FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

your line manager wants to assess your understanding and ability to prepare and produce the appropriate final accounts such as profit and loss account, owners’ equity statement, and balance sheet as well as how these accounts are differed under different forms and types of business.

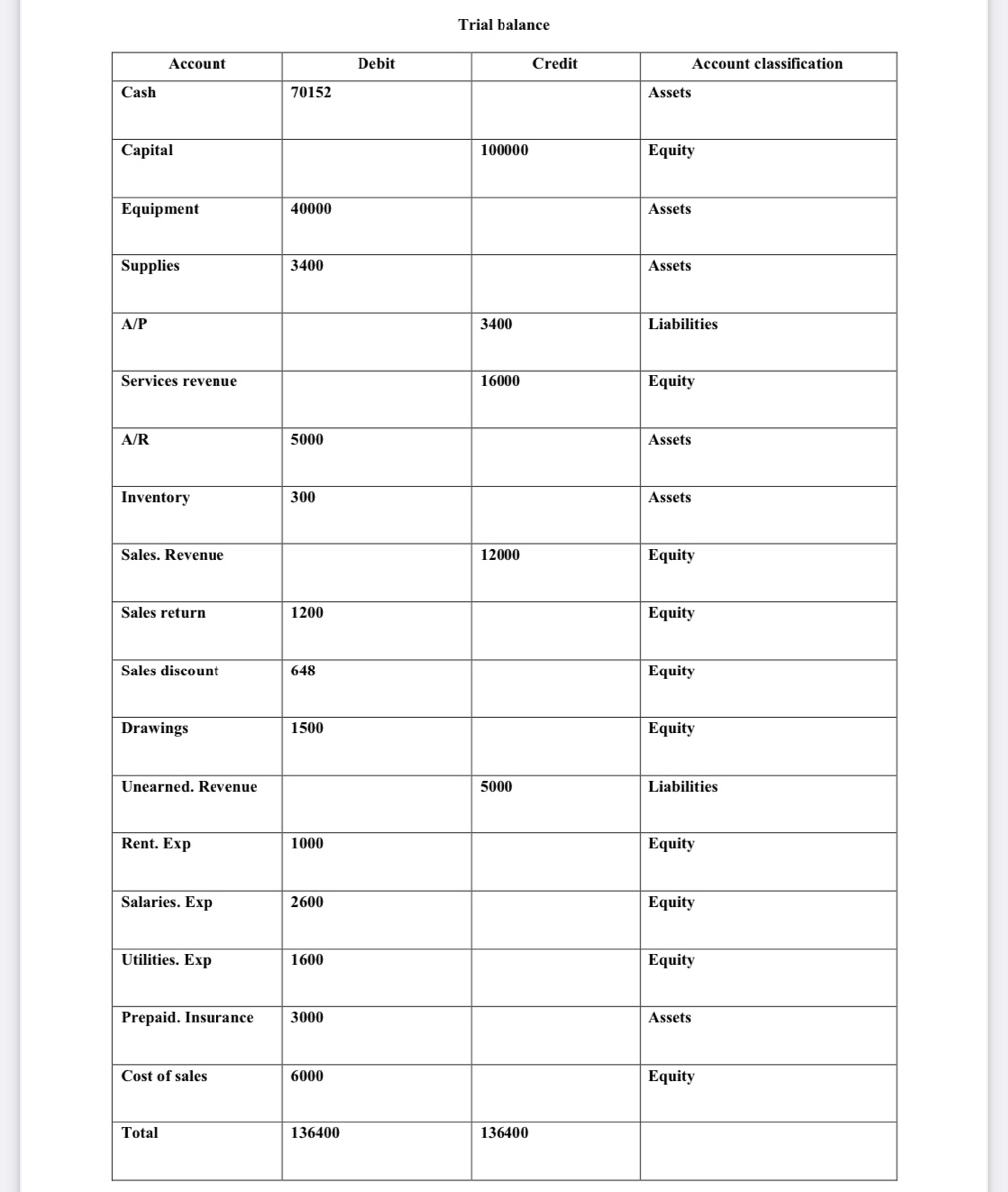

Produce the final accounts for a sole trader business (Software Programming Company) from task 1 including profit and loss account, owners’ equity statement, and balance sheet for the Period ended July 31st. using the trial balance that you have produced in problem 2/ task1

2) Make the adjustments entries for the following transactions before preparing the final accounts for LLC company:

On the 20th of October 2019, the business purchased supplies for 8000 cash. On 31st of December, 2019 the business found out that the supplies still on hand were 4000 only.

The business has a Equipment with book value of 17000, with annual depreciation rate of 10%.

On the 1st of July the business purchased a one-year insurance policy for 1500. Prepare the adjusting

entry on 31st of December 2019.

The employees are paid salaries on the 27th of each month. Prepare the adjusting entry of 4500 of

the employees’ salaries that are not yet paid on the 31st of December, 2019.

3) Use the given adjusted trial balance for ABC, LLC (Table 2) to prepare the final accounts including profit and loss account, retained earnings statement, and balance sheet for the Period ended December 31st.

4) Compare the essential features of each financial account statement to analyse the differences between them in terms purpose, structure and content.

Adjusted Trial Balance of the ABC, LLC for the Period ended 31st of December

Transcribed Image Text:Trial balance

Account

Debit

Credit

Account classification

Cash

70152

Assets

Сapital

100000

Equity

Equipment

40000

Assets

Supplies

3400

Assets

A/P

3400

Liabilities

Services revenue

16000

Equity

A/R

5000

Assets

Inventory

300

Assets

Sales. Revenue

12000

Equity

Sales return

1200

Equity

Sales discount

648

Equity

Drawings

1500

Equity

Unearned. Revenue

5000

Liabilities

Rent. Exp

1000

Equity

Salaries. Exp

2600

Equity

Utilities. Exp

1600

Equity

Prepaid. Insurance

3000

Assets

Cost of sales

6000

Equity

Total

136400

136400

Transcribed Image Text:Table 2

Adjusted Trial Balance of the ABC, LLC for the Period ended 31st of December

Account Title

Dr.

Cr.

Cash

110000

Accounts Receivable

15000

Supplies

4000

Prepaid Insurance

10000

Equipment

17000

Accumulated depreciation – Equipment

2000

Unearned Service Revenue

9000

Taxes Payable

2000

Salaries payable

2500

Share Capital

110000

Retained Earnings

25000

Dividends

22000

Service Revenue

39500

Insurance expenses

1500

Salaries Expense

4500

Depreciation Expense

2000

Supplies expenses

4000

Total

190000

190000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 14 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Describe how information reduces risk when you make a personal or work-related decision. What are information rules? How do they simplify the process of making decisions? What is the difference between data and information? Give one example of accounting data and one example of accounting information. List the five functions of an MIS. What are the components of a typical business report? Describe the three types of computer applications that help employees, managers, and executives make smart decisions. What purpose do audits and GAAPs serve in today’s business world? How do the major provisions of the Sarbanes-Oxley Act affect a public company’s audit procedures? What is the principal difference between a balance sheet and an income statement? How are current assets distinguished from fixed assets? Why are fixed assets depreciated on a balance sheet? How does the use of money solve the problems associated with a barter system of exchange? For a business firm, what type of activities…arrow_forward2) In the accounting cycle, after examining source documents and recording transaction an accounting journal, what is the next step taken by a financial manager? A) posting recorded transactions B) gathering credit card receipts C) closing the books D) preparing a trial balance E) balancing the accounting equationarrow_forwardSelect the best answer for each statement. Revenue is recorded when products and services are Choose. delivered. Each business is accounted for separately from its owner Choose. or owners. Financial statements reflect the assumption that the business continues operating. Choose. A company reports details behind financial statements Choose. that would impact users' decisions. Concepts, assumptions, and guidelines for preparing Choose. financial statements.arrow_forward

- Why is it vital for a business to have a complete and accurate chart of accounts? Select an answer: so income and expense items can be posted to the business's balance sheet so the default feature in QuickBooks can alphabetize by categories and subcategories so receipts and payments can be applied to the appropriate categories and subcategoriesarrow_forwardResearch a company you are familiar with, either in person or online, and determine what the company uses as a source document to input data into their Enterprise Resource Planning (ERP) system. Examples could be a purchase order or a new account form. Explain what the forms are used for and determine if the same documents can be used for a manufacturing company and a retail or service company.arrow_forwardMake first a proper Chart of Accounts. Then make a proper Trial Balance from the following accounts and balances listed in alphabetical order for MN Company for August 31 of the current year. Put them in the correct order along with their debit and credit balances on your Trial Balance. Total the DR and CR column and make sure they balance. Make sure you have a heading. We will work on this in class. Upload here on D2L if you are not yet finished in class. Accounts Payable $2300, Accounts Receivable $1200, Accumulated Depreciation-Equipment $800, Advertising Expense $200, Cash $3400, Equipment $12,500, Furniture and Fixtures $6700, MN, Capital, $6500, MN, Drawing $500, Notes Payable $8000, Prepaid Insurance $1200, Professional Fees $10,000, Rent Expense $500, Supplies $100, Utilities Expense $300, Wages Expense $1000.arrow_forward

- Managerial accounting reports are prepared: Oa. to provide creditors with information useful in making credit decisions. Ob. to meet the needs of decision makers within the firm. Oc. to present historical information. Od. All of these choices are correct.arrow_forwardExplain expenditure cycle for the business operating in an online environment. Identify the three (3) threats faced in an online expenditure cycle and provide relevant three (3) controls.arrow_forwardWhat is an estimate in QuickBooks Online? Select an answer: An estimate is a document that outlines a customer's purchase history. An estimate is a document that shows a customer's payment history. An estimate is a document that outlines the expenses a business expects to incur in the future. An estimate is a document that outlines the products or services a business plans to provide to a customer.arrow_forward

- Reviewing high level processes, interviewing, understanding the business is part of the _____ phase. Group of answer choices Survey Planning Work program Reportingarrow_forwardHello Please provide the journal entry for I.arrow_forwardList and describe the major steps a business should follow in developing a new accounting information system (i.e., the phases of the system’s development life cycle). Be thorough in your answerarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education