Videos

Two departments within Cougar Gear Inc. are Production and Sales. Each department has a unique scorecard, as follows:

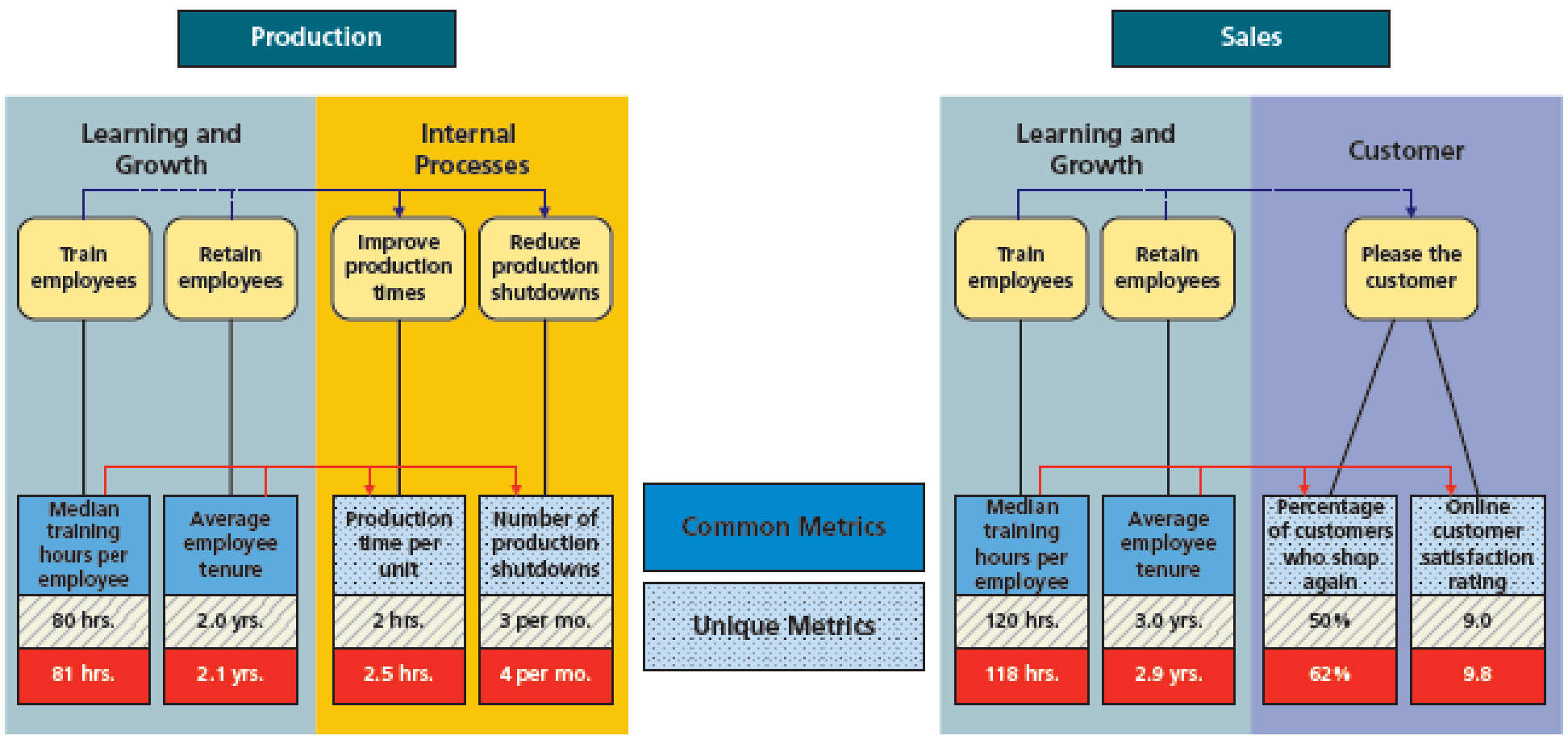

The Production Department scorecard focuses on the learning and growth and internal processes perspectives. The Sales Department scorecard focuses on the learning and growth and customer perspectives. Both scorecards have the learning and growth performance metrics of median training hours per employee and average employee tenure. The Production scorecard has the unique metrics of production time per unit and number of production shutdowns. The Sales scorecard has the unique metrics of percentage of customers who shop again and online customer satisfaction rating. The performance targets for each metric are shown in the tan boxes just under the performance metrics. The actual achieved metrics are shown in the red boxes just below the tan boxes. When evaluating both departments, Cougar Gear’s management looks at the median training hours per employee and average employee tenure metrics and subsequently decides to give the Sales Department a large bonus while giving the Production Department a minimal bonus.

- a. Determine and define the type of cognitive bias Cougar Gear’s management has exhibited in this instance.

- b. Determine which department would have received the larger bonus had the company’s management not been biased in the evaluation.

- c. Discuss one advantage and one disadvantage of using unique balanced scorecards for different departments or divisions of a company.

Want to see the full answer?

Check out a sample textbook solution

Chapter 14 Solutions

Managerial Accounting

- Classify each of the following performance measures into the balanced scorecard perspective to which it relates: financial perspective, internal operations perspective, learning and growth perspective, or customer perspective. A. Employee satisfaction surveys B. Units of waste per production process, uniformity of products and inventory control C. Number of energy-efficient bulbs replaced D. Management training course certificates awarded E. Divisional profit F. Number of customer referralsarrow_forwardConsider the following list of scorecard measures: a. Product profitability b. Ratings from customer surveys c. Number of patents pending d. Strategic job coverage ratio e. Revenue per employee f. Quality costs g. Percentage of market h. Employee turnover percentages i. First-pass yields j. On-time delivery percentage k. Percentage of revenues from new sources l. Economic value added Required: Classify each measure according to the following: perspective, financial or nonfinancial, subjective or objective, and external or internal. When the perspective is process, identify which type of process: innovation, operations, or post-sales service.arrow_forwardFrom the following list of performance measures, label each one as Financial, Customer, Internal Business Processes, or Learning and Growth: Percentage of on-time deliveries Employee turnover ratio Revenue from new products Number of new customers Percentage of compensation based on team performance Percentage of products returned Operating income Time taken to replace defective productsarrow_forward

- Coulson and Company is a large retail business that has a firm-wide balanced scorecard. Recently, management has discussed the need for the balanced scorecard to be more relevant to each individual department of the company. Specifically, management wants to come up with unique scorecards for its Public Relations and Inventory Management departments. For both departments, management recognizes that properly and efficiently training employees is important. For these purposes, management gathers data on the median training hours per employee and new employee performance review ratings. For the Inventory Management Department, management is focused on reducing stockouts (running out of certain inventory items) and keeping accurate inventory counts. For these purposes, the company tracks the number of back orders and discrepancies between the physical and record counts of inventory, respectively. For the Public Relations Department, management is focused on improving the publics CSR image of the company and attracting new customers. Management measures these objectives using Forbes CSR Rating of Coulson and Company and the number of new customers, respectively. a. Identify the term for Coulson and Companys plan to create unique balanced scorecards for its individual departments. b. Draw the unique balanced scorecards of each department. Identify the departments common and unique measures, and include all the elements of the balanced scorecard that you can in your drawings, given the information provided.arrow_forwardDescribing the balanced scorecard and identifying key performance indicators for each perspective Consider the following key performance indicators, and classify each indicator according to the balanced scorecard perspective it addresses. Choose from the financial perspective, customer perspective, internal business perspective, and the learning and growth perspective. Number of customer complaints Number of information system upgrades completed Residual income New product development time Employee turnover rate Percentage of products with online help manuals Customer retention Percentage of compensation based on performance Percentage of orders filled each week Gross margin growth Number of new patents Employee satisfaction ratings Manufacturing cycle time (average length of the production process) Earnings growth Average machine setup time Number of new customers Employee promotion rate Cash flow from operations Customer satisfaction ratings Machine downtime Finished products per…arrow_forwardCoulson and Company is a large retail business that has a firm-wide balanced scorecard. Recently, management has discussed the need for the balanced scorecard to be more relevant to each individual department of the company. Specifically, management wants to come up with unique scorecards for its Public Relations and Inventory Management departments. For both departments, management recognizes that properly and efficiently training employees is important. For these purposes, management gathers data on the median training hours per employee and new employee performance review ratings. For the Inventory Management Department, management is focused on reducing stockouts (running out of certain inventory items) and keeping accurate inventory counts. For these purposes, the company tracks the number of back orders and discrepancies between the physical and record counts of inventory, respectively. For the Public Relations Department, management is focused on improving the public’s CSR image…arrow_forward

- Coulson and Company is a large retail business that has a firm-wide balanced scorecard. Recently, management has discussed the need for the balanced scorecard to be more relevant to each individual department of the company. Specifically, management wants to come up with unique scorecards for its Public Relations and Inventory Management departments. For both departments, management recognizes that properly and efficiently training employees is important. For these purposes, management gathers data on the median training hours per employee and new employee performance review ratings. For the Inventory Management Department, management is focused on reducing stockouts (running out of certain inventory items) and keeping accurate inventory counts. For these purposes, the company tracks the number of back orders and discrepancies between the physical and record counts of inventory, respectively. For the Public Relations Department, management is focused on improving the public’s CSR image…arrow_forwardClassify the performance measures below into the most likely balanced scorecard perspective itrelates to. Label your answers using C (customer), P (internal process), I (innovation and growth), or F(financial). Length of time raw materials are in inventoryarrow_forwardThe controller of Tri Con Global Systems Inc. has developed a new costing system that traces the cost of activities to products. The new system is able to measure post-manufacturing activities, such as selling, promotional, and distribution activities, and allocate these activities to products in a manner that provides a more complete view of the company's product costs. This system produces better strategic information about the relative profitability of product lines. In the course of implementing the new costing system, the controller realized that the company's current period GAAP net income would increase significantly if the new product cost information were used for inventory valuation on the financial statements. The controller has been under intense pressure to improve the company's net income, and this would be an easy and effective way for her to help meet the company's short-term net income goals. As a result, she has decided to use the new costing system to determine GAAP…arrow_forward

- The controller of Tri Con Global Systems Inc. has developed a new costing system that traces the cost of activities to products. The new system is able to measure post-manufacturing activities, such as selling, promotional, and distribution activities, and allocate these activities to products in a manner that provides a more complete view of the company's product costs. This system produces better strategic information about the relative profitability of product lines. In the course of implementing the new costing system, the controller realized that the company's current period GAAP net income would increase significantly if the new product cost information were used for inventory valuation on the financial statements. The controller has been under intense pressure to improve the company's net income, and this would be an easy and effective way for her to help meet the company's short-term net income goals. As a result, she has decided to use the new costing system to determine GAAP…arrow_forwardDescribing the balanced scorecard and identifying key performance indicators for each perspective Consider the following key performance indicators, and classify each according to the balanced scorecard perspective it addresses. Choose from financial perspective, customer perspective, internal business perspective, or learning and growth perspective. a. Number of employee suggestions implemented b. Revenue growth c. Number of on-time deliveries d. Percentage of sales force with access to real-time inventory levels e. Customer satisfaction ratings f. Number of defects found during manufacturing g. Number of warranty claims h. Return on investment i. Variable cost per unit j. Percentage of market share k. Number of hours of employee training l. Number of new products developed m. Yield rate (number of units produced per hour) n. Average repair time o. Employee satisfaction p. Number of repeat customersarrow_forwardDescribing the balanced scorecard and identifying key performance indicators for each perspective Consider the following key performance indicators, and classify each indicator according to the balanced scorecard perspective it addresses. Choose from the financial perspective, customer perspective, internal business perspective, and the learning and growth perspective. a. Number of customer complaints b. Number of information system upgrades completed c. Residual income d. New product development time e. Employee turnover rate f. Percentage of products with online help manuals g. Customer retention h. Percentage of compensation based on performance i. Percentage of orders filled each week j. Gross margin growth k. Number of new patents l. Employee satisfaction ratings m. Manufacturing cycle time (average length of production process) n. Earnings growth o. Average machine setup time p. Number of new customers q. Employee promotion rate r. Cash flow from operations s. Customer…arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning