Concept explainers

Videos

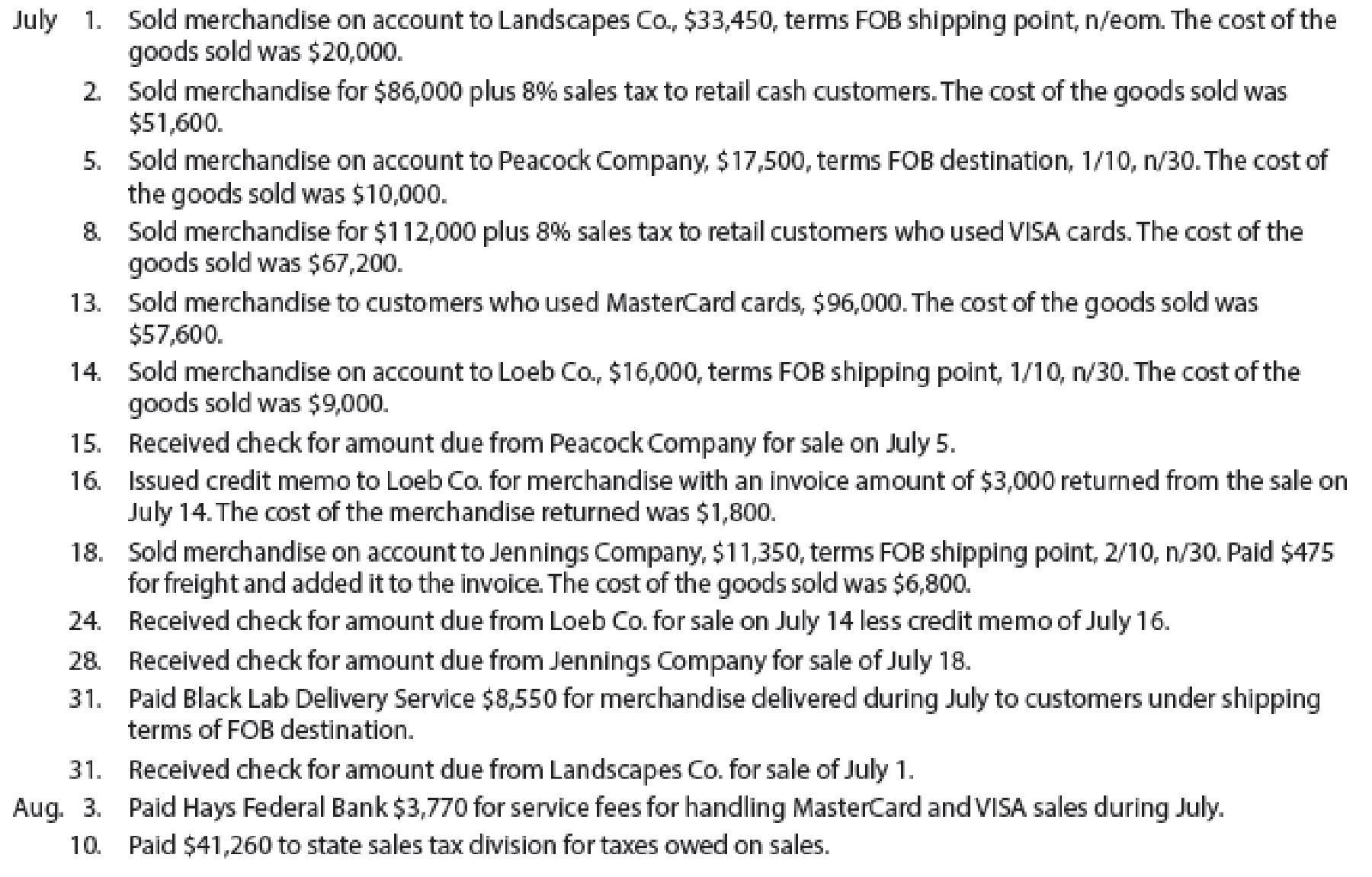

Sales-related transactions using perpetual inventory system

The following selected transactions were completed by Green Lawn Supplies Co., which sells irrigation supplies primarily to other businesses and occasionally to retail customers:

Instructions

Record the sale transactions of the company.

Explanation of Solution

Sales is an activity of selling the inventory of a business.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Accounts receivable | 33,450 | |

| Sales Revenue | 33,450 | ||

| (To record the sale of inventory on account) |

Table (1)

- • Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

- • Sales revenue is revenue and it increases the value of equity by $33,450. Therefore, credit sales revenue with $33,450.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Cost of Sold | 20,000 | |

| Inventory | 20,000 | ||

| (To record the cost of goods sold) |

Table (2)

- • Cost of sold is an expense account and it decreases the value of equity by $20,000. Therefore, debit cost of sold account with $20,000.

- • Inventory is an asset and it is decreased by $20,000. Therefore, credit inventory account with $20,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cash | 92,880 (2) | |

| Sales Revenue | 86,000 | ||

| Sales Tax Payable | 6,880 (1) | ||

| (To record the sale of inventory for cash) |

Table (3)

Working Note (1):

Calculate the amount of sales tax payable.

Sales revenue = $86,000

Sales tax percentage = 8%

Working Note (2):

Calculate the amount of cash received.

Sales revenue = $86,000

Sales tax payable = $6,880 (1)

- • Cash is an asset and it is increased by $92,880. Therefore, debit cash account with $92,880.

- • Sales revenue is revenue and it increases the value of equity by $86,000. Therefore, credit sales revenue with $86,000.

- • Sales tax payable is a liability and it is increased by $6,880. Therefore, credit sales tax payable account with $6,880.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cost of Sold | 51,600 | |

| Inventory | 51,600 | ||

| (To record the cost of goods sold) |

Table (4)

- • Cost of sold is an expense account and it decreases the value of equity by $51,600. Therefore, debit cost of sold account with $51,600.

- • Inventory is an asset and it is decreased by $51,600. Therefore, credit inventory account with $51,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Accounts receivable | 17,325 (3) | |

| Sales Revenue | 17,325 | ||

| (To record the sale of inventory on account) |

Table (5)

Working Note (3):

Calculate the amount of accounts receivable.

Sales = $17,500

Discount percentage = 1%

- • Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

- • Sales revenue is revenue and it increases the value of equity by $17,325. Therefore, credit sales revenue with $17,325.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Cost of Sold | 10,000 | |

| Inventory | 10,000 | ||

| (To record the cost of goods sold) |

Table (6)

- • Cost of sold is an expense account and it decreases the value of equity by $10,000. Therefore, debit cost of sold account with $10,000.

- • Inventory is an asset and it is decreased by $10,000. Therefore, credit inventory account with $10,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cash | 120,960 (5) | |

| Sales Revenue | 112,000 | ||

| Sales Tax Payable | 8,960 (4) | ||

| (To record the sale of inventory for cash) |

Table (7)

Working Note (4):

Calculate the amount of sales tax payable.

Sales revenue = $112,000

Sales tax percentage = 8%

Working note (5):

Calculate the amount of cash received.

Sales revenue = $112,000

Sales tax payable = $8,960 (4)

- • Cash is an asset and it is increased by $120,960. Therefore, debit cash account with $120,960.

- • Sales revenue is revenue and it increases the value of equity by $112,000. Therefore, credit sales revenue with $112,000.

- • Sales tax payable is a liability and it is increased by $8,960. Therefore, credit sales tax payable account with $8,960.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cost of Sold | 67,200 | |

| Inventory | 67,200 | ||

| (To record the cost of goods sold) |

Table (8)

- • Cost of sold is an expense account and it decreases the value of equity by $67,200. Therefore, debit cost of sold account with $67,200.

- • Inventory is an asset and it is decreased by $67,200. Therefore, credit inventory account with $67,200.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cash | 96,000 | |

| Sales Revenue | 96,000 | ||

| (To record the sale of inventory for cash) |

Table (9)

- • Cash is an asset and it is increased by $96,000. Therefore, debit cash account with $96,000.

- • Sales revenue is revenue and it increases the value of equity by $96,000. Therefore, credit sales revenue with $96,000.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cost of Sold | 57,600 | |

| Inventory | 57,600 | ||

| (To record the cost of goods sold) |

Table (10)

- • Cost of sold is an expense account and it decreases the value of equity by $57,600. Therefore, debit cost of sold account with $57,600.

- • Inventory is an asset and it is decreased by $57,600. Therefore, credit inventory account with $57,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Accounts receivable | 15,840 (6) | |

| Sales Revenue | 15,840 | ||

| (To record the sale of inventory on account) |

Table (11)

Working Note (6):

Calculate the amount of accounts receivable.

Sales = $16,000

Discount percentage = 1%

- • Accounts Receivable is an asset and it is increased by $15,840. Therefore, debit accounts receivable with $15,840.

- • Sales revenue is revenue and it increases the value of equity by $15,840. Therefore, credit sales revenue with $15,840.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Cost of Sold | 9,000 | |

| Inventory | 9,000 | ||

| (To record the cost of goods sold) |

Table (12)

- • Cost of sold is an expense account and it decreases the value of equity by $9,000. Therefore, debit cost of sold account with $9,000.

- • Inventory is an asset and it is decreased by $9,000. Therefore, credit inventory account with $9,000.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 15 | Cash | 17,325 | |

| Accounts Receivable | 17,325 | ||

| (To record the receipt of cash against accounts receivables) |

Table (13)

- • Cash is an asset and it is increased by $17,325. Therefore, debit cash account with $17,325.

- • Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

Record the journal entry for sales return.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 16 | Customer Refunds Payable | 2,970 (7) | ||

| Accounts Receivable | 2,970 | |||

| (To record sales returns) |

Table (14)

Working note (7):

Calculate the amount of refund owed to the customer.

Sales return = $3,000

Discount percentage = 1%

- • Customer refunds payable is a liability account and it is decreased by $2,970. Therefore, debit customer refunds payable account with $2,970.

- • Accounts Receivable is an asset and it is decreased by $2,970. Therefore, credit account receivable with $2,970.

Record the journal entry for the return of the .

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 16 | Inventory | 1,800 | |

| Estimated Returns Inventory | 1,800 | ||

| (To record the return of the ) |

Table (15)

- • Inventory is an asset and it is increased by $1,800. Therefore, debit inventory account with $1,800.

- • Estimated retunrs inventory is an expense account and it increases the value of equity by $1,800. Therefore, credit estimated returns inventory account with $1,800.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Accounts receivable | 11,123 (8) | |

| Sales Revenue | 11,123 | ||

| (To record the sale of inventory on account) |

Table (16)

Working Note (8):

Calculate the amount of accounts receivable.

Sales = $11,350

Discount percentage = 2%

- • Accounts Receivable is an asset and it is increased by $11,123. Therefore, debit accounts receivable with $11,123.

- • Sales revenue is revenue and it increases the value of equity by $11,123. Therefore, credit sales revenue with $11,123.

Record the journal entry.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 18 | Accounts Receivable | 475 | ||

| Cash | 475 | |||

| (To record freight charges paid) |

Table (17)

- • Accounts Receivable is an asset and it is increased by $475. Therefore, debit accounts receivable with $475.

- • Cash is an asset and it is decreased by $475. Therefore, credit cash account with $475.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Cost of Sold | 6,800 | |

| Inventory | 6,800 | ||

| (To record the cost of goods sold) |

Table (18)

- • Cost of sold is an expense account and it decreases the value of equity by $6,800. Therefore, debit cost of sold account with $6,800.

- • Inventory is an asset and it is decreased by $6,800. Therefore, credit inventory account with $6,800.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 24 | Cash | 12,870 (9) | |

| Accounts Receivable | 12,870 | ||

| (To record the receipt of cash against accounts receivables) |

Table (19)

Working note (9):

Calculate the amount of cash received.

Net accounts receivable = $15,840

Customer refunds payable = $2,970

- • Cash is an asset and it is increased by $12,870. Therefore, debit cash account with $12,870.

- • Accounts Receivable is an asset and it is increased by $12,870. Therefore, debit accounts receivable with $12,870.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 28 | Cash | 11,598 (10) | |

| Accounts Receivable | 11,598 | ||

| (To record the receipt of cash against accounts receivables) |

Table (20)

Working note (10):

Calculate the amount of cash received.

Net accounts receivable = $11,123

Freight charges = $475

- • Cash is an asset and it is increased by $11,598. Therefore, debit cash account with $11,598.

- • Accounts Receivable is an asset and it is increased by $11,598. Therefore, debit accounts receivable with $11,598.

Record the journal entry for delivery expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 31 | Delivery expense | 8,550 | |

| Cash | 8,550 | ||

| (To record the payment of delivery expenses) |

Table (21)

- • Delivery expense is an expense account and it decreases the value of equity by $8,550. Therefore, debit delivery expense account with $8,550.

- • Cash is an asset and it is decreased by $8,550. Therefore, credit cash account with $8,550.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 31 | Cash | 33,450 | |

| Accounts Receivable | 33,450 | ||

| (To record the receipt of cash against accounts receivables) |

Table (22)

- • Cash is an asset and it is increased by $33,450. Therefore, debit cash account with $33,450.

- • Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 3 | Credit card expense | 3,770 | |

| Cash | 3,770 | ||

| (To record the payment of credit card expenses) |

Table (23)

- • Credit card expense is an expense account and it decreases the value of equity by $3,770. Therefore, debit credit card expense account with $3,770.

- • Cash is an asset and it is decreased by $3,770. Therefore, credit cash account with $3,770.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 10 | Sales tax payable | 41,260 | |

| Cash | 41,260 | ||

| (To record the payment of credit card expenses) |

Table (24)

- • Sales tax payable is a liability account and it is decreased by $41,260. Therefore, debit customer refunds payable account with $41,260.

- • Cash is an asset and it is decreased by $41,260. Therefore, credit cash account with $41,260

Want to see more full solutions like this?

Chapter 5 Solutions

Financial And Managerial Accounting

- Brown Inc. records purchases in a purchases journal and purchase returns in the general journal. Record the following transactions using a purchases journal, a general journal, and an accounts payable subsidiary ledger. The company uses the periodic method of accounting for inventory.arrow_forwardPurchase-related transactions using perpetual inventory system The following selected transactions were completed by Niles Co. during March of the current year: Instructions Journalize the entries to record the transactions of Niles Co. for March.arrow_forwardCostume Warehouse sells costumes and accessories and purchases their merchandise from a manufacturer. Review the following transactions and prepare the journal entry or entries if Costume Warehouse uses A. the perpetual inventory system B. the periodic inventory systemarrow_forward

- PURCHASES JOURNAL, GENERAL LEDGER, AND ACCOUNTS PAYABLE LEDGER The purchases journal of Ryans Rats Nest, a small retail business, is as follows: REQUIRED 1. Post the total of the purchases journal to the appropriate general ledger accounts. Use account numbers as shown in the chapter. 2. Post the individual purchase amounts to the accounts payable ledger.arrow_forwardSales and purchase-related transactions using perpetual inventory system The following were selected from among the transactions completed by Babcock Company during November of the current year: Instructions Journalize the transactions.arrow_forward( Appendix 6A) Recording Purchase and Sales Transactions Refer to the information for Raymond Company in Brief Exercise 6-34 and assume that the company uses the periodic inventory system. Required: Prepare the journal entries to record these transactions on the books of Raymond Company.arrow_forward

- Pharmaceutical Supplies sells medical supplies and purchases their merchandise from a manufacturer. Review the following transactions and prepare the journal entry or entries if Pharmaceutical Supplies uses A. the perpetual inventory system B. the periodic inventory systemarrow_forwardCostume Warehouse sells costumes and accessories. Review the following transactions and prepare the journal entry or entries if Costume Warehouse uses: A. the perpetual inventory system B. the periodic inventory systemarrow_forwardPurchase-related transactions Based on the data presented in Exercise 5-16, journalize Balboa Co.s entries for (A) the purchase, (B) the return of the merchandise for credit, and (C) the payment of the invoice.arrow_forward

- Sales and purchase-related transactions using perpetual inventory system The following were selected from among the transactions completed by Essex Company during July of the current year: Instructions Journalize the transactions.arrow_forwardRecord journal entries for the following sales transactions of Balloon Depot.arrow_forwardPurchase-related transactions using periodic inventory system Selected transactions for Niles Co. during March of the current year are listed in Problem 5-1B. Instructions Journalize the entries to record the transactions of Niles Co. for March using the periodic inventory system.arrow_forward

- Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College  Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub