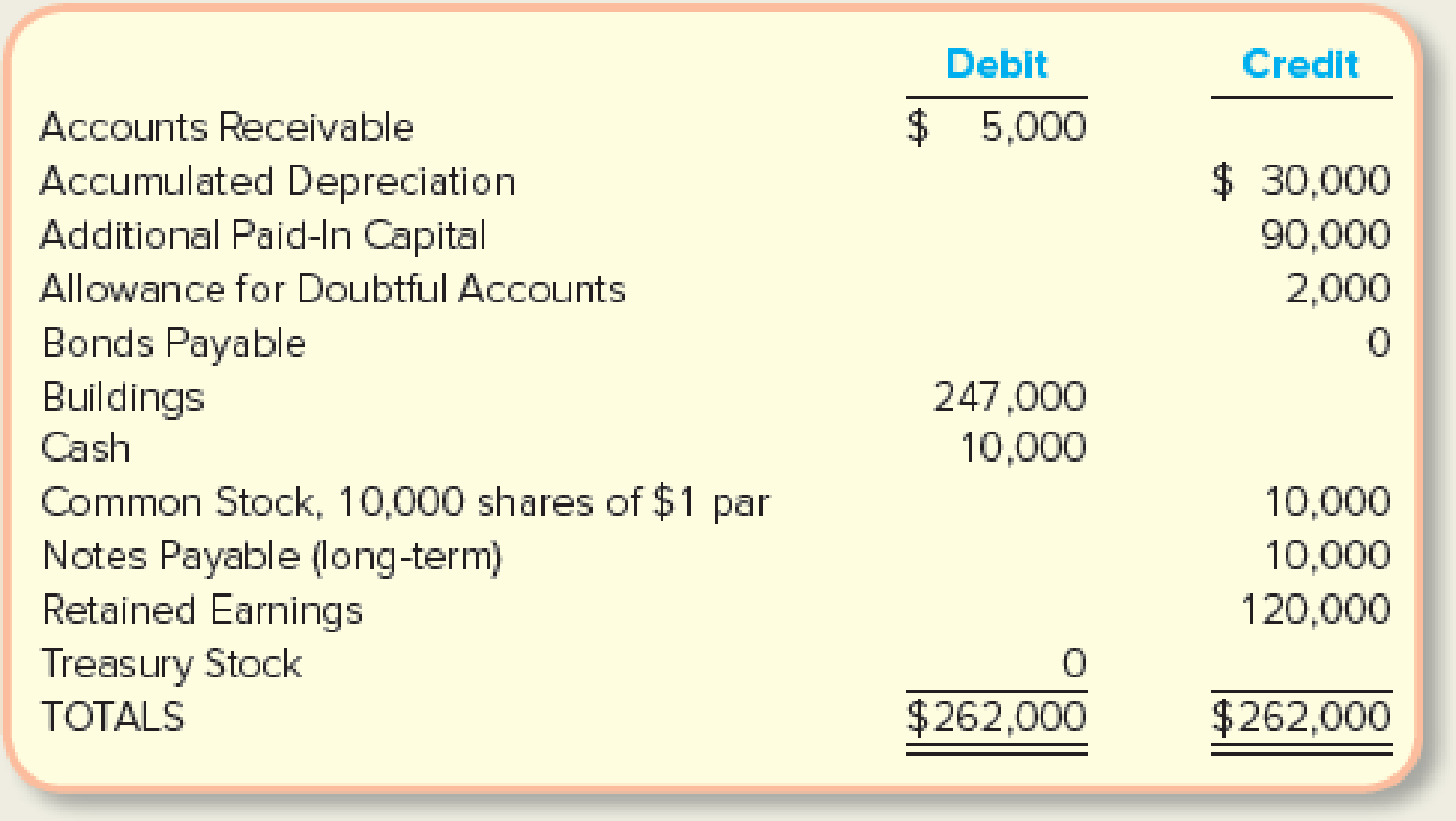

American Laser, Inc., reported the following account balances on January 1.

The company entered into the following transactions during the year.

| Jan. 15 | Issued 5,000 shares of $1 par common stock for $50,000 cash. |

| Jan. 31 | Collected $3,000 from customers on account. |

| Feb. 15 | Reacquired 3,000 shares of $1 par common stock into treasury for $33,000 cash. |

| Mar. 15 | Reissued 2,000 shares of |

| Aug. 15 | Reissued 600 shares of treasury stock for $4,600 cash. |

| Sept. 15 | Declared (but did not yet pay) a $1 cash dividend on each outstanding share of common stock. |

| Oct. 1 | Issued 100, 10-year, $1,000 bonds, at a quoted |

| Oct. 3 | Wrote off a $2,000 balance due from a customer who went bankrupt. |

| Dec. 29 | Recorded $230,000 of service revenue, all of which was collected in cash. |

| Dec. 30 | Paid $200,000 cash for this year’s wages through December 31. Ignore payroll taxes and payroll deductions. |

| Dec. 31 | Calculated $10,000 of depreciation for the year to be recorded. (Ignore accrual adjustments for interest and income taxes.) |

Required:

- 1. Analyze the effects of each transaction on total assets, liabilities, and stockholders’ equity.

- 2. Prepare journal entries to record each transaction.

- 3. Enter the January 1 balances into T-accounts,

post the journal entries from requirement 2, and determine ending balances. - 4. Prepare a closing

journal entry for the income statement accounts, assuming the events on December 29–31 were the only transactions to affect income statement accounts. - 5. Prepare the closing entry for Dividends.

- 6. Prepare a classified

balance sheet at December 31. - 7. Calculate the debt-to-assets ratio at January 1 and December 31. Does the company rely more (or less) on debt financing at the end of the year than at the beginning of the year?

1.

Analyze the effect of each transaction on total assets, liabilities and stockholder’s equity.

Explanation of Solution

Accounting equation:

Accounting equation is an accounting tool expressed in the form of equation, by creating a relationship between the resources or assets of a company, and claims on the resources by the creditors and the owners. Accounting equation is expressed as shown below:

Analyze the effect of each transaction on total assets, liabilities and stockholder’s equity as follows:

| Date of Transaction | Balance Sheet | ||

| Assets ($) | Liabilities ($) | Stockholder’s Equity ($) | |

| January 15 | Cash | NE |

Common Stock Additional paid –in capital |

| January 31 |

Cash+3,000 AR-3,000 | NE | NE |

| February 15 | Cash | NE | Treasury stock ( |

| March 15 | Cash | NE |

Treasury stock ( Additional paid –in capital |

| August 15 | Cash | NE |

Treasury stock ( Additional paid –in capital |

| September 15 | NE |

Dividends payable | Dividends ( |

| October 1 | Cash |

Bonds payable Premium on bonds payable | |

| October 3 |

AR AFDA | NE | NE |

| December 29 | Cash +230,000 | NE | Service Revenue+230,000 |

| December 30 | Cash +230,000 | NE | Salaries and Wages Expense (+E) -200,000 |

| December 31 | Accumulated depreciation -10,000 | NE | Depreciation Expense (+E) -10,000 |

(Table 1)

Note:

- NE: Denotes increase in the value

- AR: Accounts Receivable

- AFDA: Allowance for Doubtful Accounts (

2.

Prepare journal entries to record each transaction.

Explanation of Solution

Prepare journal entries to record each transaction as follows:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January 15 | Cash | 50,000 | |

| Common stock | 5,000 | ||

| Additional paid –in capital | 45,000 | ||

| (To record the issuance of common stock) | |||

| January 31 | Cash | 3,000 | |

| Accounts Receivable | 3,000 | ||

| (To record the cash received for customers) | |||

| February 15 | Treasury stock | 33,000 | |

| Cash | 33,000 | ||

| (To record the repurchase of common stock into treasury stock ) | |||

| March 15 | Cash | 24,000 | |

| Treasury Stock(2) | 22,000 | ||

| Additional paid –in capital | 2,000 | ||

| (To record the reissuance of treasury stock) | |||

| August 15 | Cash | 4,600 | |

| Additional paid-in capital | 2,000 | ||

| Treasury stock(3) | 6,600 | ||

| (To record the reissuance of 600 shares of treasury stock) | |||

| September 15 | Dividends (5) | 14,600 | |

| Dividends Payable | 14,600 | ||

| (To record the sale of merchandise on account) | |||

| October 1 | Cash(6) | 101,000 | |

| Bonds Payable (7) | 100,000 | ||

| Premium on bonds payable | 1,000 | ||

| (To record the issuance of bonds at a quoted bond price $101) | |||

| October 3 | Allowance for doubtful accounts | 2,000 | |

| Accounts Receivable | 2,000 | ||

| (To record the written off balance due from customer) | |||

| December 29 | Cash | 230,000 | |

| Service Revenue | 230,000 | ||

| (To record the service revenue earned) | |||

| December 30 | Salaries and Wages Expense | 200,000 | |

| Cash | 200,000 | ||

| (To record the payment of wages expenses) | |||

| December 31 | Depreciation Expense | 10,000 | |

| Accumulated Depreciation | 10,000 | ||

| (To record the depreciation expenses) | |||

Table (2)

Working notes (1):

Working notes (2):

Working notes (3):

Working notes (4):

Working notes (5):

Working notes (6):

Working notes (7):

3.

Record the January 1 balance in the T-accounts and post the journal entries to the T-accounts.

Explanation of Solution

Record the January 1 balance in the T-accounts and post the journal entries to the T-accounts as follows:

|

Cash (A) | |||

| Bal | 10,000 | ||

| 15-Jan | 50,000 | 33,000 | 15-Feb |

| 31-Jan | 3,000 | 200,000 | 30-Dec |

| 15-Mar | 24,000 | ||

| 15-Aug | 4,600 | ||

| 1- Oct | 101,000 | ||

| 29-Dec | 230,000 | ||

| 189,600 | |||

| Accounts Receivable (A) | |||

| Bal. | 5,000 | 3,000 | 31-Jan |

| 2,000 | 3-Oct | ||

| 0 | |||

| Buildings | |||

| Bal. | 247,000 | ||

| 247,000 | |||

| Allowance for Doubtful Accounts (xA) | |||

| 3-Oct | 2,000 | 2,000 | Bal. |

| 0 | |||

| Accumulated Dep.–Building(xA) | |||

| 30,000 | Bal. | ||

| 30,000 | |||

| Dividends Payable (L) | |||

| 0 | Bal. | ||

| 14,600 | 15-Sep | ||

| 14,600 | |||

| Notes Payable (L) | |||

| 10,000 | Bal. | ||

| 10,000 | |||

| Bonds Payable (L) | |||

| 0 | Bal. | ||

| 100,000 | 1-Oct | ||

| 100,000 | |||

| Premium on Bonds Payable (-L) | |||

| 0 | Bal. | ||

| 1,000 | 1-Oct | ||

| 1,000 | |||

| Common Stock (SE) | |||

| 10,000 | Bal. | ||

| 5,000 | 15-Jan | ||

| 15,000 | |||

| Additional Paid-In Capital (SE) | |||

| 90,000 | Bal. | ||

| 45,000 | 15-Jan | ||

| 15-Aug | 2,000 | 2,000 | 15-Mar |

| 135,000 | |||

| Treasury Stock (xSE) | |||

| Bal. | 0 | ||

| 15-Feb | 33,000 | 22,000 | 15-Mar |

| 6,600 | 15-Aug | ||

| 4,400 | |||

| Dividends (D) | |||

| Bal. | 0 | ||

| 15-Sep | 14,600 | ||

| 14,600 | |||

| Service Revenue (R) | |||

| 0 | Bal. | ||

| 230,000 | 29-Dec | ||

| 230,000 | |||

| Salaries and Wages Expense (E) | |||

| Bal. | 0 | ||

| 30-Dec | 200,000 | ||

| 200,000 | |||

| Depreciation Expense (E) | |||

| Bal. | 0 | ||

| 31-Dec | 10,000 | ||

| 10,000 | |||

| Retained Earnings (SE) | |||

| 120,000 | Bal. | ||

| 120,000 | |||

4.

Prepare a closing journal entry for the income statement accounts, assume that the events occurred on December 29 to 31 were the only transactions to affect income statement accounts.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to Retained Earnings account are referred to as closing entries. The revenue, expense, and dividends accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Prepare a closing journal entry for the income statement accounts, assume that the events occurred on December 29 to 31 were the only transactions to affect income statement accounts.

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| December 31 | Service Revenue | 230,000 | |

| Salaries and Wages Expense | 200,000 | ||

| Depreciation Expense | 10,000 | ||

| Retained Earnings | 20,000 | ||

| (To record the closure of expense account to income summary) |

(Table 3)

Revenue account:

In this closing entry, service revenue account is closed by transferring the amount of service revenue to the retained earnings account in order to bring the revenue account balance to zero. Hence, debit the service revenue account and credit retained earnings account.

Expenses account:

In this closing entry, expenses account is closed by transferring the amount of expenses to the retained earnings in order to bring the expenses account balance to zero. Hence, debit the retained earnings account and credit all expenses account.

5.

Prepare the closing entry for dividends.

Explanation of Solution

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| December 31 | Retained Earnings | 14,600 | |

| Dividends (5) | 14,600 | ||

| (To record the closing entry of dividends) |

(Table 4)

- Retained earnings are a component of stockholder’s equity and there is a decrease in the value of equity. Hence, it is debited.

- Dividend is a component of stockholder’s equity and there is an increase in the value of dividend. Hence, it is credited.

6.

Prepare a classified balance sheet at December 31.

Explanation of Solution

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections, and sub-sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

Prepare a classified balance sheet at December 31:

| Incorporation A | ||

| Classified Balance Sheet | ||

| At December 31 | ||

| Assets | ||

| Current Assets: | ||

| Cash | $189,600 | |

| Accounts Receivable | 0 | |

| Allowance for Doubtful Accounts | 0 | |

| Total Current Assets | 189,600 | |

| Buildings | 247,000 | |

| Less: Accumulated Depreciation | -40,000 | |

| 207,000 | ||

| Total Assets | $396,600 | |

| Liabilities and Stockholders’ Equity | ||

| Liabilities | ||

| Current Liabilities | ||

| Dividends Payable | $14,600 | |

| Total Current Liabilities | 14,600 | |

| Noncurrent Liabilities: | ||

| Notes Payable (long-term) | 10,000 | |

| Bonds Payable | 100,000 | |

| Premium on Bonds Payable | 1,000 | |

| Total Noncurrent Liabilities | 111,000 | |

| Total Liabilities (a) | 125,600 | |

| Stockholders’ Equity | ||

| Contributed Capital: | ||

| Common Stock, | 15,000 | |

| Additional Paid-in Capital | 135,000 | |

| Total Contributed Capital | 150,000 | |

| Retained Earnings (8) | 125,400 | |

| Less: Treasury Stock, at cost | -4,400 | |

| Total Stockholders’ Equity (b) | 271,000 | |

| Total Liabilities and Stockholders’ Equity | $396,600 | |

(Table 5)

Working notes (8):

7.

Calculate the debt-to-assets ratio at January 1 and December 31. Describe whether the company rely more (or less) on debt financing at the end of the year than at the beginning of the year.

Explanation of Solution

Calculate the debt-to-assets ratio at January 1:

Calculate the debt-to-assets ratio at December 31

Working notes (9):

Compute the total assets at January 1:

| Particulars | $ |

| Cash | $10,000 |

| Accounts Receivable | 5,000 |

| Less: Allowance for doubtful accounts | -2,000 |

| Buildings | 247,000 |

| Less: Accumulated Depreciation | -30,000 |

| Total | $230,000 |

(Table 6)

Want to see more full solutions like this?

Chapter 11 Solutions

Fundamentals Of Financial Accounting

- Stockholders' Equity section of balance sheet The following accounts and their balances appear in the ledger of Goodale Properties Inc. on June 30 of the current year: Prepare the Stockholders Equity section of the balance sheet as of June 30. Eighty thousand shares of common stock are authorized, and 9,000 shares have been reacquired.arrow_forwardThe income statement, statement of retained earnings, and balance sheet for Somerville Company are as follows: Includes both state and federal taxes. Brief Exercise 15-20 Calculating the Average Common Stockholders Equity and the Return on Stockholders Equity Refer to the information for Somerville Company on the previous pages. Required: Note: Round answers to four decimal places. 1. Calculate the average common stockholders equity. 2. Calculate the return on stockholders equity.arrow_forwardSunland Company had these transactions during the current period. June 12 Issued 83,500 shares of $1 par value common stock for cash of $313,125. July 11 Issued 3,450 shares of $101 par value preferred stock for cash at $105 per share. Nov. 28 Purchased 2,950 shares of treasury stock for $8,450. Prepare the journal entries for the Sunland Company transactions shown above. (Record journal entries in the order presented in the problem. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Date Account Titles and Explanation Debit Credit choose a transaction date June 12July 11Nov. 28 enter an account title enter a debit amount enter a credit amount enter an account title enter a debit amount enter a credit amount enter an account title…arrow_forward

- Instructions Journalize the selected transactions. Selected transactions completed by Equinox Products Inc. during the fiscal year ended December 31, Year 1, were as follows: a. Issued 15,000 shares of $20 par common stock at $30, receiving cash. b. Issued 4,000 shares of $80 par preferred 5% stock at $100, receiving cash. c. Issued $500,000 of 10-year, 5% bonds at 104, with interest payable semiannually. d. Declared a quarterly dividend of $0.50 per share on common stock and $1.00 per share on preferred stock. On the date of record, 100,000 shares of common stock were outstanding, no treasury shares were held and 20,000 shares of preferred stock were outstanding. e. Paid the cash dividends declared in (d). f. Purchased 7,500 shares of Solstice Corp. at $40 per share plus a $150 brokerage commission. The investment is classified as an available-forsale investment. g. Purchased 8,000 shares of treasury common stock at $33 per share. h. Purchased 40,000 shares of Pinkberry Co. stock…arrow_forwardBlossom Company had these transactions during the current period. June 12 Issued 83,500 shares of $1 par value common stock for cash of $313,125. July 11 Issued 2,800 shares of $101 par value preferred stock for cash at $106 per share. Nov. 28 Purchased 3,350 shares of treasury stock for $8,450. Prepare the journal entries for the Blossom Company transactions shown above. (Record journal entries in the order presented in the problem. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.)arrow_forwardThe following selected transactions occurred for Corner Corporation: Feb. 1 Purchased 400 shares of the company’s own common stock at $20 cash per share; the stock is now held in treasury. July 15 Issued 100 of the shares purchased on February 1 for $30 cash per share. Sept. 1 Issued 60 more of the shares purchased on February 1 for $15 cash per share. Required: Show the effects of each transaction on the accounting equation. Give the indicated journal entries for each of the transactions. What impact does the purchase of treasury stock have on dividends paid? What impact does the reissuance of treasury stock for an amount higher than the purchase price have on net income?arrow_forward

- Selected transactions completed by Equinox Products Inc. during the fiscal year ended December 31, Year 1, were as follows: 1. Journalize the selected transactions. a. Issued 15,000 shares of $20 par common stock at $30, receiving cash. b. Issued 4,000 shares of $80 par preferred 5% stock at $100, receiving cash c. Issued $500,000 of 10-year, 5% bonds at 104, with interest payable semiannually. d. Declared a quarterly dividend of $0.50 per share on common stock and $1.00 per share on preferred stock. On the date of record, 100,000 shares of common stock were outstanding, no treasury shares were held and 20,000 shares of preferred stock were outstanding. e. Paid the cash dividends declared in (d). f. Purchased 7,500 shares of Solstice Corp. at $40 per share plus a $150 brokerage commission. The investment is classified as an available-for-sale investment. g. Purchased 8,000 shares of treasury common stock at $33 per share h. Purchased 40,000 shares of Pinkberry Co. stock…arrow_forwardSelected transactions completed by Equinox Products Inc. during the fiscal year ended December 31, 20Y5, were as follows: Record on journal page 10: Jan. 3 Issued 15,000 shares of $20 par common stock at $30, receiving cash. Feb. 15 Issued 4,000 shares of $80 par preferred $1 stock at $100, receiving cash. May 1 Issued $500,000 of 10-year, 5% bonds at 104, with interest payable semiannually. 16 Declared a quarterly dividend of $0.50 per share on common stock and $1.00 per share on preferred stock. On the date of record, 100,000 shares of common stock were outstanding, no treasury shares were held and 20,000 shares of preferred stock were outstanding. Journalize this transaction as two separate entries. 26 Paid the cash dividends declared on May 16. Jun. 1 Purchased 4% bonds issued by Solstice Corp. as an available-for-sale investment for $300,150. 8 Purchased 8,000 shares of treasury common stock at $33 per share. 22 Purchased 40,000 shares of Pinkberry Co.’s…arrow_forwardSelected transactions completed by Equinox Products Inc. during the fiscal year ended December 31, 20Y5, were as follows: Record on journal page 10: Jan. 3 Issued 15,000 shares of $20 par common stock at $30, receiving cash. Feb. 15 Issued 4,000 shares of $80 par preferred $1 stock at $100, receiving cash. May 1 Issued $500,000 of 10-year, 5% bonds at 104, with interest payable semiannually. May 16 Declared a quarterly dividend of $0.50 per share on common stock and $1.00 per share on preferred stock. On the date of record, 100,000 shares of common stock were outstanding, no treasury shares were held and 20,000 shares of preferred stock were outstanding. Journalize this transaction as two separate entries. May 26 Paid the cash dividends declared on May 16. June 1 Purchased 4% bonds issued by Solstice Corp. as an available-for-sale investment for $300,150. June 8 Purchased 8,000 shares of treasury common stock at $33 per share. June 22…arrow_forward

- Selected transactions completed by Equinox Products Inc. during the fiscal year ended December 31, 20Y5, were as follows: Record on journal page 10: Jan. 3 Issued 15,000 shares of $20 par common stock at $30, receiving cash. Feb. 15 Issued 4,000 shares of $80 par preferred $1 stock at $100, receiving cash. May 1 Issued $500,000 of 10-year, 5% bonds at 104, with interest payable semiannually. 16 Declared a quarterly dividend of $0.50 per share on common stock and $1.00 per share on preferred stock. On the date of record, 100,000 shares of common stock were outstanding, no treasury shares were held and 20,000 shares of preferred stock were outstanding. Journalize this transaction as two separate entries. 26 Paid the cash dividends declared on May 16. Jun. 1 Purchased 4% bonds issued by Solstice Corp. as an available-for-sale investment for $300,150. 8 Purchased 8,000 shares of treasury common stock at $33 per share. 22 Purchased 40,000 shares of Pinkberry Co.’s…arrow_forwardDuring the year the following selected transactions affecting stockholders' equity occurred for Orlando Corporation: a. April 1: Repurchased 390 shares of the company's common stock at $38 cash per share. b. June 14: Sold 70 of the shares purchased on April 1 for $43 cash per share. c. September 1: Sold 60 of the shares purchased on April 1 for $33 cash per share. Required: 1. Prepare journal entries for each of the above transactions. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Answer is not complete. No 1 Date April 01 General Journal Debit Credit Treasury stock 14,820 Cash 14,820 2 June 14 Cash Treasury stock Additional paid-in capital 3,010 2,660 350 3 September 01 Cash 1,980 Additional paid-in capital Treasury stock 300X 1,680 xarrow_forwardThe following selected transactions occurred for Corner Corporation: Feb. 1 Purchased 420 shares of the company’s own common stock at $22 cash per share; the stock is now held in treasury. July 15 Issued 110 of the shares purchased on February 1 for $32 cash per share. Sept. 1 Issued 70 more of the shares purchased on February 1 for $17 cash per share. Required: Indicate the account, amount, and direction of the effect for the above transactions. (Enter any decreases to account balances with a minus sign.) Prepare journal entries for each of the transactions. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.) What impact does the purchase of treasury stock have on dividends paid?arrow_forward

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning