Concept explainers

Videos

The following

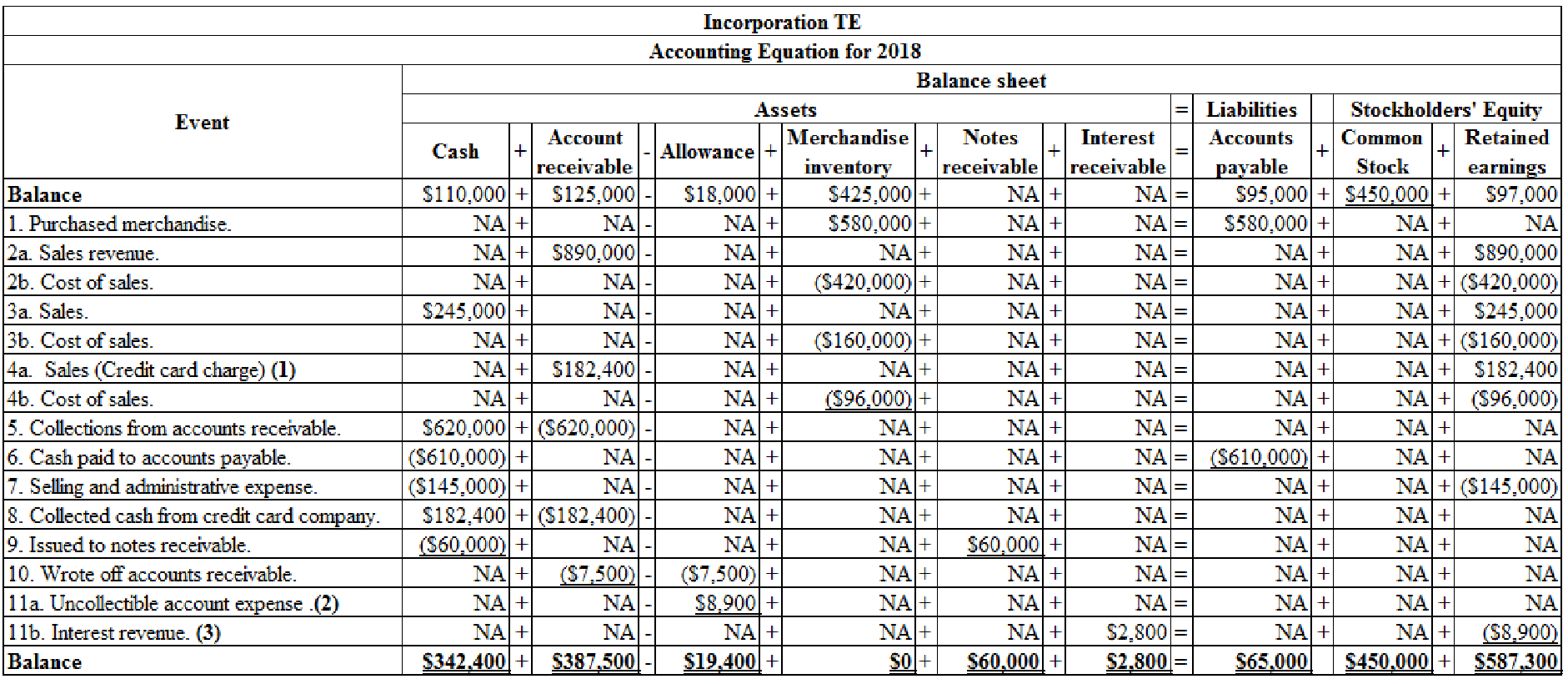

Tile, Etc. had the following transactions in 2018:

- 1. Purchased merchandise on account for $580,000.

- 2. Sold merchandise that cost $420,000 for $890,000 on account.

- 3. Sold for $245,000 cash merchandise that had cost $160,000.

- 4. Sold merchandise for $190,000 to credit card customers. The merchandise had cost $96,000. The credit card company charges a 4 percent fee.

- 5. Collected $620,000 cash from accounts receivable.

- 6. Paid $610,000 cash on accounts payable.

- 7. Paid $145,000 cash for selling and administrative expenses.

- 8. Collected cash for the full amount due from the credit card company (see item 4).

- 9. Loaned $60,000 to J. Parks. The note had an 8 percent interest rate and a one-year term to maturity.

- 10. Wrote off $7,500 of accounts as uncollectible.

- 11. Made the following

adjusting entries :- (a) Recorded uncollectible accounts expense estimated at 1 percent of sales on account.

- (b) Recorded seven months of accrued interest on the note at December 31, 2018 (see item 9).

Required

- a. Organize the transaction data in accounts under an

accounting equation. - b. Prepare an income statement, a statement of changes in stockholders’ equity, a

balance sheet , and a statement of cash flows for 2018.

a.

Organize the transaction data in accounts under an accounting equation.

Explanation of Solution

Percentage of sales method: Credit sales are recorded by debiting (increasing) accounts receivable account. The bad debts is a loss incurred out of credit sales, hence uncollectible accounts can be estimated as a percentage of credit sales or total sales.

It is a method of estimating the bad debts (expected loss on extending credit), by multiplying the expected percentage of uncollectible with the total amount of net credit sale (or total sales) for a specific period. Under percentage of sales method, estimated bad debts would be treated as a bad debt expense of the particular period.

Horizontal statements model: The model that represents all the financial statements, balance sheet, income statement, and statement of cash flows in one table in a horizontal form, is referred to as, horizontal statements model.

Organize the transaction data in accounts under an accounting equation.

Table (1)

Working note:

(1) Calculate the amount of credit card sales made to customers:

The merchandise sold to credit card customers for $190,000 and the company charges a fee of 4% on sales. So, the credit card expense is

(2) Calculate the amount for uncollectible accounts expense:

Calculate the amount of interest receivable:

Given: The loan amount is $60,000 and the rate of interest is 8%. So the total interest income is calculated as follows:

b.

Prepare an income statement, statement of changes in stockholders’ equity, a balance sheet, and a statement of cash flows for 2018.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare the income statement.

| Incorporation TE | ||

| Income statement | ||

| For the year ended December 31, 2018 | ||

| Particulars | Amount | Amount |

| Revenue | ||

| Sales revenue | $1,325,000 | |

| Less: Cost of goods sold | $676,000 | |

| Gross profit | $649,000 | |

| Less: Operating Expenses | ||

| Credit card expenses | $7,600 | |

| Selling and administrative expenses | $145,000 | |

| Uncollectible accounts expense | $8,900 | |

| Total operating income | ($161,500) | |

| Operating income | $487,500 | |

| Add: Non-operating items | ||

| Interest revenue | $2,800 | |

| Net income | $490,300 | |

Table (2)

Statement of changes in the stockholders’ equity: This statement reflects whether the components of stockholders’ equity have increased or decreased during the period.

Prepare the statement of changes in stockholders’ equity.

| Incorporation TE | ||

| Statement of changes in stockholders’ equity | ||

| For the year ended December 31, 2018 | ||

| Particulars | Amount | Amount |

| Beginning common stock | $450,000 | |

| Add: Common stocks issued | $0 | |

| Ending common stock | $450,000 | |

| Beginning retained earnings | $97,000 | |

| Add: Net income | $490,300 | |

| Less: Dividends | ($0) | |

| Ending retained earnings | $587,300 | |

| Total stockholders’ equity | $1,037,300 | |

Table (3)

Balance sheet: Balance Sheet is one of the financial statements that summarize the assets, the liabilities, and the Shareholder’s equity of a company at a given date. It is also known as the statement of financial status of the business.

Prepare the balance sheet.

| Incorporation TE | ||

| Balance sheet | ||

| As of December 31, 2018 | ||

| Particulars | Amount | Amount |

| Assets | ||

| Cash | $342,400 | |

| Accounts receivable | $387,500 | |

| Less: Allowance for doubtful accounts | $19,400 | $368,100 |

| Merchandise inventory | $329,000 | |

| Interest receivable | $2,800 | |

| Notes receivable | $60,000 | |

| Total assets | $1,102,300 | |

| Liabilities | ||

| Accounts payable | $65,000 | |

| Total liabilities | $65,000 | |

| Stockholders’ equity | ||

| Common stock | $450,000 | |

| Retained earnings | $587,300 | |

| Total stockholders' equity | $1,037,300 | |

| Total liabilities and stockholders' equity | $1,102,300 | |

Table (4)

Statement of cash flows: This statement reports all the cash transactions involves for inflow and outflow of cash, and the result of these transactions is reported as an ending balance of cash at the end of reported period.

Prepare the statement of cash flows.

| Incorporation TE | ||

| Statement of cash flow | ||

| For the year December 31, 2018 | ||

| Particulars | Amount | Amount |

| Cash flow from operating activities: | ||

| Inflow from customers (4) | $1,047,400 | |

| Outflow for inventory | ($610,000) | |

| Outflow for expenses | ($145,000) | |

| Net cash flow from operating activities | $292,400 | |

| Cash flow from investing activities | ||

| Outflow for notes receivable | ($60,000) | |

| Net cash flow from investing activities | ($60,000) | |

| Cash flow from financing activities | $0 | |

| Net change in cash | $232,400 | |

| Add: Beginning cash balance | $110,000 | |

| Ending cash balance | $342,400 | |

Table (5)

Working note:

(4) Calculate the amount of inflow from customers.

Want to see more full solutions like this?

Chapter 5 Solutions

Survey Of Accounting

- Toby Company had the following sales transactions for March: Mar. 6Sold merchandise on account to Osbourne, Inc., invoice no. 1128, 563.17. 14Sold merchandise on account to Ortiz Company, invoice no. 1129, 823.50. 20Sold merchandise on account to Bailey Corporation, invoice no. 1130, 2,350.98. 24Sold merchandise on account to Shannon Corporation, invoice no. 1131, 1,547.07. Assume that Toby Company had beginning balances on March 1 of 3,569.80 (Sales 411) and 2,450.39 (Accounts Receivable 113). Record the sales of merchandise on account in the sales journal (page 24) and then post to the general ledger.arrow_forwardGuardian Services Inc. had the following transactions during the month of April: a. Record the June purchase transactions for Guardian Services Inc. in the following purchases journal format: b. What is the total amount posted to the accounts payable and office supplies accounts from the purchases journal for April? c. What is the April 30 balance of the Officemate Inc. creditor account assuming a zero balance on April 1?arrow_forwardRead through the information below for selected transactions during the month of December, 2021 and prepare the required jounal entry to record the transaction. Post each of the entries below to the general ledger T-accounts attached . Sold Merchandise for $5,000 to Lee Corp on account on December 9. Cost of the merchandise was $3,390 and the terms of the sale were 1/15, n/30.arrow_forward

- On March 1, Crunk Company sold merchandise in the amount of $5.800 to Wells Company, with credit terms of 2/10, n/30. The cost of the items sold is $4,000. Crunk uses the perpetual inventory system and the gross method. On July 5, Wells returns some of the merchandise. The selling price of the merchandise is $500 and the cost of the merchandise returned is $350. The entry or entries that Crunk must make on July 5 is: 500 Accounts receivable Sales returns and allowances Sales returns and allowances Accounts receivable Accounts receivable Sales returns and allowances: Cost of goods sold Merchandise inventory Sales returns and allowances Accounts receivable Sales returns and allowances Accounts receivable Merchandise inventory Cost of goods sold 350 & B see 350 500 500 350 500 350 500 350 See 500 350arrow_forwardOn December 28, 20Y3, Silverman Enterprises sold $17,500 of merchandise to Beasley Co. with terms 2/10, n/30. The cost of the goods sold was $11,900. On December 31, 20Y3, Silverman prepared its adjusting entries, yearly financial statements, and closing entries. On January 3, 20Y4, Silverman Enterprises issued Beasley Co. a credit memo for returned merchandise. The invoice amount of the returned merchandise was $4,400 and the merchandise originally cost Silverman Enterprises $2,450. a. Journalize the entries by Silverman Enterprises to record the December 28, 20Y3 sale, using the net method under a perpetual inventory system. If an amount box does not require an entry, leave it blank. 20Y3 Dec. 28 20Y3 Dec. 28 b. Journalize the entries by Silverman Enterprises to record the merchandise returned by Beasley Co. on January 3, 20Y4. If an amount box does not require an entry, leave it blank. 20Y4 Jan. 3 20Y4 Jan. 3 c. Journalize the entry to record the receipt of the amount due by Beasley…arrow_forwardSheridan Co. uses the gross method to record sales made on credit. On June 1, 2020, it made sales of $45,000 with terms 4/15, n/45. On June 12, 2020, Sheridan received full payment for the June 1 sale. Prepare the required journal entries for Sheridan Co. (If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.arrow_forward

- Blossom Co. uses the gross method to record sales made on credit. On June 1, 2025, it made sales of $62,000 with terms 3/15, n/45. On June 12, 2025, Blossom received full payment for the June 1 sale. Prepare the required journal entries for Blossom Co. (If no entry is required, select "No Entry" for the account titles and enter o for the amounts. Credit account titles are automatically indented when the amount is entered. Do not indent manually. List all debit entries before credit entries. Record journal entries in the order presented in the problem.) Date Account Titles and Explanation Debit 10 Creditarrow_forwardOn March 1, Pearl Industries sold merchandise on account to Amelia Company for $30,300, terms 2/10, net 45. On March 6, Amelia returns merchandise with a sales price of $1,200. On March 11, Pearl Industries receives payment from Amelia for the balance due. Prepare journal entries to record the March transactions on Pearl Industries's books. (You may ignore cost of goods sold entries and explanations.) (Credit account titles are automatically indented when amount is entered. Do not indent manually. Record journal entries in the order presented in the problem.) Date Account Titles and Explanation Debit Credit Mar. 11arrow_forwardLloyd Gurango Co. completed the following sales transactions during the month of June 2019. All credit sales have terms of 3/10, n/30 and all invoices are dates as at the transaction date. June 1 Sold merchandise on account to KRA Company, P32 000. Invoice number 377 Sold merchandise on account to LRM Trading, P54 000. Invoice number 378. Sold P46 000 of merchandise for cash. Received payment from KRA Company, less discounts. Received payment from LRM Trading, less discounts. Sold merchandise to JPT Store on account, P62 000. Invoice number 379. 6. Borrowed P30 000 from the Unlad Bank issuing a 10% note payable due in 3 JPT Store returned P11 000 of merchandise from the June 13 sale. Sold merchandise to NOV Convenience Store on account, P17 000. Invoice months number 380. Collected amount due from JPT Store less returns and discounts. 16 Received P6 000 from NOV Convenience Store. Sold goods on account to LPR Co, P34 000. Invoice number 381 347935arrow_forward

- Prepare the journal entries to record the following transactions on Ivanhoe Company's books using a perpetual inventory system. (a) On March 2, Ivanhoe Company sold $840,000 of merchandise on account to Sarasota Company, terms 3/10, n/30. The cost of the merchandise sold was $603,000. (List all debit entries before credit entries. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts.) Account Titles and Explanation (To record credit sale) (To record cost of merchandise sold) Debit Creditarrow_forwardPrepare the journal entries to record the following transactions on Wildhorse Company’s books using a perpetual inventory system. (a) On March 2, Wildhorse Company sold $915,000 of merchandise on account to Novak Company, terms 2/10, n/30. The cost of the merchandise sold was $597,000. (List all debit entries before credit entries. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Debit Credit enter an account title to record credit sale enter a debit amount enter a credit amount enter an account title to record credit sale enter a debit amount enter a credit amount (To record credit sale) enter an account title to record cost of merchandise sold enter a debit amount enter a credit amount enter an account title to record cost of merchandise sold enter a debit amount…arrow_forwardJYP began operation in 2016. For the year ended, the company has the ff details: Merchandise Purchases USD 6, 000, 000 Merchandise Inventory, Dec. 31 USD 2, 400, 000 Collection from customers USD 4, 365, 000 Note that all merch was marked to sell at 35% on selling price. All sales are made on a credit basis and all receivables are collectibl Determine and compute the balance of accounts receivable on year end.arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning