MATLAB: An Introduction with Applications

6th Edition

ISBN: 9781119256830

Author: Amos Gilat

Publisher: John Wiley & Sons Inc

expand_more

expand_more

format_list_bulleted

Related questions

Question

This 2qstns are correlated

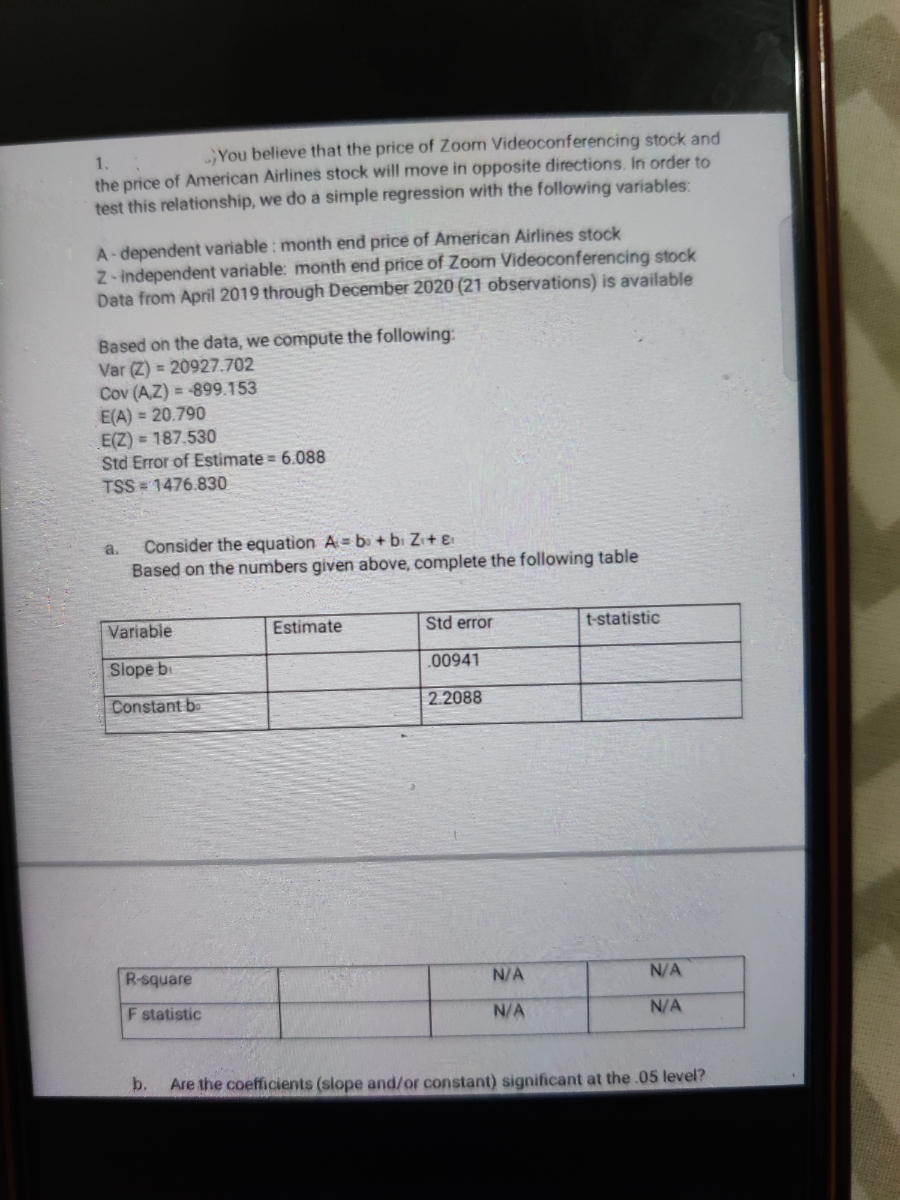

Transcribed Image Text:You believe that the price of Zoom Videoconferencing stock and

the price of American Airlines stock will move in opposite directions. In order to

test this relationship, we do a simple regression with the following variables:

1.

A-dependent variable : month end price of American Airlines stock

Z-independent variable: month end price of Zoom Videoconferencing stock

Data from April 2019 through December 2020 (21 observations) is available

Based on the data, we compute the following:

Var (2) = 20927.702

Cov (AZ) = -899.153

E(A) = 20.790

E(Z) = 187.530

Std Error of Estimate = 6.088

TSS = 1476.830

Consider the equation A = b + bi Z+ &

Based on the numbers given above, complete the following table

a.

Variable

Estimate

Std error

t-statistic

Slope b

.00941

Constant b

2.2088

R-square

N/A

N/A

F statistic

N/A

N/A

b.

Are the coefficients (slope and/or constant) significant at the.05 level?

Transcribed Image Text:You believe that the VIX trades in regimes where its average level

2.

is significantly different. You define four regimes from 2004 through 2021: June

2008 through October 2011 (financial crisis); February 2020 through March 2021

(the COVID-19 crisis); the 12-month transition periods before and after the

financial crisis and the current transition period after the COVID-19 crisis; and the

remaining periods of low volatility. In order to test your hypothesis, you examine

month-end values of the VIX from January 2004 through October 2021 (214

observations) and conduct the following regression:

Dependent variable YMonth-end value of VIX

Dummy variable X1:Financial Crisis: 1 if between June 2008 through Oct 2011,0

if not

Dummy variable X2:COVID-19 crisis: 1 if between Feb 2020 through March 2021,

O if not

Dummy variable X2:Transition period: 1 if in 12 months before or after the

financial crisis orthe current period since the COVID-19 crisis

(June 2007 - May 2008, Nov 2011 - Oct 2012, or April 2021 Oct 2021)

The results for the regression are as follows

Coefficie

Standard

Error

0.5226

1.0610

nts

Intercept

financial crisis

COVID-19 crisis

transition

14.63

13.21

15.71

1.6643

5.40

1.1835

How would the introduction of Dummy variable X4: Low volatility period

(Jan 2004- May 2007, or Nov 2012-Jan 2020) affect the output of this

regression? Why?

a.

b. Which of the coefficients are significant at the 0.01 level?

C.

According to the regression result, what was the average value of the VIX

during the COVID-19 Crisis?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 6 steps

Knowledge Booster

Similar questions

- It takes a while for new factory workers to master a complex assembly proces. During thre first month new employees wor, the company tracks the number of days the have been on the job and the length of time it rtakes them to complete assembly. The correlation is most likely to be what?arrow_forwardThe degrees of freedom of correlation test is determined by what?arrow_forwardPls help ASAParrow_forward

- What does it mean if the linear correlation coefficient is A) 0? B) -1?arrow_forwardA researcher is studying the intensity of hurricanes that entered the Gulf of Mexico between 1975-2015 and the average water temperature of the Gulf of Mexico at the hurricane's peak strength. What is the independent and dependent variable in this study?arrow_forwardSuppose data are collected concerning the weight of a person in pounds and the number of calories burned in 30 minutes of walking on a treadmill at 3.5 miles per hour. How would the value of the correlation coefficient, r, change if all of the weights were converted to kilograms?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- MATLAB: An Introduction with ApplicationsStatisticsISBN:9781119256830Author:Amos GilatPublisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning  Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON

Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman

The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

MATLAB: An Introduction with Applications

Statistics

ISBN:9781119256830

Author:Amos Gilat

Publisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...

Statistics

ISBN:9781305251809

Author:Jay L. Devore

Publisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...

Statistics

ISBN:9781305504912

Author:Frederick J Gravetter, Larry B. Wallnau

Publisher:Cengage Learning

Elementary Statistics: Picturing the World (7th E...

Statistics

ISBN:9780134683416

Author:Ron Larson, Betsy Farber

Publisher:PEARSON

The Basic Practice of Statistics

Statistics

ISBN:9781319042578

Author:David S. Moore, William I. Notz, Michael A. Fligner

Publisher:W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:9781319013387

Author:David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:W. H. Freeman