1.

Prepare a single column revenue journal and cash receipt journal, and post the accounts in the accounts payable subsidiary ledger.

1.

Explanation of Solution

General Ledger: General ledger refers to the ledger that records all the transactions of the business related to the company’s assets, liabilities, owners’ equities, revenues, and expenses. Each subsidiary ledger is represented in the general ledger by summarizing the account.

Accounts payable control account and subsidiary ledger: Accounts payable account and subsidiary ledger is the ledger which is used to post the creditors transaction in one particular ledger account. It helps the business to locate the error in the creditor ledger balance. After all transactions of creditor accounts are posted, the balances in the accounts payable subsidiary ledger should be totaled, and compare with the balance in the general ledger of accounts payable. If both the balance does not agree, the error has been located and corrected.

Purchase journal: Purchase journal refers to the journal that is used to record all purchases on account. In the purchase journal, all purchase transactions are recorded only when the business purchased the goods on account. For example, the business purchased cleaning supplies on account.

Cash payments journal: Cash payments journal refers to the journal that is used to record all transaction which involves the cash payments. For example, the business paid cash to employees (salary paid to employees).

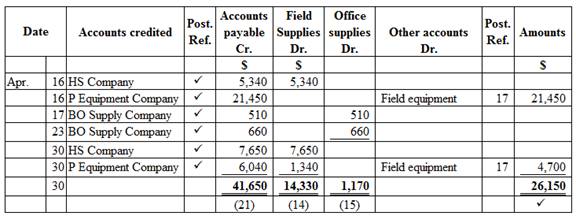

Purchase journal: Purchase journal of Company AF in the month of April is as follows:

Purchase journal

Figure (1)

Cash payment journal: Cash payment journal of Company AF in the month of April is as follows:

Cash payment journal

| Date | Check No. | Account debited | Post Ref. | Other accounts Dr. | Accounts payable Dr. | Cash Dr. | |

| Apr. | 16 | 1 | Rent expense | 71 | 3,500 | 3,500 | |

| 19 | 2 | Field supplies | 14 | 3,340 | 3,340 | ||

| Office supplies | 15 | 400 | 400 | ||||

| 23 | 3 | Land | 19 | 140,000 | 140,000 | ||

| 24 | 4 | HS Company | ✓ | 5,340 | 5,340 | ||

| 26 | 5 | P Equipment Company | ✓ | 21,450 | 21,450 | ||

| 30 | 6 | BO Supply Company | ✓ | 510 | 510 | ||

| 30 | 7 | Salary expense | 61 | 29,400 | 29,400 | ||

| 30 | 176,640 | 27,300 | 203,940 | ||||

| ✓ | (21) | (11) | |||||

Table (1)

Accounts payable subsidiary ledger

| Name: BO Supply Company | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| April | 17 | P1 | 510 | 550 | ||

| 23 | P1 | 660 | 1,170 | |||

| 30 | CP1 | 510 | 660 | |||

Table (2)

| Name: HS Company | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| April | 16 | P1 | 5,340 | 5,340 | ||

| 24 | CP1 | 5,340 | - | |||

| 30 | P1 | 7,650 | 7,650 | |||

Table (3)

| Name: P Equipment Company | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| April | 16 | P1 | 21,450 | 21,450 | ||

| 26 | CP1 | 21,450 | - | |||

| 30 | P1 | 6,040 | 6,040 | |||

Table (4)

2. and 3.

2. and 3.

Explanation of Solution

Prepare the general ledger for given accounts as follows:

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| April | 30 | CP1 | 203,940 | 203,940 | |||

Table (5)

| Account: Field supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| April | 19 | CP1 | 3,340 | 3,340 | |||

| 30 | P1 | 14,330 | 17,670 | ||||

Table (6)

| Account: Office supplies Account no. 15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| April | 19 | CP1 | 400 | 400 | |||

| 30 | P1 | 1,170 | 1,570 | ||||

Table (7)

| Account: Field equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| April | 16 | P1 | 21,450 | 21,450 | |||

| 30 | P1 | 4,700 | 26,150 | ||||

| 30 | J1 | 12,000 | 14,150 | ||||

Table (8)

| Account: Land Account no. 19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| April | 23 | CP1 | 140,000 | 140,000 | |||

| 30 | J1 | 12,000 | 152,000 | ||||

Table (9)

| Account: Accounts payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| April | 30 | P1 | 41,650 | 41,650 | |||

| 30 | CP1 | 27,300 | 14,350 | ||||

Table (10)

| Account: Salary expense Account no. 61 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| April | 30 | CP1 | 29,400 | 29,400 | |||

Table (11)

| Account: Rent expense Account no. 71 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| April | 16 | CP1 | 3,500 | 3,500 | |||

Table (12)

| Journal Page 01 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| April | 30 | Land | 19 | 12,000 | |

| Field equipment | 17 | 12,000 | |||

| (To record the acquisition of land in exchange for field equipment) | |||||

Table (13)

4.

Prepare the accounts payable creditor balances.

4.

Explanation of Solution

Accounts payable creditor balance

Accounts payable creditor balance is as follows:

| Company AF | |

| Accounts payable creditor balances | |

| April 30 | |

| Amount ($) | |

| BO Supply Company | 660 |

| HS Company | 7,650 |

| P Equipment Company | 6,040 |

| Total accounts receivable | 14,350 |

Table (14)

Accounts payable controlling account

Ending balance of accounts payable controlling account is as follows:

| Company AF | |

| Accounts payable (Controlling account) | |

| April 30 | |

| Amount ($) | |

| Opening balance | 0 |

| Add: | |

| Total credits (from purchase journal) | 41,650 |

| 41,650 | |

| Less: | |

| Total debits (from cash payment journal) | (27,300) |

| Total accounts payable | 14,350 |

Table (15)

In this case, accounts payable subsidiary ledger is used to identify, and locate the error by way of cross check the creditor balance and accounts payable controlling account. From the above calculation, we can understand that the both balance of accounts payable is agree, hence there is no error in the recording and posing of transactions.

5.

Discuss the reason for using subsidary ledger for the field equipment.

5.

Explanation of Solution

A subsidiary ledger for the field equipment helps the company to track the cost of each piece of equipment, location, useful life, and other necessary data. This information is useful for safeguarding the equipment, and determining depreciation of equipment.

Want to see more full solutions like this?

Chapter 5 Solutions

Financial Accounting

- The cash payments and purchases journals for Outdoor Artisan Landscaping follow. The accounts payable control account has a June 1, 20Y1, balance of 2,230, consisting of an amount owed to Augusta Sod Co. Prepare a schedule of the accounts payable creditor balances and determine that the total agrees with the ending balance of the accounts payable controlling account.arrow_forwardAll problems can be completed manually or by using either MyAccountingLab General Ledger or QuickBooks. Using the purchases, cash payments, and general journals The general ledger of Finnish Lake Golf Shop includes the following selected accounts, along with their account numbers: Transactions in December that affected purchases and cash payments were as follows: Requirements Use the appropriate journal to record the preceding transactions in a purchases journal, a cash payments journal (omit the Check No. column), and a general journal. Finnish Lake Golf Shop records purchase returns in the general journal. The company uses the perpetual inventory system. Total each column of the special journals. Show that total debits equal total credits in each special journal. Show how postings would be made from the journals by writing the account numbers and check marks in the appropriate places in the journals.arrow_forwardMiss Angela recently joined A2A Limited as an accounting clerk. As a part of the financial reporting process, she receives the following source documents to prepare journal vouchers for general ledger entries. purchase orders, sales invoices, and vendor invoices Angela posts the journal vouchers to the general ledger and the related subsidiary ledgers at the end of each day. Each month the clerk reconciles the subsidiary accounts to their control accounts in the general ledger to ensure that they balance. Required: Discuss any control weaknesses and risks associated with the accounting information system of A2A Limited.arrow_forward

- Miss Anglea recently joined A2A Limited as an accounting clerk. As a part of financial reporting process, she receives the following source documents to prepare journal vouchers for general ledger entries. purchase orders, sales invoices, and vendor invoices At the end of each day, Angela posts the journal vouchers to the general ledger and the related subsidiary ledgers. Each month the clerk reconciles the subsidiary accounts to their control accounts in the general ledger to ensure that they balance. Required: Discuss any control weaknesses and risks associated with the accounting information system of A2A Limited. Please provide references as well.arrow_forwardTransactions related to purchases and cash payments completed by Wisk Away Cleaning Services Inc. during the month of May 20Y5 are as follows: Prepare a purchases journal and a cash payments journal to record these transactions. The forms of the journals are similar to those illustrated in the text. Place a check mark () in the Post. Ref. column to indicate when the accounts payable subsidiary ledger should be posted. Wisk Away Cleaning Services Inc. uses the following accounts:arrow_forwardVendor account reconciliations are performed by three clerks in the accounts payabledepartment on Friday of each week. The accounts payable supervisor reviews thecompleted reconciliations the following Monday to ensure they have been completed.The work performed by the supervisor is an example of which COSO component?(1) Control activities (3) Risk assessment(2) Information and communication (4) Monitoringarrow_forward

- 1. You are tasked to perform cut-off procedures for expenses and its related payable. In testing the completeness/cut-off assertion, what document would you most likely inspect? Group of answer choices a. Accounts payable subsidiary ledger. b. Vendor invoice register 15 days before and 15 days after report date. c. Purchase journal 15 days before and 15 days after report date. d. Cash disbursement journal 15 days before and 15 days after report date. 2. During the review of loan contracts and agreements, the auditor would most likely figure out the following, except: Group of answer choices a. The existence of loans. b. The completeness of loans. c. The accuracy of interest expense recorded by the entity. d. Related disclosures pertaining to assets pledged as collateral.arrow_forwardDance Studio created a $200 imprest petty cash fund. During the month, the fund custodian authorized and signed petty cash tickets as follows: Requirement 1. Make the general journal entry to create the petty cash fund. Include an explanation. (Record debits first, then, credits. Select the explanation on the last line of the journal entry table.) Date Accounts and Explanation Debit Credit Requirement 2. Make the general journal entry to record the petty cash fund replenishment. Cash in the fund totals $8. Include an explanation. (Record debits first, then, credits. Select the explanation on the last line of the journal entry table. Prepare a single compound journal entry.) Date Accounts and Explanation Debit Credit Requirement 3. Assume that Louise's Dance Studio decides to decrease the petty cash fund to $100. Make the general journal entry to record this decrease. (Record debits first, then, credits. Select the explanation on the last line of the journal entry table.) Date Accounts…arrow_forwardThe petty cash custodian reported the following transactions during the month. Prepare the journalentry to record the replenishment of the fund.A $10 cash payment is made to Starbucks to purchase coffee for a business client, a $40 cashpayment is made for supplies purchased from Office Depot, and a $30 cash payment is made toUPS to deliver goods to a customerarrow_forward

- Transactions for petty cash, cash short and overJeremiah Restoration Company completed the following selectedtransactions during January: Instructions Journalize the transactionsarrow_forwardKelley Company has completed the following October sales and purchases journals: a. Total and post the journals to T accounts for the general ledger and the accounts receivable and accounts payable ledgers. b. Complete a schedule of accounts receivable for October 31, 20--. c. Complete a schedule of accounts payable for October 31, 20--. d. Compare the balances of the schedules with their respective general ledger accounts. If they are not the same, find and correct the error(s).arrow_forwardThe following describes the purchases and cash disbursements procedures for a lawn and garden supply wholesaler that uses central computer system terminals with in departments. The inventory control clerk visually reviews inventory levels from his computer terminal to identify items that need to be ordered. He then prints and sends a hard copy purchase requisition for the needed items to the purchasing agent. Based on the requisi- tion, the purchasing agent selects a vendor and adds a digital record to the purchase order file from terminal in the purchasing department. The clerk then prints a hard copy of the purchase order and mails it to the vendor. Finally, the purchasing agent destroys the purchase requisition, which it is no longer niceded since the relevant details are on the PO. When the materials arrive at the receiving department a receiving clerk prints a copy of the purchase order from his terminal and reconciles to the packing slip. The clerk then manually creates wo-part…arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning