Concept explainers

Videos

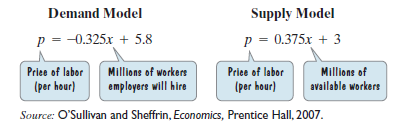

An important application of systems of equations arises in connection with supply and demand. As the price of a product increases, the demand for that product decreases. However, at higher prices, suppliers are willing to produce greater quantities of the product. The price at which supply and demand are equal is called the equilibrium price. The quantity supplied and demanded at that price is called the equilibrium quantity. Exercises 61-62 involve supply and demand.

The following models describe wages for low-skilled labor.

a. Solve the system and find the equilibrium number of workers, in millions, and the equilibrium hourly wage.

b. Use your answer from part (a) to complete this statement:

If workers are paid ____ per hour, there will be ____ million available workers and ____ million workers will be hired.

c. In 2007, the federal minimum wage was set at $5.15 per hour. Substitute 5.15 for p in the demand model,

d. At a minimum wage of $5.15 per hour, use the supply model,

e. At a minimum wage of $5.15 per hour, use your answers from parts (c) and (d) to determine how many more people are looking for work than employers are willing to hire.

Want to see the full answer?

Check out a sample textbook solution

Chapter 7 Solutions

EBK THINKING MATHEMATICALLY

- Redo Exercise 5, assuming that the house blend contains 300 grams of Colombian beans, 50 grams of Kenyan beans, and 150 grams of French roast beans and the gourmet blend contains 100 grams of Colombian beans, 350 grams of Kenyan beans, and 50 grams of French roast beans. This time the merchant has on hand 30 kilograms of Colombian beans, 15 kilograms of Kenyan beans, and 15 kilograms of French roast beans. Suppose one bag of the house blend produces a profit of $0.50, one bag of the special blend produces a profit of $1.50, and one bag of the gourmet blend produces a profit of $2.00. How many bags of each type should the merchant prepare if he wants to use up all of the beans and maximize his profit? What is the maximum profit?arrow_forward23. Consider a simple economy with just two industries: farming and manufacturing. Farming consumes 1/2 of the food and 1/3 of the manufactured goods. Manufacturing consumes 1/2 of the food and 2/3 of the manufactured goods. Assuming the economy is closed and in equilibrium, find the relative outputs of the farming and manufacturing industries.arrow_forward

Linear Algebra: A Modern IntroductionAlgebraISBN:9781285463247Author:David PoolePublisher:Cengage Learning

Linear Algebra: A Modern IntroductionAlgebraISBN:9781285463247Author:David PoolePublisher:Cengage Learning

Algebra & Trigonometry with Analytic GeometryAlgebraISBN:9781133382119Author:SwokowskiPublisher:Cengage

Algebra & Trigonometry with Analytic GeometryAlgebraISBN:9781133382119Author:SwokowskiPublisher:Cengage