Concept explainers

a.

To calculate: The amount of FCFE per share for the year 2016 using the data given in the table.

Introduction:

FCFE: When expanded, it is

a.

Answer to Problem 3CP

The free cash flow earning(FCFE) per share will be

Explanation of Solution

The information given to us is as follows:

Table 18A

Sundanci actual 2010 and 2011 financial statements

for fiscal years ending May 31

(Amount in million $, except per share data)

| Income statement | 2010 | 2011 |

| Revenue |  |  |

| 23 | |

| Other operating costs |  |  |

| Income before taxes |  |  |

| Taxes |  |  |

| Net Income |  |  |

| Dividends |  |  |

| Earnings per share |  |  |

| Dividend per share |  |  |

| Common shares outstanding (millions) |  |  |

| Balance sheet | 2010 | 2011 |

| Current assets |  |  |

| Net property, plant and equipment |  |  |

| Total assets |  |  |

| Current liabilities |  |  |

| Long term debt | 0 | 0 |

| Total liabilities |  |  |

| Shareholder’s equity |  |  |

| Total liabilities and equity |  |  |

| Capital expenditures |  |  |

Sundanci FCFE will grow at  for two year and

for two year and  thereafter.

thereafter.

Capital expenditures, depreciation and working capital are expected to increase proportionately with FCFE.

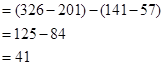

Note 1: Calculation of increase in working capital:

Therefore, when there is an increase in working capital, it implies that the there is an increase in current assets and current liabilities.

Let us now calculate the increase in working capital.

The value of currents assets has increased from Similarly, even the current liabilities have increased from

Similarly, even the current liabilities have increased from  million dollars. So, let us consider the difference amounts for calculations.

million dollars. So, let us consider the difference amounts for calculations.

Therefore the net increase in working capital will be

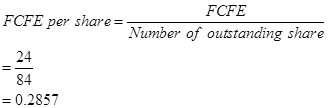

Calculation of FCFE per share:

Number of outstanding shares=84 (as per the given information.)

Number of outstanding shares=84 (as per the given information.)

or 0.286 when rounded off.

Therefore, free cash flow equity per share will be

b.

To calculate: The current value of a share of Sundanci stock using the two-stage FCFE model.

Introduction:

DDM model: DDM model refers to

b.

Answer to Problem 3CP

The current value of the share is

Explanation of Solution

The information given to us is as follows:

Table 18A

Sundanci actual 2010 and 2011 financial statements

for fiscal years ending May 31

(Amount in million $, except per share data)

| Income statement | 2010 | 2011 |

| Revenue |  |  |

| Depreciation |  |  |

| Other operating costs |  |  |

| Income before taxes |  |  |

| Taxes |  |  |

| Net Income |  |  |

| Dividends |  |  |

| Earnings per share |  |  |

| Dividend per share |  |  |

| Common shares outstanding (millions) |  |  |

| Balance sheet | 2010 | 2011 |

| Current assets |  |  |

| Net property, plant and equipment | 474 | 489 |

| Total assets | 675 | 815 |

| Current liabilities | 57 | 141 |

| Long term debt | 0 | 0 |

| Total liabilities | 57 | 141 |

| Shareholder’s equity | 618 | 674 |

| Total liabilities and equity | 675 | 815 |

| Capital expenditures | 34 | 38 |

Sundanci FCFE will grow at 27% for two year and 13% thereafter.

Capital expenditures, depreciation and working capital are expected to increase proportionately with FCFE.

Usage of two-stage FCFE model is simple. We have to first calculate the FCFE per share in the year 2012 and 2013. We have to proceed with calculation using the given information that there is a growth rate of 27%. Then, we have to calculate the terminal value in 2013 which has a continuous growth of 13%. Finally, this value has to be discounted at current period by the required rate of return.

Let us now calculate the current value of a share.

| Income statement | Actual | Estimated | |||

| 2011 | 2012 | 2013 | 2014 | ||

| Growth

rate | 27%- | 27% | 13% | ||

| Per share value | Per share value | Per share value | |||

| Net

Income | 80 |  |  |  |  |

| Add: Depreciation | 23 |  |  |  |  |

| Less:

Capital expenditure | -38 |  |  |  |  |

| Less: Increase in working capital | -41 |  |  |  |  |

| FCFE | 24 |  |  |  |  |

Let us now calculate the terminal value.

The rate of return 14% and perpetuity dividends 13% are converted into decimals by dividing it by 100.

Having done, let us now calculate the total FCFE estimated in 2013.

Let us now discount the FCFE to derive the FCFE per share value.

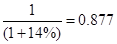

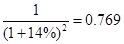

Since, we are given that the required rate of return is 14%, let us use the PV factor of 14%

So, when we are calculating the PV factor for 2012, it will be 1.

For 2013 PV factor=

For 2014 PV factor=

So, now we have to calculate the discounted value.

For 2013 Discounted value

For 2014 discounted value

Therefore, the current value of the share=40.742.

c.

To describe: The limitation of two-state DDM model calculated by using and than by not using the two-stage FCFE model.

Introduction:

DDM Model: DDM model refers to dividend discount model. It is supposed to be a quantitative method useful in estimating the company’s stock price.

c.

Answer to Problem 3CP

The assumption of continuous growth sounds unrealistic resulting in a number of limitations on usage.

Explanation of Solution

The whole concept of DDM is based on the theory that the present- day’s price is worth the sum of all of its future dividend payments which are later discounted back to is

- The shares of a company cannot be valued using DDM model since distribution of dividends is not possible. With the help of FCFE model, the value of the firm can be predicted even though dividends are not distributed.

- When both models i.e., FCFE model and DDM, we can observe one thing. The assumption of continuous growth rate sounds unrealistic. Practically seen, the growth rate keeps on changing and it is highly impossible for it to be stable for a long time. Estimation of the time when the growth rate will be constant is not possible. This results in difficulty in calculation of required rate of return.

Want to see more full solutions like this?

Chapter 18 Solutions

EBK INVESTMENTS

- Using the Value Line Investment Survey report in Exhibit 11.5, find the following information for Apple. What was the amount of revenues (i.e., sales) generated by the company in 2017? What were the latest annual dividends per share and dividend yield? What is the earnings per share (EPS) projection for 2019? How many shares of common stock were outstanding? What were the book value per share and EPS in 2017? How much long-term debt did the company have in the third quarter of 2018?arrow_forwardThe forecast for Discomfort’s free cash flows for next year is provided in the table. Assume that free cash flow is paid at the end of each year and we are at the beginning of a year. Last year’s values are for the year end yesterday. Analysts expect Discomfort’s cash flow to remain constant at next year’s level in perpetuity. The WACC for Discomfort is 8%. What is the fair price for Discomfort’s shares today? Selected Financial Information Discomfort Inc. ($000s) Last Year Next Year Sales 743,203 934,978 Depreciation 13,543 20,401 EBIT 90,453 119,787 Tax Rate, T 34.8% 34.8% Net Working Capital -64200 -61662 Net Property and Equipment 43,850 79,356 Long-Term Debt 14,216 15,263 Shares Outstanding 20,000 20,000 Round your answer to the nearest cent.arrow_forwardDreamline expects to earn $20 per share this year and intends to pay out $8 in dividends to shareholders. It is planning to invest in new projects with an expected return on equity of 20%. The future plans of Dreamline involve retaining the same dividend payout ratio. Dreamline expects to earn 20% on its equity .The number of common shares outstanding will remain unchanged. i) Calculate the future growth rate for Dreamline’s earnings. ii) If the required rate of return of for Dreamline’s common stock is 15%, what would be the price of Dreamline’s common stock? iii) Compare the valuation of bonds and preferred stock with that of common stockarrow_forward

- You expect Fab Corp to pay a dividend of $2.14/share next year (Year 1); $2.24/share in Year 2; $2.35/share in Year 3; and $2.55/share in Year 4. You also believe the stock will trade in the market at $130/share at the end of Year 4. Draw a timeline for Fab Corp given your expectations assuming all cash flows occur at the end of each year. You have estimated Fab Corp’s Cost of Equity to be 9.1%. Using your timeline, estimate what Fab’s stock should be trading at now.arrow_forwardUse your own words to answer the following questions: Write the formula for the P/E ratio and what it measures? Should you invest in a company with high P/E or low P/E? A company has the following items for the fiscal year 2020: Revenue = 10 million Net income = 4 million The company has 2 million shares of stock Stock price per share = $70 Calculate the company’s earnings per share and P/E ratioarrow_forwardAt the beginning of 2012 investors had invested $25,000 of common equity in Grant Corp. and expect to earn a return of 11% per year. In addition, investors expect Grant Corp. to pay out 100% of income in dividends each year. Forecasts of Grant's net income are as follows: 2012 - $3,500 2013 $3,200 2014 - $2,900 2015 and beyond - $2,750 Using this information, what is Grant's residual income valuation at the beginning of 2012?arrow_forward

- ranger Inc. has done the following projections for its balance sheet: total assets of $85 million, current liabilities of $29 million, long-term liabilities of $43 million. If the firm will require net new financing of $1 million, what is the projected amount of stockholders' equity?arrow_forwardProcter and Gamble (PG) paid an annual dividend of $2.89 in 2018. You expect PG to increase its dividends by 7.7% per year for the next five years (through 2023), and thereafter by 3.3% per year. If the appropriate equity cost of capital for Procter and Gamble is 8.7% per year, use the dividend-discount model to estimate its value per share at the end of 2018. (Round to the nearest cent.)arrow_forwardProcter and Gamble (PG) paid an annual dividend of $2.86 in 2018. You expect PG to increase its dividends by 8.7% per year for the next five years (through 2023), and thereafter by 2.7% per year. If the appropriate equity cost of capital for Procter and Gamble is 8.3% per year, use the dividend-discount model to estimate its value per share at the end of 2018.arrow_forward

- The stock of Nogro Corporation is currently selling for $29 per share. Earnings per share in the coming year are expected to be $3.90. The company has a policy of paying out 50% of its earnings each year in dividends. The rest is retained and invested in projects that earn a 21% rate of return per year. This situation is expected to continue indefinitely. a. Assuming the current market price of the stock reflects its intrinsic value as computed using the constant-growth DDM, what rate of return do Nogro's investors require (round to 2 decimal places)? Rate of Return ?% b. By how much does its value exceed what it would be if all earnings were paid as dividends and nothing were reinvested (round to 2 decimal places)? PVGO $?arrow_forwardThe stock of Nogro Corporation is currently selling for $28 per share. Earnings per share in the coming year are expected to be $7.00. The company has a policy of paying out 50% of its earnings each year in dividends. The rest is retained and invested in projects that earn a 25% rate of return per year. This situation is expected to continue indefinitely. Required: Assuming the current market price of the stock reflects its intrinsic value as computed using the constant-growth DDM, what rate of return do Nogro’s investors require? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. By how much does its value exceed what it would be if all earnings were paid as dividends and nothing were reinvested? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. If Nogro were to cut its dividend payout ratio to 25%, what would happen to its stock price? Note: Round your answer to 2 decimal places. What would happen to its…arrow_forwardAn analyst is trying to estimate the intrinsic value of VN Co. that has a weighted average cost of capital at 10%. The estimated free cash flows for the company for the following years are: · Year 1 P3,000 · Year 2 P4,000 · Year 3 P5,000 The analyst estimates that after three years, free cash flow will grow at a constant annual percentage of 6%. What is the total intrinsic value of the company’s common stock if combined debt and preferred stock has a P25,000 market value? A. 98,556 B. 109,339 C. 78,310 D. 84,339arrow_forward

Pfin (with Mindtap, 1 Term Printed Access Card) (...FinanceISBN:9780357033609Author:Randall Billingsley, Lawrence J. Gitman, Michael D. JoehnkPublisher:Cengage Learning

Pfin (with Mindtap, 1 Term Printed Access Card) (...FinanceISBN:9780357033609Author:Randall Billingsley, Lawrence J. Gitman, Michael D. JoehnkPublisher:Cengage Learning

Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning