Concept explainers

Videos

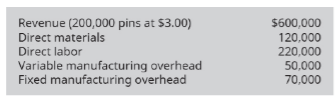

Aspen Enterprises makes award pins for various events. Budget information regarding the current period is:

A fraternity with which Aspen has a long relationship approached Aspen with a special order for 6,000 pins at a price of $2.75 per pin. Variable costs will be the same as the current production, and the special order will not impact the rest of the company’s orders. However, Aspen is operating at capacity and will incur an additional $5,000 in fixed manufacturing overhead if the order is accepted. Based on this information, what is the differential income (loss) associated with accepting the special order?

Want to see the full answer?

Check out a sample textbook solution

Chapter 10 Solutions

Principles of Accounting Volume 2

Additional Business Textbook Solutions

Financial Accounting (12th Edition) (What's New in Accounting)

Managerial Accounting (4th Edition)

Principles of Accounting Volume 1

Financial Accounting (11th Edition)

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

- Foy Company has a welding activity and wants to develop a flexible budget formula for the activity. The following resources are used by the activity: Four welding units, with a lease cost of 12,000 per year per unit Six welding employees each paid a salary of 50,000 per year (A total of 9,000 welding hours are supplied by the six workers.) Welding supplies: 300 per job Welding hours: Three hours used per job During the year, the activity operated at 90 percent of capacity and incurred the actual activity and resource costs, shown on page 676. Lease cost: 48,000 Salaries: 315,000 Parts and supplies: 805,000 Required: 1. Prepare a flexible budget formula for the welding activity using welding hours as the driver. 2. Prepare a performance report for the welding activity. 3. What if welders were hired through outsourcing and paid 30 per hour (the welding equipment is provided by Foy)? Repeat Requirement 1 for the outsourcing case.arrow_forwardNovo, Inc., wants to develop an activity flexible budget for the activity of moving materials. Novo uses eight forklifts to move materials from receiving to stores. The forklifts are also used to move materials from stores to the production area. The forklifts are obtained through an operating lease that costs 18,000 per year per forklift. Novo employs 25 forklift operators who receive an average salary of 50,000 per year, including benefits. Each move requires the use of a crate. The crates are used to store the parts and are emptied only when used in production. Crates are disposed of after one cycle (two moves), where a cycle is defined as a move from receiving to stores to production. Each crate costs 1.80. Fuel for a forklift costs 3.60 per gallon. A gallon of gas is used every 20 moves. Forklifts can make three moves per hour and are available for 280 days per year, 24 hours per day (the remaining time is downtime for various reasons). Each operator works 40 hours per week and 50 weeks per year. Required: 1. Prepare a flexible budget for the activity of moving materials, using the number of cycles as the activity driver. 2. Calculate the activity capacity for moving materials. Suppose Novo works at 80 percent of activity capacity and incurs the following costs: Prepare the budget for the 80 percent level and then prepare a performance report for the moving materials activity. 3. Calculate and interpret the volume variance for moving materials. 4. Suppose that a redesign of the plant layout reduces the demand for moving materials to one-third of the original capacity. What would be the budget formula for this new activity level? What is the budgeted cost for this new activity level? Has activity performance improved? How does this activity performance evaluation differ from that described in Requirement 2? Explain.arrow_forwardNovo, Inc., wants to develop an activity flexible budget for the activity of moving materials.Novo uses eight forklifts to move materials from receiving to stores. The forklifts are also usedto move materials from stores to the production area. The forklifts are obtained through an operating lease that costs $18,000 per year per forklift. Novo employs 25 forklift operators whoreceive an average salary of $50,000 per year, including benefits. Each move requires the use of a crate. The crates are used to store the parts and are emptied only when used in production.Crates are disposed of after one cycle (two moves), where a cycle is defined as a move from receiving to stores to production. Each crate costs $1.80. Fuel for a forklift costs $3.60 per gallon. A gallon of gas is used every 20 moves. Forklifts can make three moves per hour and are available for 280 days per year, 24 hours per day (the remaining time is downtime for various reasons). Each operator works 40 hours per week and 50…arrow_forward

- Sneaky Snacky Squirrel Inc. has a budget of $900,000 in 2021 for prevention costs. If it decides to automate a portion of its prevention activities, it will save $80,000 in variable costs. The new method will require $40,000 in training costs and $100,000 in annual equipment costs. Management is willing to adjust the budget for an amount up to the cost of the new equipment. The budgeted production level is 150,000 units. Appraisal costs for the year are budgeted at $600,000. The new prevention procedures will save appraisal costs of $50,000. Internal failure costs average $15 per failed unit of finished goods. The internal failure rate is expected to be 3% of all completed items. The proposed changes will cut the internal failure rate by one-third. Internal failure units are destroyed. External failure costs average $54 per failed unit. The company's average external failures average 3% of units sold. The new proposal will reduce this rate by 50%. Assume all units produced are sold…arrow_forwardSneaky Snacky Squirrel Inc. has a budget of $900,000 in 2021 for prevention costs. If it decides to automate a portion of its prevention activities, it will save $80,000 in variable costs. The new method will require $40,000 in training costs and $100,000 in annual equipment costs. Management is willing to adjust the budget for an amount up to the cost of the new equipment. The budgeted production level is 150,000 units. Appraisal costs for the year are budgeted at $600,000. The new prevention procedures will save appraisal costs of $50,000. Internal failure costs average $15 per failed unit of finished goods. The internal failure rate is expected to be 3% of all completed items. The proposed changes will cut the internal failure rate by one-third. Internal failure units are destroyed. External failure costs average $54 per failed unit. The company's average external failures average 3% of units sold. The new proposal will reduce this rate by 50%. Assume all units produced are sold…arrow_forwardThe management of Springer plc is considering next year’s production and purchase budget. One of the components produced by the company, which is incorporated into another product before being sold, has budgeted manufacturing costs as follows: $ Direct Material 14 Direct labour (4 hours at $3 per hour) 12 Variable overhead (4 hours at $2 per hour) 8 Fixed overheads (4 hours at $5 per hour) 20 Total Cost $54 per unit Trigger plc has offered to supply the above component at a guaranteed price of $50 per unit. Required: Considering cost criteria only, advise management whether the above component should be purchased from Trigger plc. Any calculation should be shown and assumptions made, or aspects which may require further investigation should be clearly stated. Explain how your advice would be affected by the following: “As a result of recent government legislation if Springer plc continues to manufacture this component, the company will incur additional inspection and…arrow_forward

- QC Corp has the following budget amounts for the current year: $1,100,000 for prevention costs and $880,000 for appraisal costs. Internal failure equals $100 per failed item and external failure has a total budget of $660,000. The Product Testing department has proposed a new method of testing products. If management decides to implement the new method, $2.20 per unit of appraisal costs will be saved, up to a level of 150,000 tests. No additional savings are expected past the 150,000 level. The new method involves $104,500 in training costs and $71,500 in yearly testing supplies. If the new testing method is implemented what is the revised budget for appraisal costs, assuming 550,000 units are tested during the current year?arrow_forwardLucky Lager has just purchased the Austin Brewery. The brewery is two years old and uses absorption costing. It will “sell” its products to Lucky Lager at $45 per barrel. Paul Brandon, Lucky Lager’s controller, obtains the following information about Austin Brewery’s capacity and budgeted fixed manufacturing costs for 2012: Denominator-Level Capacity Concept Budgeted Fixed MOH per period Days of Production per period Hours of production per day Barrels per hour Theoretical capacity $28,000,000 360 24 540 Practical capacity $28,000,000 350 20 500 Normal capacity utilization $28,000,000 350 20 400 Master-Budget capacity for each half year: a) January – June 2012 b) July – December 2012 $14,000,000 $14,000,000 175 175 20 20 320 480 Required: Compute the budgeted fixed MOH rate per barrel for each of the denominator-level capacity concepts. Explain why they are different.arrow_forwardAl Khoud Training Center (KTC) is an industrial training company operating in Muscat Knowledge Oasis. Following increased competition and customer expectations, KTC has been forced to revisit its operational strategy and its quality standards. The following budgeted data for 2022 are available: Number of Trainees 6,000 Operating Income OMR45,000 Budgeted Variable Cost per Trainee Trainee's Support Service Training Materials Foods Miscellaneous Products & Services OMR15 Budgeted Fixed Cost per Training 16,000 5,000 OMR26 Facilities OMR12 Salaries OMR22 Based on the customer survey it conducted, KTC has learned that several improvements to its products and services are required. The improvements would provide the following impacts: Increase in the Number of Trainees Increase in the Total Variable Costs Increase in the Total Fixed Costs 70% 65% 50% You are required to: (0) Calculate the budgeted revenue per trainee based on the available data. (i) Assuming that budgeted revenue per…arrow_forward

- SafeNow sells its main product, ergonomic mouse pads, for $11 each. Its variable cost is $5.20 per pad. Fixed costs are $205,000 per month for volumes up to 65,000 pads. Above 65,000 pads, monthly fixed costs are $255,000. Prepare a monthly flexible budget for the product, showing sales revenue, variable costs, fixed costs, and operating income for volume levels of 40,000, 45,000, and 75,000 pads. SafeNow Flexible Budget Budget Amounts Per Unit 75.000 45,000 Units back @ # * 3 $ 40.000 IOI 4 5 6 4- & 7 LO T 9 O 44 ←arrow_forwardEagle Sales has developed the following budgeted income statement. The company is experimenting with new engineering techniques and believes it can reduce variable cost to $4 per unit and significantly improve the product. The innovations would increase fixed cost to $10,000. The company expects to be able to maintain current sales (2,500 units). Assuming Eagle decides to pursue this strategy, by what amount would the budgeted profit ?change Sales Revenue (2.500 units x $10 sales price) Total Variable Expenses (2,500 x S6 per unit). Contribution Margin Fixed Expenses Net Income S25,000 (15,000) 10,000 (6,000) $4.000 decrease by $4,000 ) increase by S4,000 decrease by $1,000 O decrease by $2,000 increase by $1,000arrow_forwardErgoNow sells its main product, ergonomic mouse pads, for $12 each. Its variable cost is $5.40 per pad. Fixed costs are $200,000 per month for volumes up to 65,000 pads. Above 65,000 pads, monthly fixed costs are $260,000. Prepare a monthly flexible budget for the product, showing sales revenue, variable costs, fixed costs, and operating income for volume levels of 35,000, 45,000, and 75,000 pads. ErgoNow Flexible Budget Budget Amounts Per Unit Units 35,000 45,000 75,000 (1) (2) (3) (4) (5) (1) Contribution Margin Fixed Costs Operating Income Sales Revenue Variable Costs (2) Contribution Margin Fixed Costs Operating Income Sales Revenue Variable Costs (3)…arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning