Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

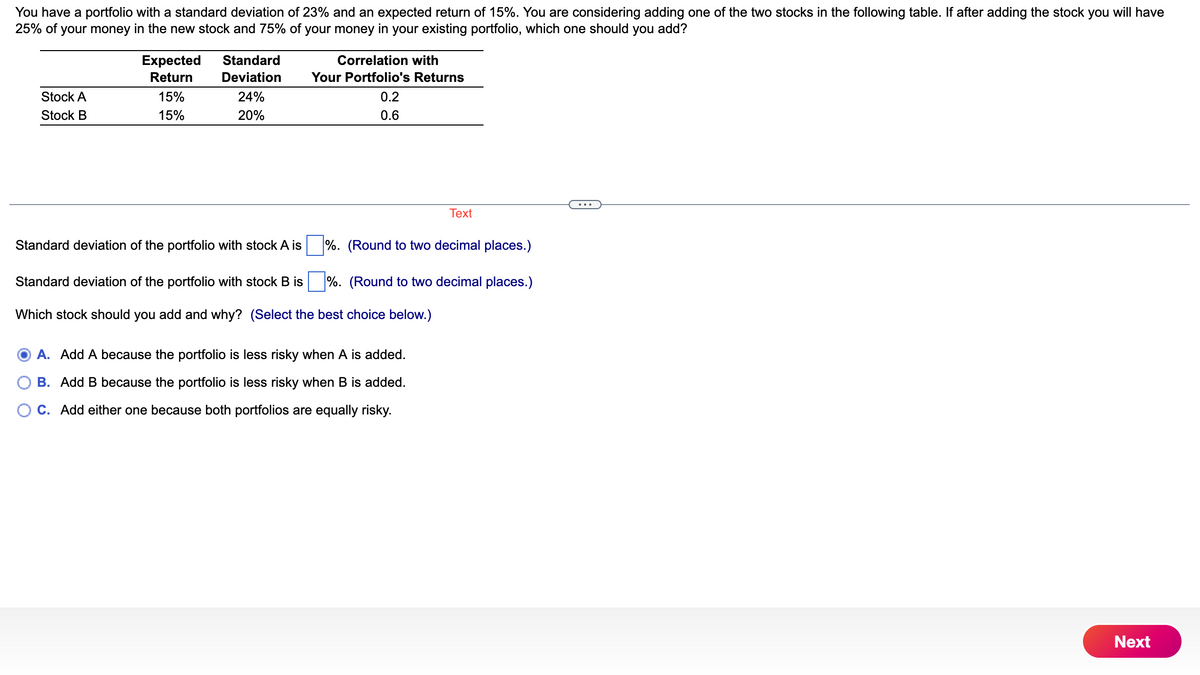

Transcribed Image Text:You have a portfolio with a standard deviation of 23% and an expected return of 15%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have

25% of your money in the new stock and 75% of your money in your existing portfolio, which one should you add?

Stock A

Stock B

Expected

Return

15%

15%

Standard

Deviation

24%

20%

Standard deviation of the portfolio with stock A is

Correlation with

Your Portfolio's Returns

0.2

0.6

%. (Round to two decimal places.)

%. (Round to two decimal places.)

Standard deviation of the portfolio with stock B is

Which stock should you add and why? (Select the best choice below.)

Text

A. Add A because the portfolio is less risky when A is added.

B. Add B because the portfolio is less risky when B is added.

OC. Add either one because both portfolios are equally risky.

Next

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You are considering three stocks—A, B, and C—for possible inclusion in your investment portfolio. Stock A has a beta of 0.80, stock B has a beta of 1.40, and stock C has a beta of -0.30. If the return on the market portfolio increased by 12%, what change would you expect in the return for each stock? If the return on the market portfolio decreased by 5%, what change would you expect in the return for each stock?arrow_forwardalso do deviation of stock b pleasearrow_forwardConsider the following information about three stocks: Probability 0.22 State of Economy Boom Normal Bust 0.53 0.25 Stock A 0.24 0.00 0.17 -0.28 Stock B 0.36 0.13 -0.45 Stock C 0.55 0.09 Instructions: a) If your portfolio is invested 40% each in A and B and 20% in C, what is the portfolio expected return? The variance? The standard deviation? b) If the expected T-bill rate is 3.80%, the expected inflation rate is 3.50% what are the approximate and exact expected real returns on the portfolio? what is the approximate real risk premium? Show your steps.arrow_forward

- Your client has $102,000 invested in stock A. She would like to build a two-stock portfolio by investing another $102,000 in either stock B or C. She wants a portfolio with an expected return of at least 14.0% and as low a risk as possible, but the standard deviation must be no more than 40%. What do you advise her to do, and what will be the portfolio expected return and standard deviation? Expected Return Standard Deviation Correlation with A A B с 15% 13% 13% 47% 40% 40% Part 1 of 5 The expected return of the portfolio with stock B is 1.00 0.11 0.32 %. (Round to one decimal place.)arrow_forwardYou have a portfolio consisting solely of stock A and stock B. The portfolio has an expected return of 10.6% stock A has an expected return of 12.4%. Stock B is expected to return 6.6%. What is the portfolio weight of stock A?arrow_forwardYou have a portfolio with a standard deviation of 24% and an expected return of 19%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 30% of your money in the new stock and 70% of your money in your existing portfolio, which one should you add? Standard deviation of portfolio with stock A is ? Expected Return Standard Deviation Correlation with Your Portfolio's Returns Stock A 12 % 22 % 0.2 Stock B 12 % 17 % 0.7arrow_forward

- You are analyzing a stock that has a beta of 1.3 and a standard deviation of 12.0%. The risk-free rate is 4.2% and you estimate the expected return on the market portfolio to be 11.1%. What return do you expect this stock to have? The expected return according to CAPM is: OA. 13.2% B. 14.3% OC. 19.8% OD. 18.6% OE 12.0% OF. 14.4% OG. 9.8% OH. 8.7% OL 9.0%arrow_forwardYou manage a risky portfolio with an expected rate of return of 13% and a standard deviation of 34%. The T-bill rate is 2%. Stock A Stock B Stock C 45% 32% 23% Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate of return of 11%. Required: a. What is the proportion y? b. What are your client's investment proportions in your three stocks and the T-bill fund? c. What is the standard deviation of the rate of return on your client's portfolio? Complete this question by entering your answers in the tabs below. Required A Required B Required C What is the proportion y? Note: Round your answer to the nearest whole number. Proportion y %arrow_forwardYou want to create a portfolio equally as risky as the market, and you have $250,000 to invest. Given this information, fill in the three missing pieces of information in the following table. Show your calculations: Investment Betal 0.90 Asset Stock A $50,000 Stock B $70,000 Stock C Risk-Free Asset 1.25 1.60arrow_forward

- Consider a portfolio consisting of the three risky stocks. You decide to invest 25 percent in Apple, 35 percent in HP and 40 percent in Spree. These stocks show the volatility at the level of 11.15 percent, 24.4 percent and 15.29 percent, and the correlation with the market portfolio at the level of 0.65, 0.83 and 0.36, respectively. Calculate the expected portfolio return using CAPM if the market portfolio shows the expected return of 12.88 percent and its volatility is 10.05 percent. The risk-free rate of return is 3.31 percent. Please make sure your answer is correct tutor. Out of my questions in Bartleby, 90% are wrong all the time. Which is resulting also to my low grades. Don't get it if you don't know the answer. Please use TEXT. not snip or handwriting. Thank youarrow_forwardNikularrow_forwardYou want to create a portfolio that is 80% as risky as the market. You can choose to invest in either Stock B with a beta of 2 or the risk-free asset. How much do you invest in Stock B? A. 40% B. 50% C. 60% D. 70%arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education