Videos

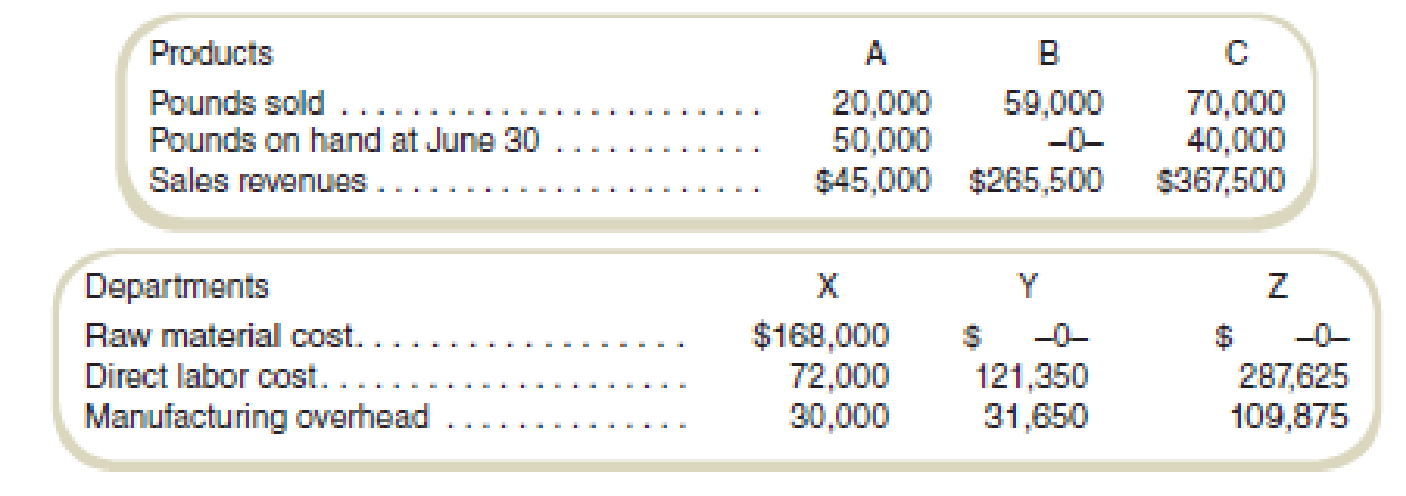

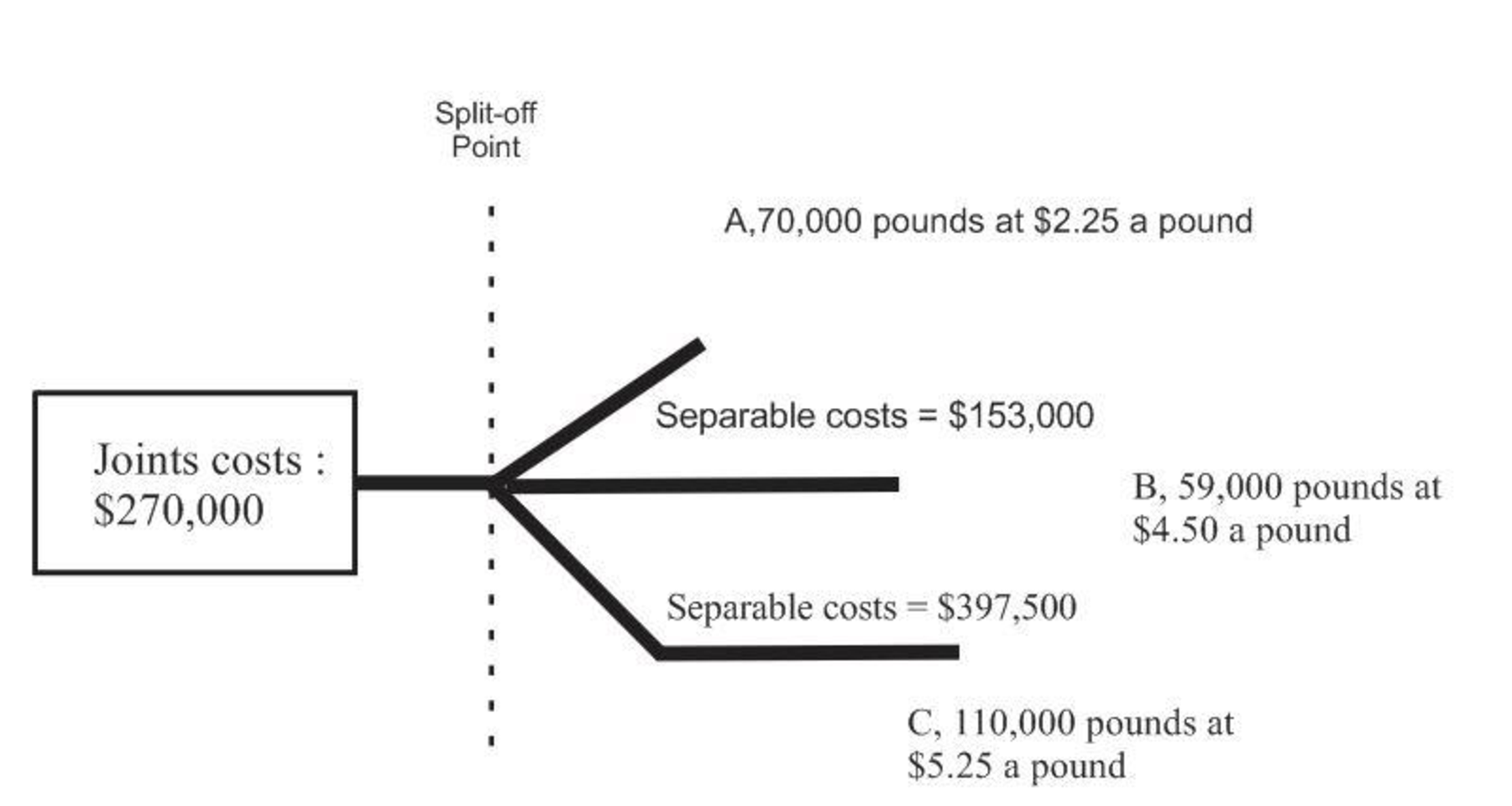

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of allocating joint production costs. Following is a summary of costs and other data for the quarter ended June 30.

No inventories were on hand at the beginning of the quarter. No raw material was on hand at June 30. All units on hand at the end of the quarter were fully complete as to processing.

Required

- a. Determine the following amounts for each product: (1) estimated net realizable value used for allocating joint costs, (2) joint costs allocated to each of the three products, (3) cost of goods sold, and (4) finished goods inventory costs, June 30.

- b. Assume that the entire output of product A could be processed further at an additional cost of $6.00 per pound and then sold for $12.90 per pound. What would have been the effect on operating profits if all of product A output for the quarter had been further processed and then sold rather than being sold at the split-off point?

- c. Write a memo to management indicating whether the company should process product A further and why.

a.

Determine the following amounts for each product:

(1) The estimated net realizable value used for allocating joint costs

(2) The joint costs allocated to each of the three products

(3) The cost of goods sold, and

(4) The finished goods inventory costs, June 30.

Explanation of Solution

Joint cost allocation:

Joint cost allocation allocates the common cost of the various departments of the business. IT, accounting and administration services are utilized by various departments so it should be allocated to the various departments based on the usage of the cost.

Determine the estimated net realizable value used for allocating joint costs:

1.

| Particulars | Product A | Product B | Product C | Total |

| Selling price per pound: | ||||

| A: | $ 2 | |||

| C: | $ 5 | |||

| Pounds produced: | ||||

| A: | 70,000 | |||

| C: | 110,000 | |||

| Gross sales values | $ 157,500 | $ 265,500 | $ 577,500 | |

| Less: Costs of separate processing: | ||||

| A: | $ - | |||

| B: | $ 153,000 | |||

| C: | $ 397,500 | |||

| Estimated net realizable values at split-off point | $ 157,500 | $ 112,500 | $ 180,000 | $450,000 |

| Percentage of total | 35% | 25% | 40% | 100% |

Table: (1)

2.

Determine the joint costs allocated to each of the three products:

Product A:

Product B:

Product C:

Total joint costs:

Thus, the total amount of the joint cost is $270,000.

3.

| Particulars | Total costs | Cost of goods sold | Ending inventory |

| Product A: | |||

| Joint costs allocated | $ 94,500 | ||

| Sold: | $ 27,000 | ||

| Inventory | $ 67,500 | ||

| Product B: | |||

| Joint costs allocated | $ 67,500 | ||

| Separate processing costs | $ 153,000 | ||

| Total of sales | $ 220,500 | $ 220,500 | $ - |

| Product C: | |||

| Joint costs allocated | $ 108,000 | ||

| Separate processing costs | $ 397,500 | ||

| Total costs of Z | $ 505,500 | ||

| Sold: | $ 321,682 | ||

| Inventory | $ 183,818 | ||

| Total | $ 820,500 | $ 569,182 | $ 251,318 |

Table: (2)

4.

Thus, the cost of the finished goods inventory as on June 30 is $569,182.

b.

Identify the effect on operating profits if all of the product A output had been further processed for the quarter and then sold rather than being sold at the split-off point.

Explanation of Solution

Operating profit:

The operating profit is the excess of total revenues over total expenses after adjusting for depreciation and taxes.

Compute the incremental revenue of further processing:

Compute the incremental costs of further processing:

Compute the effect on operating profits:

Thus, the operating profits have been increased by $325,500 when all of the product A output for the quarter had been further processed and then sold rather than being sold at the split-off point.

c.

Prepare a memo to management indicating whether product A should be processed by the company or not.

Explanation of Solution

Memo

From

ABC

To

XYZ

Re: Whether product A should be continued by the management or not.

Dear XYZ,

I am glad to share that Product A is going to bring an additional operating profit of $325,500. So, here I am explaining to you whether Product A should be continued by the management.

Product A:

The incremental revenue arising out of the product is $745,500, and the incremental costs are $420,000. Thus, it results in an extra profit of $325,500.

Thus, the company should continue with product A because it is going to be profitable if it is further processed.

I hope now you are clear about the information I have provided regarding whether the product should be processed or not. You can revert if you need some more information or clarification on the information provided.

Regards,

ABC

Want to see more full solutions like this?

Chapter 11 Solutions

Fundamentals Of Cost Accounting (6th Edition)

Additional Business Textbook Solutions

Fundamentals of Financial Accounting

Fundamentals Of Financial Accounting

FINANCIAL ACCT.FUND.(LOOSELEAF)

Financial Accounting

Cost Accounting (15th Edition)

Managerial Accounting: Tools for Business Decision Making

- CARAMEL Inc. manufactures three joint products. The following production data were provided by CARAMEL Inc. for the current period: Product Name Units Produced X Y Z Joint product costs for the current period were as follows: Raw materials Direct labor Factory overhead Costs before separation Costs after separation: X 1,000 2,000 3,000 The company uses the net realizable value method for allocating joint costs. 8. What is the Gross profit/(loss) on the sale of all X products? Y Z Production for April, in pounds: Z Additional Processing Final Selling Price Cost after Split Off 9. What is the total gross profit (loss) on the sale of all the joint products? MACCHIATO Company produces two main products jointly. X and Y. and Z. which is a by- product of Y. X and Y are produced from the same raw material. Z is manufactured from the residue of the process creating Y. Sales for April: Costs before separation are apportioned between the two main products by the net realizable value method. The…arrow_forwardTroester Manufacturing produces products X, Y, and Z from a joint process. Each product can be processed further and sold as X- Prime, Y-Prime, and Z-Prime. Information on the operations for the most recent period follows. Required: Determine the value of each missing item. The joint costs of $144,000 for X is the portion of the total joint cost of $288,000 that had been allocated to X. Note: Do not round intermediate calculations. Product Units produced Joint costs Sales value at split-off Additional costs to convert to Prime Sales value as Prime $ X 76,800 144,000 Y 38,400 33,600 $ 24,000 336,000 184,000 $ Z 19,200 72,000 14,400 96,000 Total 134,400 288,000 480,000 72,000 $ 616,000 $arrow_forwardArdmore Company produces two main products jointly, A and B, and C, which is a by-product of B. A and B are produced from the same raw material. C is manufactured from the residue of the process creating B. Costs before separation are apportioned between the two main products by the net realizable value method. The net revenue realized from the sale of C is deducted from the cost of B. Data for April were as follows: Costs before separation P200,000 Costs after separation: A 50,000 B 32,000 C 4,000 Production for April, in pounds: A 800,000 B 200,000 C 20,000 Sales for April: A 640,000 pounds @ P0.4375 B 180,000 pounds @ 0.65 C 20,000 pounds @ 0.30 Determine the gross profit for April.arrow_forward

- Fundador Inc. makes two products, Wet and Dry, from a joint operating process. For the month of May 2021, the total joint costs of processing was P120,000 and the costs of further processing after the point of split-off, as well as other relevant data, are as follows: The company uses the net realizable value method for allocating the joint costs of processing. For the month of may 2021, the joint costs allocated to product Wet was: A. 60,000 B. 66,000 C. 72,000 D. 80,000arrow_forwardA company manufactures three products, L-Ten, Triol, and Pioze, from a joint process. Each production run costs 12,900. None of the products can be sold at split-off, but must be processed further. Information on one batch of the three products is as follows: Required: 1. Allocate the joint cost to L-Ten, Triol, and Pioze using the net realizable value method. (Round the percentages to four significant digits. Round all cost allocations to the nearest dollar.) 2. What if it cost 2 to process each gallon of Triol beyond the split-off point? How would that affect the allocation of joint cost to the three products?arrow_forwardOakes Inc. manufactured 40,000 gallons of Mononate and 60,000 gallons of Beracyl in a joint production process, incurring 250,000 of joint costs. Oakes allocates joint costs based on the physical volume of each product produced. Mononate and Beracyl can each be sold at the split-off point in a semifinished state or, alternatively, processed further. Additional data about the two products are as follows: An assistant in the companys cost accounting department was overheard saying ...that when both joint and separable costs are considered, the firm has no business processing either product beyond the split-off point. The extra revenue is simply not worth the effort. Which of the following strategies should be recommended for Oakes?arrow_forward

- Leigh Manufacturers produces three products from a common manufacturing process. The total joint cost of producing 2,000 pounds of Product A; 1,000 pounds of Product B; and 1,000 pounds of Product C is P7,500. Selling price per pound of the three products are P15 for Product A; P10 for Product B; and P5 for Product C. Joint cost is allocated using the sales value method. Compute the unit cost of Product A if all three products are main products. Compute the unit cost of Product A if Products A and B are main products and Product C is a by-product for which the cost reduction method is used.arrow_forwardCorporation manufactures three products from a joint process. The three products are in industrial grade form at the split- off point. They can either be sold at that point or processed further into premium grade. Costs related to each batch of this process is as follows: Sales Price at split-off point Allocated joint costs Sales Price after further processing Cost of further processing Product Quantity Product 1 $16 $6,000 $20 $5,330 1,000 lb. Product 2 $12 $6,000 $18 $2,050 1,000 lb. Product 3 $5 $6,000 $14 $2,530 1,000 lb. Q: What would be the additional amount of profit that more profitable to process further rather than be sold at the split-off point? A: $ Corp, would gain from further processing the product(s) that is/arearrow_forwardABC Company produces two main products and a by-product out of a joint process. The ratio of output quantities to input quantities of direct material used in the joint process remains consistent from month to month. ABC employs the physical units method to allocate joint pro- duction costs to the two main products. The net realizable value of the by-product is used to reduce the joint production costs before the joint costs are allocated to the main products. Da- ta regarding ABC's operations for the current month are presented below. During the month, ABC incurred joint production costs of P2,520,000. The main products are not mar- ketable at the split-off point and, thus, have to be processed further. Monthly output in Kilos.. Selling price per Kilo. Separable process costs. First Main Product Second Main Product 150,000 P14 By-Product 60,000 P2 90,000 P30 P540,000 P660,000 The amount of joint production cost that ABC would allocate to the Second Main Product by using the physical…arrow_forward

- ABC Company produces two main products and a by-product out of a joint process. The ratio of output quantities to input quantities of direct material used in the joint process remains consistent from month to month. ABC employs the physical units method to allocate joint pro- duction costs to the two main products. The net realizable value of the by-product is used to reduce the joint production costs before the joint costs are allocated to the main products. Da- ta regarding ABC's operations for the current month are presented below. During the month, ABC incurred joint production costs of P2,520,000. The main products are not mar- ketable at the split-off point and, thus, have to be processed further. First Main Product Second Main Product Monthly output in Kilos.. Selling price per Kilo.. Separable process costs. By-Product 60,000 P2 90,000 P30 150,000 P14 P540,000 P660,000 The amount of joint production cost that ABC would allocate to the Second Main Product by using the physical…arrow_forwardJoint Products; By-Products (Appendix) The Marshall Company has a joint production process that produces two joint products and a by-product. The joint products are Ying and Yang, andthe by-product is Bit. Marshall accounts for the costs of its products using the net realizable valuemethod. The two joint products are processed beyond the split-off point, incurring separable processing costs. There is a $1,000 disposal cost for the by-product. A summary of a recent month’s activityat Marshall is shown below:Ying Yang BitUnits sold 50,000 40,000 10,000Units produced 50,000 40,000 10,000Separable processing costs—variable $140,000 $42,000 $—Separable processing costs—fixed $10,000 $8,000 $—Sales price $6.00 $12.50 $1.60Total joint costs for Marshall in the recent month are $265,000, of which $115,000 is a variable cost.Required1. Calculate the manufacturing cost per unit for each of the three products.2. Calculate the total gross margin for each productarrow_forwardCONSO Inc. manufactures joint products ALT and TAB, and a by-product DEL. Costs are assigned to the joint products by the net realizable value or final market value method which considers further processing costs in subsequent operations. It is the policy of CONSO Inc. to account for its by-product by market value or reversal cost method or deduction of net realizable value of by-product from the joint manufacturing costs of main products. The total manufacturing costs for 100,000 units were Php 1,520,000.00 during the year. Production and costs data follow: (a)Product Name: ALT, units produced:60,000, sales price per unit: Php 70.00, Further processing cost per unit Php 20.00 (b)Product Name: TAB, units produced:30,000, sales price per unit: Php 25.00, Further processing cost per unit Php 5.00 (C)Product Name: DEL, units produced:10,000, sales price per unit: Php 10.00, Further processing cost per unit Php 30.00, Selling and admin expense per unit, Php 5.00. 1.What is the value of DEL…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub