Concept explainers

Videos

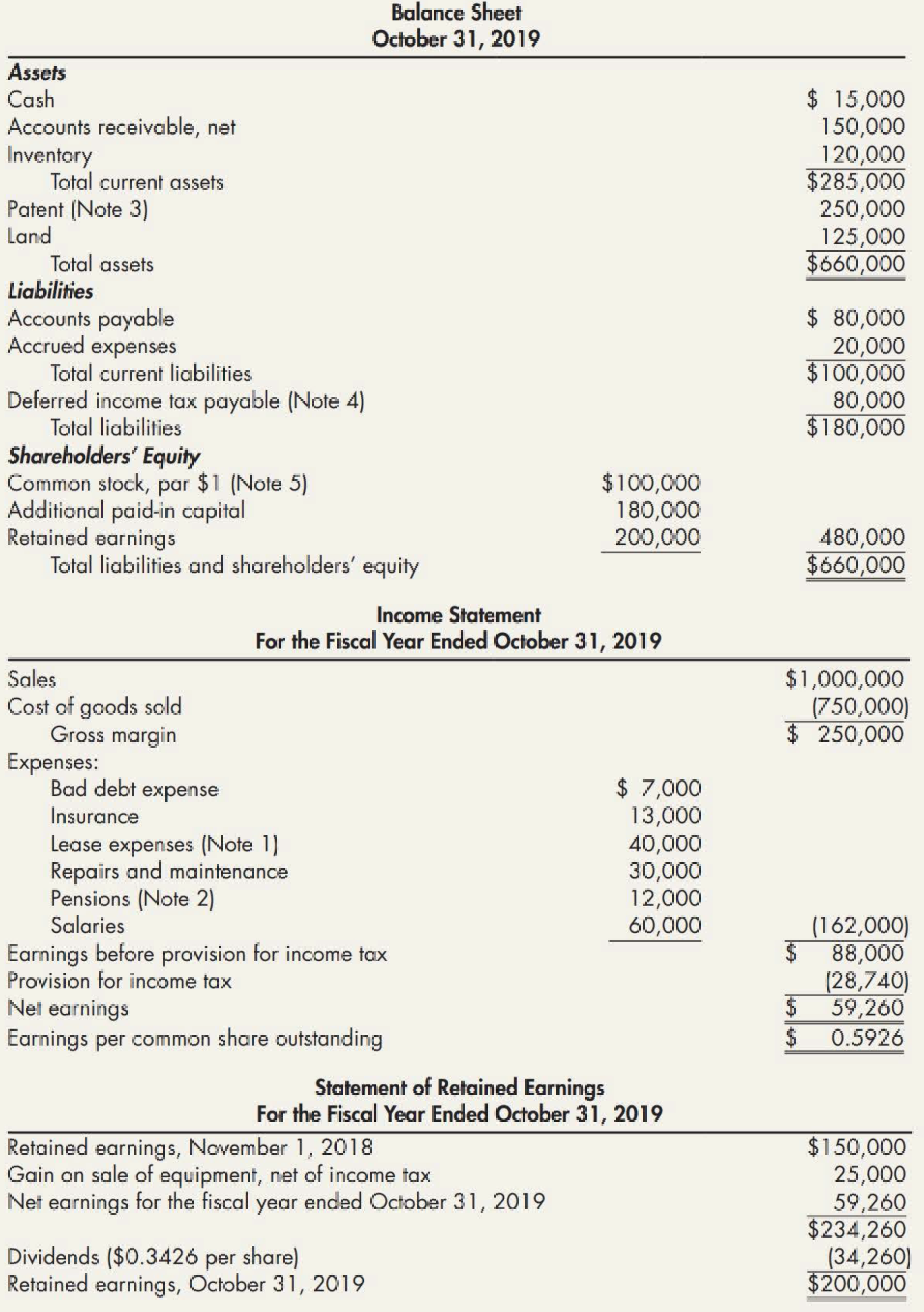

Financial Statement Violations of U.S. GAAP The following are the financial statements issued by Allen Corporation for its fiscal year ended October 31, 2019:

Notes to Financial Statements:

1. Long-Term Lease. Under the terms of a 5-year, noncancelable lease for a building, Allen is obligated to make annual rental payments of $40,000 in each of the next 4 fiscal years.

2. Pension Plan. Substai1tially all employees are covered by Allen’s defined benefit pension plan. Pension expense is equal to the total of pension benefits accrued and paid to retired employees during the year. Because it is a defined benefit plan that is paid every year, no pension liability exists.

3. Patent. The patent had an estimated remaining life of 10 years at the time of purchase. Allen’s patent was purchased from Apex Corporation on January 1, 2019, for $250,000.

4.

5. Warrants. On January 1, 2018, one common stock warrant was issued to shareholders of record for each common share owned. An additional share of common stock is to be issued upon exercise of 10 stock warrants and receipt of an amount equal to par value. For the 6 months ended October 31, 2019, the average market value for Allen’s common stock was $5 per share and no warrants had yet been exercised.

6.

Required:

Next Level Review the preceding financial state1nents and related notes. Identify any inclusions or exclusions from them that would be in violation of GAAP, and indicate corrective action to be taken. Do not comment as to format or style. Respond in the following order:

1.

2. Notes

3. Income statement

4. Statement of

5. General

Trending nowThis is a popular solution!

Chapter 5 Solutions

Intermediate Accounting: Reporting And Analysis

- Lessee Accounting Issues Timmer Company signs a lease agreement dated January 1, 2019, that provides for it to lease equipment from Landau Company beginning January 1, 2019. The lease terms, provisions, and related events are as follows: The lease is noncancelable and has a term of 5 years. The annual rentals are 83,222.92, payable at the end of each year, and provide Landau with a 12% annual rate of return on its net investment. Timmer agrees to pay all executory costs directly to a third party on December 1 of each year. In 2019, these were insurance, 3,760; property taxes, 5,440. In 2020: insurance, 3,100; property taxes, 5,330. There is no renewal or bargain purchase option. Timmer estimates that the equipment has a fair value of 300,000, an economic life of 5 years, and a zero residual value. Timmers incremental borrowing rate is 16%, it knows the rate implicit in the lease, and it uses the straightline method to record depreciation on similar equipment. Required: 1. Calculate the amount of the asset and liability of Timmer at the inception of the lease. (Round to the nearest dollar.) 2. Prepare a table summarizing the lease payments and interest expense. 3. Prepare journal entries on the books of Timmer for 2019 and 2020. 4. Next Level Prepare a partial balance sheet in regard to the lease for Timmer for December 31, 2019. Use the present value of next years payment approach to classify the finance lease obligation between current and noncurrent. 5. Next Level Prepare a partial balance sheet in regard to the lease for Timmer for December 31, 2019. Use the change in present value approach to classify the finance lease obligation between current and noncurrent.arrow_forwardLessee Accounting with Payments Made at Beginning of Year Adden Company signs a lease agreement dated January 1, 2019, that provides for it to lease non-specialized heavy equipment from Scott Rental Company beginning January 1, 2019. The lease terms, provisions, and related events are as follows: 1. The lease term is 4 years. The lease is noncancelable and requires annual rental payments of 20,000 to be paid in advance at the beginning of each year. 2. The cost, and also fair value, of the heavy equipment to Scott at the inception of the lease is 68,036.62. The equipment has an estimated life of 4 years and has a zero estimated residual value at the end of this time. 3. Adden agrees to pay all executory costs directly to a third party. 4. The lease contains no renewal or bargain purchase options. 5. Scotts interest rate implicit in the lease is 12%. Adden is aware of this rate, which is equal to its borrowing rate. 6. Adden uses the straight-line method to record depreciation on similar equipment. 7. Executory costs paid at the end of the year by Adden are: Required: 1. Next Level Determine what type of lease this is for Adden. 2. Prepare a table summarizing the lease payments and interest expense for Adden. 3. Prepare journal entries for Adden for the years 2019 and 2020.arrow_forwardLessee Accounting Issues Sax Company signs a lease agreement dated January 1, 2019, that provides for it to lease computers from Appleton Company beginning January 1, 2019. The lease terms, provisions, and related events are as follows: 1. The lease term is 5 years. The lease is noncancelable and requires equal rental payments to be made at the end of each year. The computers are not specialized for Sax. 2. The computers have an estimated life of 5 years, a fair value of 300,000, and a zero estimated residual value. 3. Sax agrees to pay all executory costs directly to a third party. 4. The lease contains no renewal or bargain purchase options. 5. The annual payment is set by Appleton at 83,222.92 to earn a rate of return of 12% on its net investment. Sax is aware of this rate. Saxs incremental borrowing rate is 10%. 6. Sax uses the straight-line method to record depreciation on similar equipment. Required: 1. Next Level Examine and evaluate each capitalization criteria and determine what type of lease this is for Sax. 2. Calculate the amount of the asset and liability of Sax at the inception of the lease (round to the nearest dollar). 3. Prepare a table summarizing the lease payments and interest expense. 4. Prepare journal entries for Sax for the years 2019 and 2020.arrow_forward

- Lessee and Lessor Accounting Issues The following information is available for a noncancelable lease of equipment entered into on March 1, 2019. The lease is classified as a sales-type lease by the lessor (Anson Company) and as a finance lease by the lessee (Bullard Company). Assume that the lease payments are nude at the beginning of each month, interest and straight-line depreciation are recognized at the end of each month, and the residual value of the leased asset is zero at the end of a 3-year life. Required: 1. Record the lease (including the initial receipt of 2,000) and the receipt of the second and third installments of 2,000 in Ansons accounts. Carry computations to the nearest dollar. 2. Record the lease (including the initial payment of 2,000), the payment of the second and third installments of 2,000, and monthly depreciation in Bullards accounts. The lessee records the lease obligation at net present value. Carry computations to the nearest dollar.arrow_forwardLessor Accounting Issues Ramsey Company leases heavy equipment to Terrell Inc. on March 1, 2019, on the following terms: 1. Twenty-four lease rentals of 2,950 at the beginning of each month are to be paid by Terrell, and the lease is noncancelable. 2. The cost of the heavy equipment to Ramsey was 55,000. 3. Ramsey uses an implicit interest rate of 18% per year and will account for this lease as a sales-type lease. Required: Prepare journal entries for Ramsey (the lessor) to record the lease contract on March 1, 2019, the receipt of the first two lease rentals, and any interest income for March and April 2019. (Round your answers to the nearest dollar.)arrow_forwardLessee and Lessor Accounting Issues Diego Leasing Company agrees to provide La Jolla Company with equipment under a noncancelable lease for 5 years. The equipment has a 5-year life, cost Diego 25,000, and will have no residual value when the lease term ends. The fair value of the equipment is 30,000. La Jolla agrees to pay all executory costs (500 per year) throughout the lease period directly to a third party. On January 1, 2019, the equipment is delivered. Diego expects a 14% return on its net investment. The five equal annual rents are payable in advance starting January 1, 2019. Required: 1. Assuming this is a sales-type lease for the Diego and a finance lease for the La Jolla, prepare a table summarizing the lease and interest payments suitable for use by either party. 2. Next Level On the assumption that both companies adjust and close books each December 31, prepare journal entries relating to the lease for both companies through December 31, 2020, based on data derived in the table. Assume that La Jolla depreciates similar equipment by the straight line methodarrow_forward

- Determining Type of Lease and Subsequent Accounting On January 1, 2019, Caswell Company signs a 10-year cancelable (at the option of either party) agreement to lease a storage building from Wake Company. The following information pertains to this lease agreement: 1. The agreement requires rental payments of 100,000 at the beginning of each year. 2. The cost and fair value of the building on January 1, 2019, is 2 million. The storage building has not been specialized for Caswell. 3. The building has an estimated economic life of 50 years, with no residual value. Caswell depreciates similar buildings according to the straight-line method. 4. The lease does not contain a renewable option clause. At the termination of the lease, the building reverts to the lessor. 5. Caswells incremental borrowing rate is 14% per year. Wake set the annual rental to ensure a 16% rate of return (the loss in service value anticipated for the term of the lease). Caswell knows the implicit interest rate. 6. Executory costs of 7,000 annually, related to taxes on the property, are paid by Caswell directly to the taxing authority on Dec. 31 of each year. Required: 1. Determine what type of lease this is for the lessee. 2. Prepare appropriate journal entries on the lessees books to reflect the signing of the lease agreement and to record the payments and expenses related to this lease for the years 2019 and 2020.arrow_forwardA debtor firm’s 12/31/21 statement of financial position is to be issued of 4/15/22. A long-term obligation contracted in 2019 for settlement on 1/15/22 was extinguished through cash payment on its due date. On 1/20/22, a 5-year note was issued to replace the cash used up for the payment made on 1/15/22. Which of the following statements is correct? Group of answer choices The original obligation should be reported in the 2021 statement of financial position as a current liability because the entity does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting period. The new obligation entered into on 1/20/22 should be reported in the 2022 statement of financial position as a non-current liability because it is due to be settled beyond twelve months after the reporting period. The original obligation should be reported in the 2022 statement of financial position as a non-current liability because the entity does have an…arrow_forwardA Co entered into an agreement to lease office space on 1 April 2019 for afixed period of five years. As an incentive to encourage the office spaceto be occupied, a first-year rent-free period was included in theagreement after which A Co is required to pay an annual lease ofP360,000. How much lease should be accounted for in the year ended 31March 2020? A. P0B. P288,000C. P360,000D. P1,440,000arrow_forward

- Canton Cave Company provided the following schedule of liabilities on December 31, 2019: Accounts payable Notes payable-bank Interest payable Mortgage payable-10% Bonds payable *Bank notes payable include two separate notes payable to First Bank > AP3, 000,000, 10% note issued March 1, 2018, payable on demand. Interest is payable every six 6,500,000 8,000,000 150,000 2,000,000 4,000,000 months. > A one-year, P5,000,000, 11% note issued January 2, 2019. On December 31, 2019, Canton Cave negotiated a written agreement with First Bank to replace the note with a 2-year, P5,000,000, 10% note issued January 2, 2020. *The 10% mortgage note was issued October 1, 2016 with a term of 10 years. > Terms of the note give the holder the right to demand immediate payment if the entity fails to make a monthly interest within 10 days of the date the payment is due. On December 31, 2019, Canton Cave is three months behind in paying its required initial payment. The bonds payable are 10-year, 8% bonds,…arrow_forwardAccounting Delray Leasing Company signs an agreement on January 1, 2020, to lease equipment to Swifty Company. The following information relates to this agreement. 1. The term of the non-cancelable lease is 4 years with no renewal option. The equipment has an estimated economic life of 6years. 2. The fair value of the asset at January 1, 2020, is $118,700. 3. The asset will revert to the lessor at the end of the lease term, at which time the asset is expected to have a residual value of $22,600, none of which is guaranteed. 4. The agreement requires equal annual rental payments of $26,886.99 to the lessor, beginning on January 1, 2020. 5. The lessee’s incremental borrowing rate is 6%. The lessor’s implicit rate is 5% and is unknown to the lessee. 6. Swifty uses the straight-line depreciation method for all equipment. Click here to view factor tables.Prepare all of the journal entries for the lessee for 2020 to record the lease agreement, the lease…arrow_forwardLessee Accounting On June 1, 2020, Halifax Corporation leases equipment from Thunder Bay Manufacturing Ltd. The lease agreement indicates that Halifax can purchase the equipment at the end of the lease term for a specified price. Assume that both companies follow ASPE. Details pertaining to the lease agreement follow: Price at which Halifax can purchase the equipment at the end of the lease term $ 25,502 Annual lease payment, due at the beginning of each year $ 25,683 Halifax's incremental interest rate 8% Interest rate implicit in the lease 10% Leased asset's estimated fair value at the end of the lease term $ 89,169 Estimated useful life of equipment (in years) 12 Lease term (in years) 10 Fair value of the equipment at the inception of the lease $ 217,761 Estimated residual value of equipment at end of asset's useful life $ - Halifax uses the straight-line…arrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning