Review Figure 3.4. Suppose the

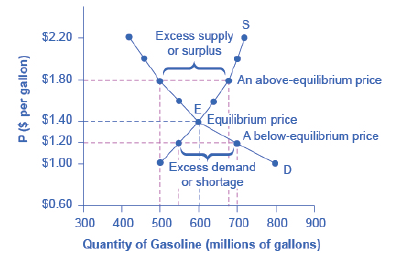

Figure 3.4

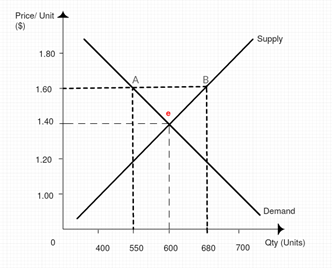

If the price of gasoline is $1.60 per gallon and the equilibrium price is $1.40 per gallon. Comment whether the quantity demanded and supplied is higher or lower at $1.60 per gallon. Is there a shortage or surplus?

Explanation of Solution

As per the diagram, the equilibrium price is $1.40 per gallon in the market. Any price above the equilibrium price level in the market creates surplus of the product in the market and any price below the equilibrium price creates a shortage of the product in the market.

In the above figure, at price level $1.60 per gallon, the quantity demand is 550 millions of gallons and quantity supply is 680 million gallons, represented by point A and B in the diagram. Clearly, we can see that quantity supply is more than quantity demand and there is a surplus of the product.

If the price is below the equilibrium price, then there will be shortage of the product.

Equilibrium Price: It is that level of price where demand of a product is equal to the supply of a product.

Want to see more full solutions like this?

Chapter 3 Solutions

Principles of Macroeconomics 2e

Additional Business Textbook Solutions

Financial Accounting (12th Edition) (What's New in Accounting)

Engineering Economy (17th Edition)

Business Essentials (12th Edition) (What's New in Intro to Business)

Foundations Of Finance

Horngren's Accounting (12th Edition)

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

- There are many different ways that governments collect taxes. In Zambia alone there are income taxes, taxes on copper and other mining royalties, taxes on property and financial transactions among others. One common tax is sales tax. Sales taxes are collected by the retailer when the final sale in the supply chain occurs via a sale to the end customer. In some parts of the world, however, rather than a sales tax, there is a Value Added Tax (VAT). In a VAT system taxes are collected by all sellers in each stage of the supply chain. Suppliers, Manufacturers, Distributors, and Retailers all collect the VAT on applicable sales and consumers pay the VAT on their purchases. The Zambian government in recent years has heavily debated the merits of which system is better a national sales tax on end purchase transactions or a VAT which collects taxes at each stage. For the purposes of this research paper, debate whether Zambia should have a national sales tax system or a VAT system. Which…arrow_forwardThe U.S. Census Bureau conducts annual surveys to obtain information on the percentage of the voting-age population that is registered to vote. Suppose that 679 employed persons and 690 unemployed persons are independently and randomly selected, and that 429 of the employed persons and 369 of the unemployed persons have registered to vote. Can we conclude that the percentage of employed workers (P1), who have registered to vote, exceeds the percentage of unemployed workers (P2), who have registered to vote? Use a significance level of α = 0.05 for the test. Step 5 of 6: Determine the decision rule for rejecting the null hypothesis Ho. Round the numerical portion of your answer to three decimal places.arrow_forwardDon't give AI generated solution Give only typing answer with explanationarrow_forward

- Consider a standard Hotelling model of competition with quadratic transportation costs. The consumers are located uniformly along a segment of unit length. There are two firms, A and B, located at the opposite ends of the segment. Each firm has constant marginal costs 2. Each consumer buys at most one unit of product and gets utility 20. Each consumer incurs travel cost of 4 times the square of traveled distance. Find equilibrium price and profit of firm A when firms set a unform price for the entire Hotelling segment. Suppose now that firms can price discriminate between consumers located in the interval 悯 (interval 1) and those located in the interval 瞓 (interval 2). Find equilibrium prices of firm A and B on the interval 1. Answer: equilibrium uniform price of firm A = profit of firm A under uniform pricing = equilibrium price of firm A on interval 1 = equilibrium price of firm B on interval 1 = ✓arrow_forwardDon't give AI generated solution Give all answers Please send me the graph for part farrow_forwardYou are planning to open a new Italian restaurant in your hometown where there are three other Italian restaurants. You plan to distinguish your restaurant from your competitors by offering northern Italian cuisine and using locally grown organic produce. What is likely to happen in the restaurant market in your hometown after you open? Part 2 A. While the demand curves facing your competitors becomes more elastic, your demand curve will be inelastic. B. The demand curve facing each restaurant owner shifts to the right. C. The demand curve facing each restaurant owner becomes more elastic. D. Your competitors are likely to change their menus to make their products more similar to yours.arrow_forward

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics Today and Tomorrow, Student EditionEconomicsISBN:9780078747663Author:McGraw-HillPublisher:Glencoe/McGraw-Hill School Pub Co

Economics Today and Tomorrow, Student EditionEconomicsISBN:9780078747663Author:McGraw-HillPublisher:Glencoe/McGraw-Hill School Pub Co

Microeconomics: Principles & PolicyEconomicsISBN:9781337794992Author:William J. Baumol, Alan S. Blinder, John L. SolowPublisher:Cengage Learning

Microeconomics: Principles & PolicyEconomicsISBN:9781337794992Author:William J. Baumol, Alan S. Blinder, John L. SolowPublisher:Cengage Learning