Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

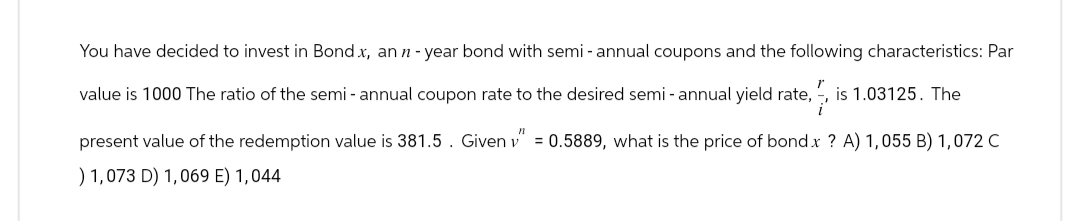

Transcribed Image Text:You have decided to invest in Bond x, an n-year bond with semi-annual coupons and the following characteristics: Par

value is 1000 The ratio of the semi - annual coupon rate to the desired semi- annual yield rate, is 1.03125. The

present value of the redemption value is 381.5. Given v=0.5889, what is the price of bond x ? A) 1,055 B) 1,072 C

) 1,073 D) 1,069 E) 1,044

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The YTM on a bond is the interest rate you earn on your investment if interest rates don't change. If you actually sell the bond before it matures, your realized return is known as the holding period yield (HPY). a. Suppose that today you buy an annual coupon bond with a coupon rate of 8.4 percent for $825. The bond has 8 years to maturity and a par value of $1,000. What rate of return do you expect to earn on your investment? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b-1. Two years from now, the YTM on your bond has declined by 1 percent, and you decide to sell. What price will your bond sell for? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) b-2. What is the HPY on your investment? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) X Answer is complete but not entirely correct. Rate of return…arrow_forwardThe yield curve reveals that the 1-year spot rate is 6.9% and the 2-year spot rate is 9.0%. What is the duration of a 2-year bond with a face value of $1,000.00 making annual coupon payments of 35.6%? Do not report the modified duration. O a. 1.17 O b. 1.28 O c. 1.65 O d. 1.90 O e. 1.05 Of. 1.43 O g. 1.77 O h. 1.53arrow_forwardWhat are the yield to maturity on a three-year bond whose face value is $1000 with a coupon rate of 6% per year and a price of $900? Given the above yield to maturity, what would be the price on a two-year coupon bond whose face value is $1000 with a coupon rate of 4% per year? Choose the closest price. (1) $944 (2) $954 (3) $964 (4) $974 (5) $984arrow_forward

- Suppose a ten-year, $1,000 bond with an 8.4% coupon rate and semiannual coupons is trading for $1,034.84. a. What is the bond's yield to maturity (expressed as an APR with semiannual compounding)? b. If the bond's yield to maturity changes to 9.9% APR, what will be the bond's price? **** a. What is the bond's yield to maturity (expressed as an APR with semiannual compounding)? The bond's yield to maturity is%. (Round to two decimal places.)arrow_forwardYou are given the following spot rates: s1 = 6%, s2 = 7%, s3 = 8%.Calculate the YTM for a 3 year bond that sells for the present value of its cash flows. The bond has 6% coupons that are paid annually and is redeemed for its $1,000 par value. Answer Choices: a) 7.12% b) 7.50% c) 7.76% d) 7.92%arrow_forwardNeed help finding the current yield for both bond P and D, & the capital yield gains for both bonds P and D. Thank you in advancearrow_forward

- For time value of money calculations (circle all that apply): Increasing i increases present value Increasing i increases future value More frequent compounding increases future value More frequent discounting increases present value n is always expressed in yearsarrow_forward4) A coupon bond pays this amount every 6 months; $ 30.00 bgs for the number of payments/year; 2 The bond also pays at maturity the par (face) value; $ 1,000.00 Number of years until maturity 15 The required return of holders of this bond is; 8.00% bgs a) What is the PV of the CFs, or what would be the fair price to purchase this bond? b) If the required return of holders of this bond is; 6.00% bgs What is the PV of the CFs, or what would be the fair price to purchase this bond? c) If the required return of holders of this bond is; 4.00% What is the PV of the CFs, or what would be the fair price to purchase this bond? to purchase this bond? bgs d) If the previous bond sells for; $ (976.00) What must be the yield to maturity for this bond (aka IRR) ? (to…arrow_forwardFor example, assume Sophia wants to earn a return of 7.00% and is offered the opportunity to purchase a $1,000 par value bond that pays a 7.00% coupon rate (distributed semiannually) with three years remaining to maturity. The following formula can be used to compute the bond’s intrinsic value: Intrinsic ValueIntrinsic Value = = A(1+C)1+A(1+C)2+A(1+C)3+A(1+C)4+A(1+C)5+A(1+C)6+B(1+C)6A1+C1+A1+C2+A1+C3+A1+C4+A1+C5+A1+C6+B1+C6 Complete the following table by identifying the appropriate corresponding variables used in the equation. Unknown Variable Name Variable Value A Bond’s semiannual coupon payment B Bond’s par value $1,000 C Semiannual required return Now, consider the situation in which Sophia wants to earn a return of 5.00%, but the bond being considered for purchase offers a coupon rate of 7.00%. Again, assume that the bond pays semiannual interest payments and has three years to maturity. If you round the bond’s…arrow_forward

- you re creating a yield curve in order to price some forward rate agreements. You have assembled the following prices for bonds (all of which pay semi-annual coupons): Maturity Coupon (per annum) Price (per $100 face value) 6 months 2.25% 98.1363 12 months 1.75% 95.3758 18 months 6.50% 99.1579 (a) What are the discount factors for: i. 6 months? ii. 12 months? iii. 18 months? (b) What is the 6-18 month forward rate, quoted with semi-annual compounding?arrow_forwardConsider two bonds x and y, both with face value 100, coupon rate 10%, and maturity of 1 year. Assume that the interest rate is 10%. Assume that bond y will go into default on both the principal and interest payments with a probability of 50%. Suppose that prices equal the expected discounted payments. What is the difference in the yields to maturity? (a) The yields to maturity are the same. (b) 110. (c) 120. (d) 10. (e) 12.arrow_forwardAssume that you are considering the purchase of a 20-year, noncallable bond with an annual coupon rate of 9.5%. The bond has a face value of $1,000, and it makes semiannual interest payments. If you require an 10.7% nominal yield to maturity on this investment, what is the maximum price you should be willing to pay for the bond? раy a. $910.81 b. $874.74 c. $721.44 d. $1,000.99 O e. $901.80arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education